Bond Traders Are Too Quick to Doubt the Fed's Resolve

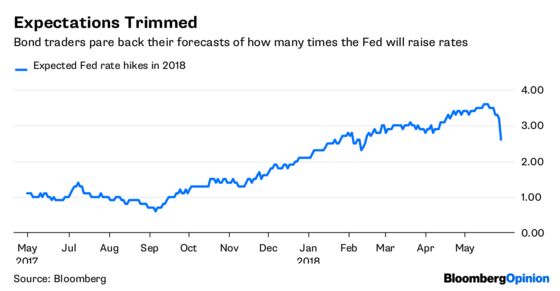

(Bloomberg Opinion) -- Bond traders in the U.S. responded to the brewing crisis in Italy by sharply reducing their forecasts for how many times the Federal Reserve will raise interest rates this year. In reality, it’s too soon to make that call. The U.S. economy is in a very different place compared with previous rounds of the European debt crisis. To be sure, Fed policy makers will be watching the European situation closely for signs of contagion, but they will be watching the U.S economy even more closely.

My baseline position on monetary policy remains unchanged, which is that the Fed is most likely to follow up on its March rate increase with another in two weeks and then another in September. At that point, its target for the federal funds rate will be in a range of 2 percent to 2.25 percent, close to the lower end of estimates of neutral. At that point, policy will become increasingly data-dependent. Absent more obvious inflationary pressures, the Fed will be wary of pushing rates much beyond neutral.

It shouldn’t be surprising that the bond market has revised lower its expectations of rate hikes in coming months amid speculation that the political turmoil in Italy could cause the euro zone’s currency union to unravel. That, in turn, has led investors to seek safety in U.S. government bonds while the storm plays out, pushing yields down.

The current situation in the euro zone would have to unravel very quickly to force the Fed to change course at its June 12-13 policy meeting. The Fed will remain focused on incoming data indicating the economy is running at a fairly strong pace. For example, the regional manufacturing surveys are coming in hot, suggesting the economy maintains significant momentum this quarter. And that momentum is likely to keep downward pressure on the unemployment rate, which is already well below the Fed’s estimates of what is consistent with full employment. The Fed will be inclined to continue pushing policy rates toward neutral in this environment.

What about September and beyond? The same story applies, in that the domestic economy will be the dominant factor in the Fed’s policy decisions. Remember that with the inflation rate ticking higher, the Fed is fairly close to meeting its goals — much closer than when the euro-zone crisis was reaching a crescendo in 2011-12. Back then, the U.S. unemployment was at an unacceptably high average annual rate of 8.9 percent, more than twice the current rate. At that point in time, the nascent economy recovery was simply much more vulnerable than now to external shocks. As a result, the Fed then needed to weigh such shocks more heavily when formulating policy.

When does Italy become a problem that needs Fed attention? Two mechanisms strike me as potentially impacting policy. The first is that the U.S. economy slows markedly relative to the Fed’s expectations as a result of a slowdown related to Europe or emerging markets. This won’t happen overnight and thus wouldn’t become a factor in the near term, but could later in the year and next. The second mechanism is that the situation in Italy spills over into other euro-zone nations, leading to a return to the financial contagion seen in 2011 and 2012 or something like the swift moving 1997 Asian Financial Crisis. We are not there yet.

The Italian situation does present a communications challenge for the Fed. Central bankers will acknowledge the situation and associated possibility of downside risks that could change policy. But they will emphasize that changing course is only a possibility and that the baseline expectations for further rate hikes remains as yet unchanged. They will attempt to maintain focus on the strength of the domestic economy as the primary factor driving policy. The Fed will need a more rapid spread of Italy’s problems before Chairman Jerome Powell and his fellow policy makers shift direction.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

©2018 Bloomberg L.P.