(Bloomberg Opinion) -- Reality is beginning to bite in the FTSE 100 as some high-yielding stocks give up on generous dividends. But many British companies are still continuing to offer jaw-dropping payouts when what investors really crave is growth.

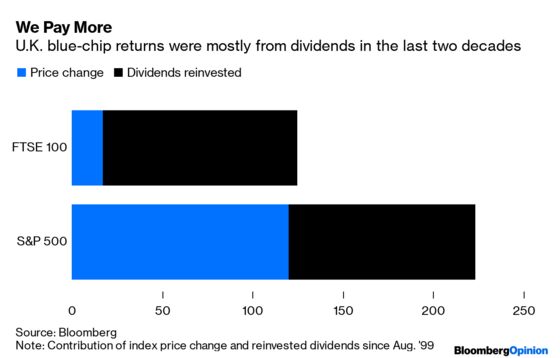

The dividend culture of the FTSE 100 has long been an oddity. Its investors have received a far higher proportion of their total returns from income over the last two decades than if they had invested in, say, the S&P 500 over the same period.

With dividends a very British symbol of corporate confidence, boards are reluctant to cut them even when it might be wise to do so. So the FTSE 100 culture has been self-reinforcing.

This year has brought some signs of change. Centrica Plc slashed its payout last week. Analysts had expected the utility to announce a deep cut, but not by nearly 60%. Vodafone Group Plc snipped its dividend in May. And last month, tobacco giant Imperial Brands Plc dropped a commitment to grow its payout 10% annually.

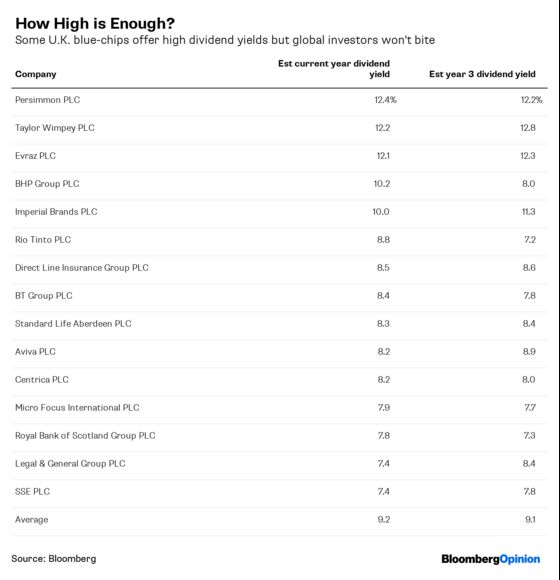

Yet even now, these companies’ share prices look superficially cheap on a dividend basis, with yields (the dividend divided by the share price) of between 6% and 10%.

Indeed, such ratios are nowadays pretty common in the U.K. The average dividend for the top 15 highest-yielding stocks is worth 9% of the share price. The standard explanation – that this signals dividend cuts in the coming years – doesn’t fit very well. Take analysts’ predictions for dividends in three years; even with some cuts forecast, the average yield for this group is still 9%.

This is especially odd in a low-rate environment. Yields on some government bonds and high-rated corporate debt are negative or zero. Surely income investors would buy these dividend stocks if the return provided by their annual cash payouts was only 5% rather than double that level? Wouldn’t that provide sufficient compensation for the added risk?

One explanation is simply that international investors just don’t care for yield anymore. Domestic U.K. income funds probably would be willing to pay more for these stocks and bid down their yields. But this group isn’t driving the market. Global investors are. They covet growth and don’t want exposure to the U.K. until there’s clarity about Brexit. The average expected increase in sales over the next two years for the top-15 yielding U.K. blue-chip stocks is under two percent.

Of course, if the companies aren’t growing, it’s likely because of past under-investment caused by overly-generous dividends. But cutting dividends now to invest in growth won’t pay off for some time and would only infuriate the small pool of domestic investors who actually like the income. Meanwhile, global investors sit on the sidelines and company managers stand frozen like a deer in the headlights.

To contact the editor responsible for this story: Stephanie Baker at stebaker@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.