(Bloomberg Opinion) -- It’s hard to imagine sentiment being any worse than it was coming into this week. The Dow Jones Industrial Average was down 35% from its high for the year in February, and more than a few Wall Street strategists were calling for a drop of 50% or more before it was over. What a difference a few days make. The benchmark briefly entered a (technical) bull market on Thursday, rising 20% over the course of three days from its lows on Monday. False rallies are a hallmark of bear markets, and this could be one of those, but this turnaround has one big thing going for it.

Rather the some sudden confidence in the battle against the coronavirus pandemic and a subsequent quick rebound in the economy and corporate profits, much of the recovery in stocks can be tied to the dollar. As equities have soared the past three days, the Bloomberg Dollar Spot Index, which measures the greenback against a basket of major currencies, has tumbled some 3.78% from a record high after surging 8.91% the previous two weeks. Considered a haven, it’s not unusual for the dollar to strengthen in times of crisis. The problem is, the global financial system is tied to the dollar like never before, and its appreciation causes financial conditions around the world to tighten. The most visible example is in the debt markets, with the Institute of International Finance estimating that emerging-market borrowers alone have $8.3 trillion of foreign-currency debt, the bulk of it in dollars, up more than $4 trillion from a decade ago. So, any rise in the dollar makes it that much more expensive for these borrowers to make interest payments or refinance, which would only exacerbate the deep recession already facing the global economy.

Much of the dollar’s recent weakness can be tied to one key move by the Federal Reserve to ease the run on the U.S. currency. What the Fed did was provide foreign-exchange swap lines with central banks in both developed and emerging markets, offering dollars in exchange for their currencies. The dollar “may now become a barometer of the efficacy of the policy response to corporate credit difficulties, interbank funding challenges, etc.,” Standard Chartered currency strategists Eric Robertson and Steve Englander wrote in a research note. “Global policy makers have adopted a ‘whatever it takes’ approach to countering financial-market volatility and the expected recession, but this response may also need to have an impact on the (dollar) to be seen as truly effective.”

THE ‘SMART MONEY’ BELIEVES

There’s a school of thought on Wall Street that trading in the first 30 minutes after equity markets open represents emotions, driven by greed and fear of the crowd based on news, as well as a lot of trades based on previously set-up market orders. The “smart money,” though, waits until the end of trading to place big bets, when there is less “noise.” This action is what the Smart Money Flow Index tries to capture as it relates to the Dow. What’s encouraging is that this gauge has just risen back to pre-crisis levels, suggesting big institutions are more confident that perhaps equities have reached fair value. It’s also notable that Deutsche Bank AG equity strategist Binky Chadha, who called the S&P 500 Index’s surge higher in 2019, then pivoted to forecast no gain at all in 2020 before the coronavirus crisis hit, is turning more bullish — or at least less negative. Chadha just boosted his recommended equity allocation to “neutral” from “underweight,” according to Bloomberg News’s Joanna Ossinger. Among the main reasons for his shift, Chadha pointed out that equities’ peak-to-bottom decline was in line with historical patterns and that positioning was at a record low.

BRING IT ON

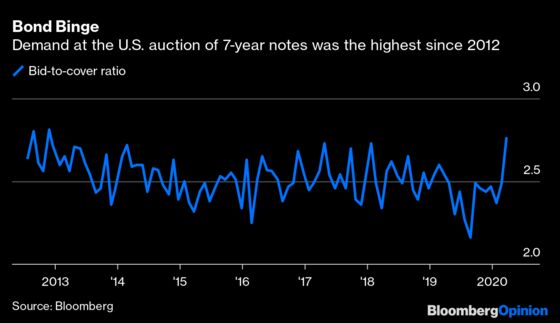

Usually it could be a warning sign when demand soars at an auction of U.S. Treasury securities. After all, Treasuries are the ultimate haven asset, and a rush into them may signal tough times ahead for the economy. So how should Thursday’s auction of $32 billion of seven-year notes be interpreted? Investors bid for 2.76 times the amount offered, the highest so-called bid-to-cover ratio since the height of the European debt crisis in 2012 and a big jump from the 2.49 times at last month’s sale. Yes, there is still a lot of concern about the future of the economy, but perhaps the jump in demand signals that the government will have no problems selling as much debt as needed to fund the $2 trillion rescue package. There’s even evidence of optimism in the corporate bond market, where the cost to insure investment-grade company debt from default has fallen for four consecutive days to the lowest since March 6. It has fallen three days for junk bonds. Not only that, Bloomberg News reports 34 issuers in the U.S. and Europe were in the market selling debt on Thursday, making it the busiest day in months. They wouldn’t be selling if there was no demand.

COMMODITIES AS THE OUTLIER

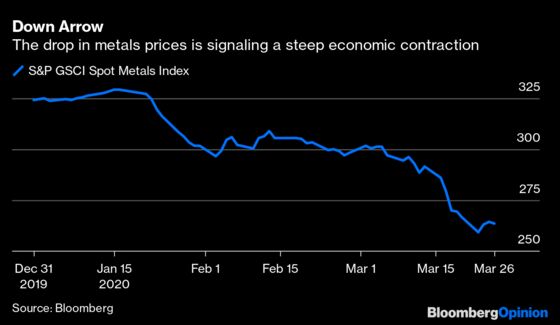

The market for raw materials doesn’t seem to have received the memo. Some investors feel there won’t be a real recovery in markets until oil prices begin to rise, bolstering the cash flow of many U.S. energy firms that are now in jeopardy of defaulting after West Texas Intermediate crude plunged from more than $60 a barrel in January to as low as about $20 this month before trading at $22.78 Thursday. And it’s not just oil. Bloomberg Economics notes that metals consumption moves closely in line with global gross domestic product growth. As a result, the economists note that metals prices can provide a high-frequency guide to the ups and downs in the economy. “The fit is so strong that Bloomberg Economics uses the S&P GSCI Metals Price Index in our global GDP nowcast,” Tom Orlik and Niraj Shah wrote in a research note Thursday. “A 13% drop in the index since the start of March shows markets pricing in a sharp decline in activity.”

TEA LEAVES

The news out of Italy has been grim. The nation reported the most coronavirus infections in the last five days on Thursday, even after weeks of rigid lockdown rules. The civil protection agency reported 6,153 new cases on Thursday, bringing confirmed cases there to 80,539, which is a level approaching China’s. On Friday, we’ll get some sense of what this is doing to consumer confidence when data for March is released. The median estimate of economists surveyed by Bloomberg is for a drop to 100.4, which would be the lowest since December 2014 from 111.5 in February. Such measures will likely gain in importance in the months ahead because market optimists are banking on consumer confidence rebounding quickly once the coronavirus pandemic slows. But no one knows when that will be and whether consumers will have the confidence — or the resources — to go about life as they did before Covid-19.

DON’T MISS

What More Could the Federal Reserve Possibly Do? A Lot: Tim Duy

Euro-Zone Rescue Talks Are Irrelevant: Ferdinando Giugliano

We Can’t Dismiss This Rebound as a Reflex Action: John Authers

Dollar Crunch Is Europe’s Gift to Asia: Gopalan and Mukherjee

Matt Levine’s Money Stuff: Nobody Wants a Margin Call Right Now

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2020 Bloomberg L.P.