WeWork Gets a Visit From Financial Reality

Gulf investors backing Vision Fund seem to have decided that WeWork is not a tech bet but an aggressive punt on real estate.

(Bloomberg Opinion) -- The tech bubble’s financial backer of last resort, the $100 billion SoftBank Vision Fund, seems to be having second thoughts about its role as booster-in-chief of very expensive and very unprofitable startups. That’s healthy for the fund. But it must be troubling for the various companies and industries that were relying on its largess — not least the real-estate sector.

The bridge too far appears to be WeWork Cos. Inc., the fast-growing $20 billion shared-office-space provider that masquerades as a “physical social network.” While SoftBank Group Corp.’s founder Masayoshi Son and his backers in the Gulf region had been expected to splurge $15 billion to $20 billion on a majority stake in WeWork, the Financial Times has reported that the plan is now for a more miserly $2 billion. The Vision Fund, a kind of gargantuan private equity shop run by Son and SoftBank, is no longer expected to take part.

The plaid-clad entrepreneurs who populate WeWork’s offices haven’t suddenly lost all their appeal for the big money crowd; $2 billion is still a princely sum and shouldn’t lead to a dreaded “down round” — Silicon Valley-speak for a valuation discount — according to the FT. SoftBank has already poured $4.4 billion into WeWork alongside the Vision Fund. Taking into account other commitments from the Japanese company, including convertible debt, warrants and the latest $2 billion, the total comes to more than $10 billion.

Still, the fact that SoftBank’s shares rose almost 6 percent because of the much smaller new investment shows investors are mightily relieved about Son’s sudden bout of prudence. Understandably so, given the recent gyrations in the markets and the tech industry in particular. And while WeWork’s $20 billion or so implied valuation appears untouched, there are plenty of other alarm bells ringing around the New York-based startup.

The Vision Fund’s investment model depends on deploying huge amounts of cash to companies that are growing extremely quickly. WeWork no longer seems to fit the bill, and that should worry people. This is a firm whose valuation only really makes sense if it grows at double-digit rates for years to come, while managing to maintain its rental prices even if the era of cheap financing comes to a halt.

The Gulf investors backing the Vision Fund seem to have decided that WeWork is not a tech bet but simply an aggressive punt on real estate. They “have told SoftBank executives they would prefer the fund stick to technology bets,” according to the WSJ. That’s got to hurt.

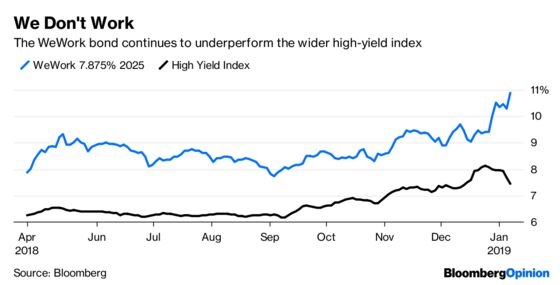

There’s another way too, beyond SoftBank’s valuation, of looking at how the market judges WeWork’s prospects. The office space provider issued a seven-year unsecured high-yield bond last April, which has dropped 14 percent in value subsequently and is doing worse than the broader high-yield index (as the chart above shows). Given WeWork’s opaque financials and its self-made metrics such as “community-adjusted Ebitda,” you can see why investors might be rethinking a company that has relied a lot on confidence, optimism and faith.

While there’s no doubt a sober message here for Silicon Valley optimists, there’s also one for markets at large. This might be a turning point not too dissimilar to past real-estate bubbles. In 2007, Blackstone splashed $39 billion on a portfolio of commercial property including debt, only to begin selling off assets soon after. Lehman Brothers’ forays into real estate didn’t go so well. With WeWork already occupying swathes of our big cities, it’s hard to see how its ambitions get dented without more far-reaching consequences.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering Brussels. He previously worked at Reuters and Forbes.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.