What It Means When Markets Ignore Goldman Sachs

(Bloomberg Opinion) -- There was a time when a bold call from Goldman Sachs Group Inc. moved markets worldwide. Lately, not so much, judging by the action on Wednesday, and that says a lot about where investors’ mindsets are these days.

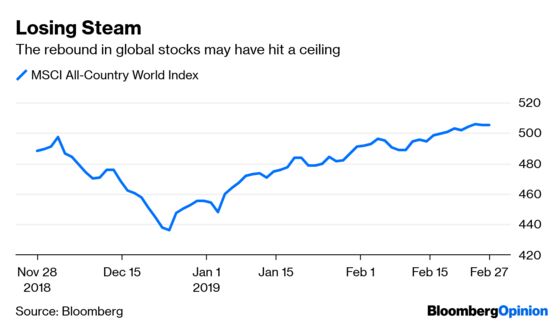

What’s interesting is that Goldman’s chief economist, Jan Hatzius, came out with a report saying the global economy may have already bottomed judging by the firm’s current activity indicator for February. “Some green shoots are emerging that suggest that sequential growth will pick up from here,” Hatzius and colleague Sven Jari Stehn wrote in a research note dated Tuesday. The best the MSCI All-Country World Index of stocks could do was end the day unchanged. To be sure, this is not to say that Goldman’s influence is waning. Rather, it’s more about the growing realization among investors that 2019 is still going to be a tough year for the global economy regardless, and it’s going to be awfully hard to build on the 11 percent gain that the MSCI All-Country World Index has delivered since the end of December. Indeed, the Goldman economists added that the risks to its global GDP forecast of 3.5 percent for 2019 “is probably still on the downside.”

Consider State Street Global Markets’ monthly index of global institutional investor confidence. After plunging to a record low of 69.4 for January, the firm said Wednesday that the index was basically unchanged at 70.9 in February. To put those numbers in context, the index only got as low as about 82 during the financial crisis and was above 100 — the level at which investors are neither increasing nor decreasing their long-term allocations to risky assets — as recently as last summer. The measure has some authority because unlike survey-based gauges, it’s based on actual trades and covers 15 percent of the world’s tradeable assets.

DEBT TRADERS HAVE NO DEBT CONCERNS

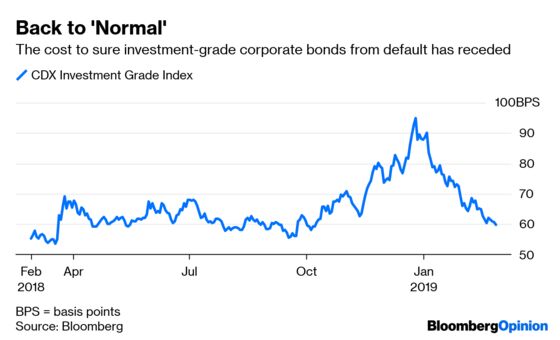

For all the hand-wringing over the rising level of corporate debt, those with the most at stake don’t seem to mind. About nine investment-grade rated issuers including Stanley Black & Decker and Huntsman International were in the market on Wednesday seeking to raise funds. Some strategists blamed the activity for reducing demand for U.S. Treasuries, which fell. That’s the opposite of what might be expected to happen if bond traders were truly worried that companies would have a harder time servicing their debt. At the heart of the issue is the more than doubling of the size of the U.S. investment-grade debt market since 2008 to about $5 trillion. About half is composed of bonds in the triple-B tier — those with BBB+, BBB or BBB- ratings — which have more than tripled. It’s here, in the lowest investment-grade category, where investors are most worried because anything rated BB+ or lower is considered junk. But as East West Investment Management market strategist Kevin Muir noted in a blog post, company executives would most likely divert cash from buybacks and dividends to paying down debt if it looked as if their credit ratings were in jeopardy of falling below investment grade. In fact, S&P Global Ratings said this month that only 27 issuers globally were downgraded to junk in 2018, the fewest since 2014. Junk bond investors also don’t seem too worried about the market suddenly being swamped with so-called fallen angels. The largest junk bond exchange-traded fund is experiencing its biggest cash injection in two years in February, with $1.6 billion flowing into the $16.1 billion iShares iBoxx High Yield Corporate Bond ETF, according to Bloomberg News’s Reade Pickert.

OIL TRADERS SHOULD BRACE FOR MORE TWEETS

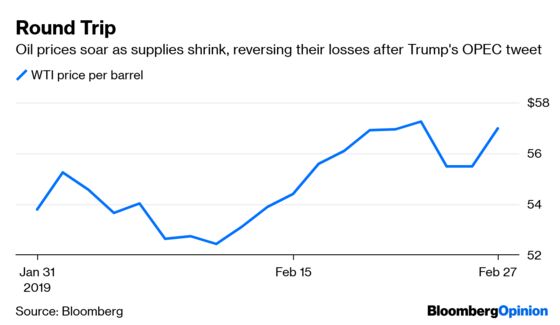

Crude oil tumbled 3.11 percent on Monday after president Donald Trump tweeted that prices were too high and called on OPEC to “relax and take it easy.” Perhaps Trump’s tweet was misguided and he should have actually directed his comments toward U.S. producers. That’s because oil recouped most all of its losses from Monday by surging as much as 3.41 percent in its biggest gain in almost a month after government data showed U.S. stockpiles plunged when the U.S. has become a net oil exporter. In other words, why aren’t U.S. producers opening the spigots like Trump wants? Overall, domestic oil inventories slid by 8.65 million barrels last week, twice the decline foreseen in a bullish industry report a day earlier, according to Bloomberg News’s Alex Nussbaum. The oil market is complicated, and the U.S. still imports lots of crude. The report from the Energy Information Administration said oil imports to the U.S. fell to a two-decade low, with shipments from Saudi Arabia the smallest on record. Prices have rallied about 26 percent this year as OPEC and Russia orchestrated production cuts and Venezuela’s political crisis restricted supplies further, Nussbaum reports. “No matter how you cut it, a draw of 8 million during turnaround season is a gigantic number,” Bob Yawger, director of futures at Mizuho Securities USA, told Bloomberg News. The U.S. imported 5.92 million barrels of crude last week, the lowest level since 1996, the EIA said. The decline in foreign shipments and increase in demand for refined products overshadowed American shale oil production that hit yet another weekly record.

