(Bloomberg Opinion) -- I have been arguing for some time that the Federal Reserve should run the U.S. economy “hot” by keeping interest rates low even after unemployment falls below its so-called natural rate. Not everyone agrees with me, to put it mildly. One of the more thoughtful critiques came this week from Raphael Bostic, president of the Atlanta Fed.

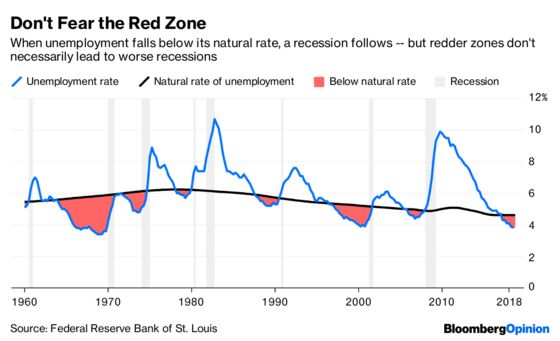

In a speech to a business group in Louisiana, Bostic defended the Fed’s policy of raising rates to help prevent a recession. As evidence, he presented a version of the chart below, which he called “a picture worth thinking about.”

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a senior fellow at the Niskanen Center and founder of the blog Modeled Behavior.

©2018 Bloomberg L.P.