Doubting the Fed’s Resolve Is a Losing Proposition

Falling stocks, rising rates and a strengthening dollar are all signs the central bank’s plan is working.

(Bloomberg Opinion) -- It’s been a tough few weeks on Wall Street. Equity markets have struggled, with the S&P 500 Index down almost 10 percent from its Sept. 20 record high before finally finding what may be a floor. As is always the case when stocks struggle, market participants start to doubt the Federal Reserve’s resolve. Don’t.

While the turmoil has triggered a small reduction in the market’s pricing of Fed interest-rate increases going forward, the tumble in stocks falls short of that necessary to dissuade the central bank from continuing its path of gradual hikes. Barring a more significant disruption in financial markets, the Fed will resist sending dovish signals as long as labor market strength looks likely to continue. Incoming data suggests this continues to be the case.

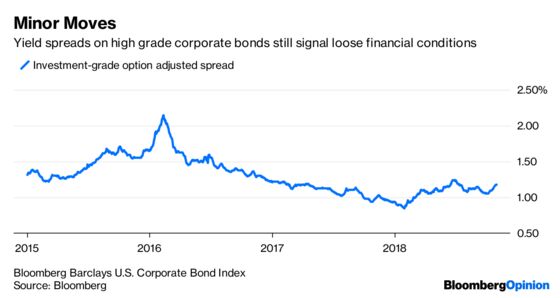

Falling stocks, rising rates and a strengthening dollar are all signs that the Fed’s plan to tighten financial conditions is working. Even so, financial conditions remain loose relative to crisis level standards, and loose even relative to the 2015-16 disruption that stayed the Fed’s hand. Then, corporate debt yields rose dramatically relative to U.S. Treasuries. Recent moves are minor in comparison.

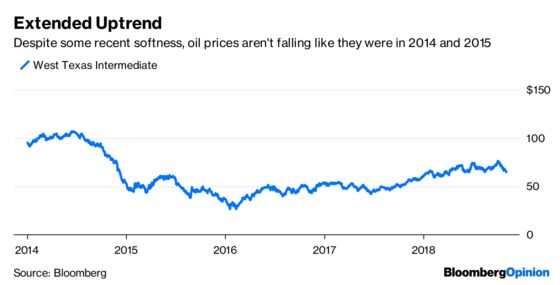

Then, oil prices were collapsing. Now, oil has been in an extended uptrend.

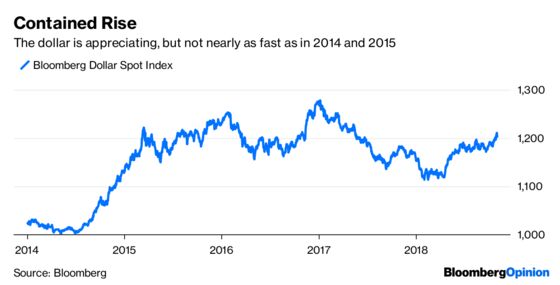

Then, the dollar surged. Now, the dollar’s rise is much more moderate.

Then, inflation expectations were falling. Now, they are stable.

In short, a look beyond the equities markets does not reveal a widespread pattern of financial tightness that one would normally associate with an economic disruption or recession. Moreover, central bankers are probably happy to see some steam come out of the stock market. The key to a sustained expansion is avoiding the buildup of imbalances such as asset bubbles that would threaten economic stability.

While Fed Chairman Jerome Powell and his fellow policy makers want to avoid sending signals that breed excessive pessimism in financial markets, they also want to avoid excessive optimism. Switching to a dovish stance in the wake of every correction in the stock market would favor the latter. And most importantly, incoming data do not point to a shift in the economy that would be inconsistent with the Fed’s forecast that tight labor market conditions will persist for a considerable period of time.

Gross domestic product grew at a 3.5 percent rate in the third quarter, supported by a 4 percent pace of consumer spending. Consider this number in light of the Fed’s median estimate of longer-run growth of 1.8 percent. This means that the economy operates at a pace likely to put further downward pressure on unemployment, and will continue to do so even if economic activity slows as anticipated in 2019. Labor market tightness won’t dissipate quickly, so don’t count on a slowing economy alone to persuade Powell to pull his foot off the brakes.

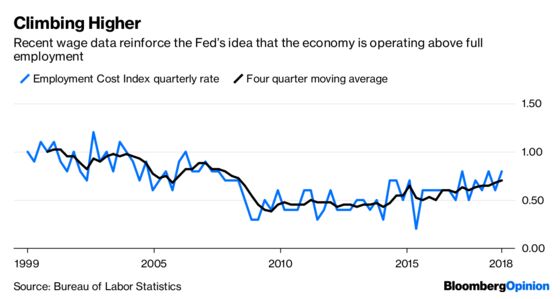

Moreover, recent wage data will only reinforce the Fed’s suspicions that the economy currently operates above full employment. While not yet excessive, wage growth is clearly climbing higher. The Employment Cost Index report for the third quarter released Wednesday confirmed that trend.

Despite persistently tight labor markets, inflation has yet to take off and instead sits comfortably at the Fed’s target. From the Fed’s view, this is not reason to change the policy path. Policy makers will tend to view tame inflation not as a reason to stop boosting rates, but as a reason not to accelerate the pace of rate hikes. Central bankers might argue that past rate increases are the reason the inflation rate isn’t higher.

Remember, Fed policy has always been about preemptive rate hikes to stave off inflationary pressures or financial imbalances. If successfully executed, neither should emerge to a degree that threatens the expansion. From the Fed’s point of view, so far, so good.

Altogether, this means that market participants should keep their eyes on the interplay between incoming data and the Fed’s forecasts. The Fed will most likely continue to raise rates until central bankers become confident that they have tightened the screws enough to slow activity to what they view is a more sustainable pace. Even after the equity market tumble, we aren’t yet at that point.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Duy is a professor of practice and senior director of the Oregon Economic Forum at the University of Oregon and the author of Tim Duy's Fed Watch.

©2018 Bloomberg L.P.