(Bloomberg Opinion) -- Among the biggest economic stories in the U.S. over the past couple of decades has been the increasing concentration of wealth in a few “superstar” metropolitan areas. Recently, many people — myself included — have been looking hopefully for signs that maybe the situation is changing at least a little. One place to look is in the venture capital data, since VC investment presumably presages future growth. But most VC investment in 2018 went to … the same places it’s been going for a while now.

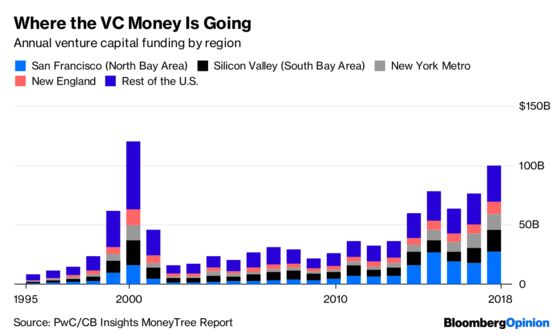

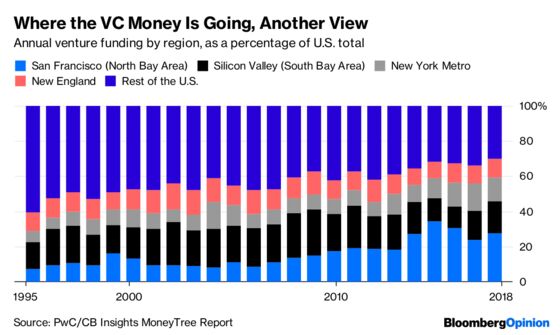

This is from the PricewaterhouseCoopers/CB Insights MoneyTree report, the fourth-quarter-2018 edition of which was released Monday. It showed 2018 to be the second-biggest year for venture capital investment in U.S. history — with the $99.5 billion invested topped only by the $120 billion ($175 billion in 2018 dollars) invested at the tail end of the dot-com frenzy in 2000. But only about 30 percent of 2018 VC investment landed outside the superstar metros of San Francisco, San Jose, New York and Boston. (The regions that PwC sorts VC activity by — the ones in the chart — aren’t the same as the metropolitan areas used in government statistical data, but these four are close-ish.) That’s down from 61 percent back in 1995, and 34 percent in 2017.

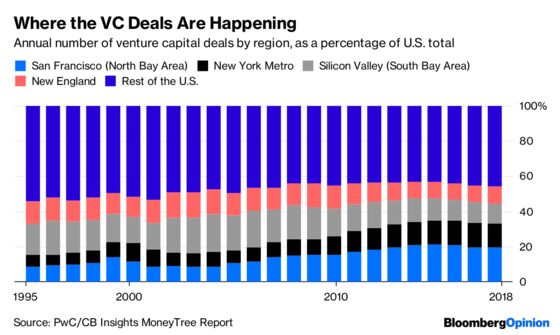

Big, late-stage deals have been making up a growing share of VC activity lately, meaning that a lot of this money is going to companies that can no longer really be described as startups. For a somewhat more forward-looking, startup-oriented view, then, here’s the data sliced by the number of deals instead of the dollar amounts.

This makes things look a bit better for the rest of the country. The share of VC deals going outside the superstar regions is still smaller than it was in the 1990s and early 2000s, but it’s the biggest it has been since 2007. The rest-of-the-U.S. regions that have gained the most ground since then: the Midwest (which by PwC’s definition includes the tech hotbed of Pittsburgh), up from 5.7 percent of all deals in 2007 to 7.7 percent in 2018, and Los Angeles/Orange County, up to 7.6 percent from 6 percent. But nine of the 15 rest-of-the-U.S. regions have actually lost deal share since 2007, and the two regions with by far the largest deal-share gains have been San Francisco and New York.

The two biggest regional developments in U.S. venture capital over the past decade, then, have been activity shifting northward in the San Jose/San Francisco Bay Area (PwC’s main dividing line between San Francisco and Silicon Valley is Route 92, which crosses the bay on the San Mateo Bridge) and New York City establishing itself as a major center of startup activity. If you just look at the last five years, San Francisco’s dominance has slipped a little, and more rest-of-the-U.S. regions have made gains. But overall, the VC data still seems mainly to show how resilient the superstars remain.

To contact the editor responsible for this story: Brooke Sample at bsample1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Justin Fox is a Bloomberg Opinion columnist covering business. He was the editorial director of Harvard Business Review and wrote for Time, Fortune and American Banker. He is the author of “The Myth of the Rational Market.”

©2019 Bloomberg L.P.