Xerox’s Higher Bid Might Be Enough to Bring HP to the Table

(Bloomberg Opinion) -- In the lumbering takeover battle for HP Inc., Carl Icahn-backed Xerox Holdings Corp. had been wielding plenty of stick, so it was about time for some carrot. What came was more of a crudite, but it might just be the appetizer that HP needs.

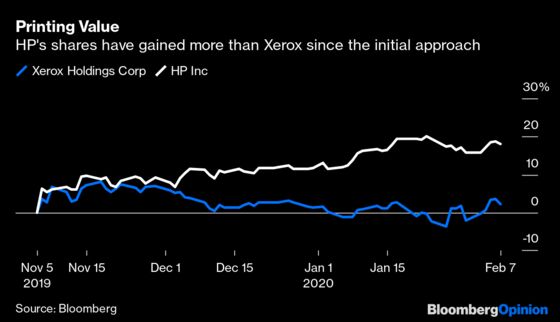

In the three months since Xerox’s initial bid, Icahn, who’s already the biggest investor in Xerox, took a 4% stake in HP. Xerox started a proxy fight for control of HP’s board and lobbied shareholders directly for support. On Monday, it finally improved the terms of the bid, increasing its offer to $24 a share from the initial $22.

The bump may not be enough to get a deal over the line, but it ought to at least give HP Chief Executive Officer Enrique Lores good reason to start formal talks. So far, HP has rejected the approaches and declined to negotiate. Should he do so now, he does so in the knowledge that he still has a stronger hand than his Xerox counterpart, John Visentin.

The extra $2 a share translates to a price increase of a little more than $3 billion, valuing HP at $35 billion excluding debt. And debt is a sticking point. As it stands, the Palo Alto, California-based company has very little of it: Net debt represents just 0.1 times earnings before interest, taxes, depreciation and amortization. To fund the acquisition, Xerox would most likely increase debt at the combined entity to more than four times Ebitda, essentially using up HP’s own debt capacity. HP could just as readily buy back its own shares and end up with a lower debt-to-Ebitda ratio than it would after a Xerox deal.

That’s why the higher offer looks like Xerox’s best effort to get HP just to engage. Is there an industrial logic to the two firms tying up? Yes. The printer market is in structural decline, so combining resources makes sense, assuming regulatory approval isn’t an issue, which is a question mark.

But if the argument is one of industrial logic, is it in the interest of the companies’ investors, which will both own a stake in the combined entity, to emerge with a significantly bigger debt pile to service? Probably not. Creating additional revenue, achieving cost synergies and maintaining investment-grade ratings could be challenging, according to Bloomberg Intelligence analyst Robert Schiffman.

It has always looked as if Xerox was just as interested in being acquired as it was being the acquirer, as I wrote in November. The fact that HP shareholders would own 49.95% of the combined entity under the latest offer, up from 48.9 % in the initial bid, seems to indicate which way the conversation is likely to head should serious negotiations begin. Lores will now find it easier to fight for more prominence for HP and its team and try to avoid the unpleasant distraction of a proxy fight.

As it outlined the strategic logic for the deal, Xerox might have made its life more difficult by identifying about $2 billion in savings from combining operations. If that’s true, then it might afford more than the $24 a share on the table based on the net present value of those savings.

But compared with HP’s undisturbed share price before the approach was first reported, Xerox is now offering a premium of more than 40%. That should be more than enough to move things along, even if Lores still has good reason to walk away.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2020 Bloomberg L.P.