RUSSIAN BONDS ARE IN HIGH DEMAND

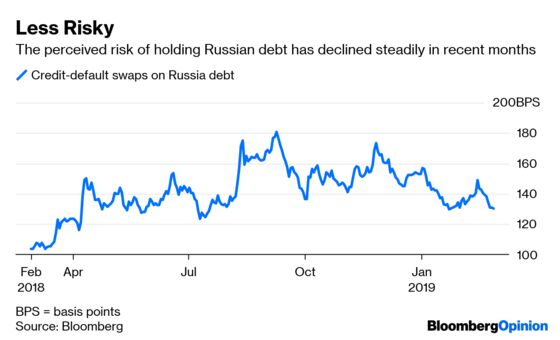

Maybe it had something to do with the outlook for higher oil prices, but Russia is finally getting some love from the bond market. Russia scored its biggest local-debt auction on record, and foreigners boosted their holdings of the debt for the first time in almost a year, even as the threat of U.S. sanctions lingers, according to Bloomberg News’s Artyom Danielyan and Olga Voitova. The nation’s Finance Ministry sold a total of 57.6 billion rubles ($875 million) in two offerings on Wednesday, with demand for both exceeding the amount offered. Also on Wednesday, the central bank published data on bond holdings for January, which showed foreigners increased their share to 25 percent, the first gain since March. Russia’s local debt has handed investors an 8.2 percent return so far this year, the most among developing nations after Egypt. That’s a big turnaround from September, when Russia was forced to cancel a number of debt auctions as sanction concerns soared. “The strong demand was expected and to an extent it confirms our theory that the American sanctions are already priced in,” Alexey Pogorelov, an analyst at Credit Suisse, told Bloomberg News. The ruble has appreciated 5.98 percent this year, the best in emerging markets behind only the Chile peso’s 6.57 percent gain.

INDIA GLASS IS HALF FULL OR HALF EMPTY

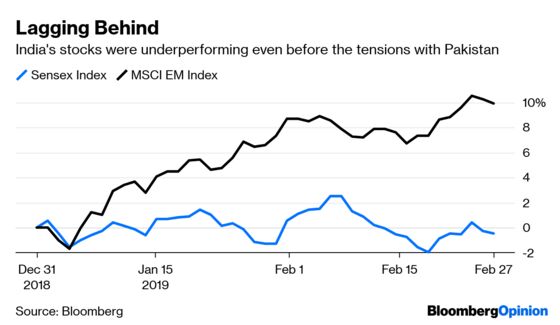

Rising tensions between Indian and Pakistan — two nations with nuclear capabilities — is having little impact on their financial markets. To recap, Pakistani fighter jets on Wednesday struck at targets inside Indian-controlled Kashmir, prompting both nations to close down large swaths of airspace. That came a day after India bombed a major terror camp inside Pakistan. So what has India’s rupee done? It weakened all of 0.24 percent to 71.24 a dollar on Wednesday. That’s still stronger than last year’s low of 74.4825 a dollar in October. The Sensex index of Indian stocks declined 0.19 percent, leaving it little changed on the year. Although Indian stocks haven’t fallen, they’re lagging far behind the MSCI Emerging Markets Index, which is up about 10 percent. The rupee’s 2.07 percent drop in 2019 compares with the 2.25 percent gain in the MSCI EM Currency Index. Besides tensions with Pakistan, other reasons for India’s underperformance include rising oil prices and uncertainty surrounding pending elections, according to Bloomberg News’s Kartik Goyal. The seeming stability in India’s markets “might be a little deceiving,” Simon Derrick, the chief currency strategist at BNY Mellon, wrote in a research note Wednesday. “It’s noticeable that the Sensex has struggled over the past four months to regain the losses it sustained between August and October of last year. Moreover, since mid-December our (money flow) data show foreign investors have been losing faith in the local equity market while the surge of money back into the (rupee) since the start of November appears to have run out of steam.”

TEA LEAVES

The U.S. fourth-quarter gross domestic product report will finally be released on Thursday, a month late because of the government shutdown. The median estimate of economists surveyed by Bloomberg is for growth to have slowed to a 2.2 percent annual rate in the final three months of 2018 following the best back-to-back gains since 2014. But don’t expect markets to spend too much time poring over the numbers, as the focus is now on how this quarter is doing. In that regard, economists are rapidly slashing their forecasts. The median estimate in a Bloomberg survey is for the economy to expand 1.98 percent in the January through March period. At the start of the year, the forecast was for 2.30 percent growth. And it doesn’t get much better as the year goes on, with estimates of 2.5 percent for the second quarter, 2.2 percent in the third and 1.9 percent in the fourth.

DON’T MISS

Tech Can’t Drive U.S. Economy Forever. What’s Next?: Conor Sen

Macron-Style Capitalism Is Taking Over in Europe: Lionel Laurent

Convertible Bonds Are Finding Their Sweet Spot: Brian Chappatta

U.S. Should Grab the Talent China Is Driving Away: Noah Smith

Matt Levine’s Money Stuff: Who Can Say What California Means?

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.