(Bloomberg Opinion) -- Remember the big corporate tax cuts of 2017? Wonder how they’re doing? Not so well, judging from the latest government data on the U.S. economy.

When President Donald Trump signed the cuts into law in December 2017, there was a lot of talk about how they would affect jobs and wages. But the real test of their effectiveness is whether lower rates encourage companies to invest more in things like factories, equipment and innovation. Such investment would both boost growth immediately and increase the economy’s productive capacity in the longer term.

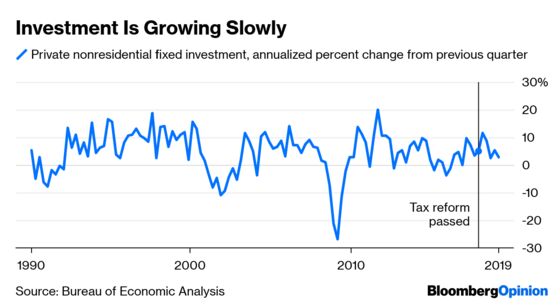

So what’s happening? The relevant measure — private fixed nonresidential investment — accelerated a bit in the first half of 2018, but has since slowed significantly. In the first three months of 2019, it was up an annualized 2.7 percent, well short of the 5.3 percent average for the current expansion. Here’s how that looks:

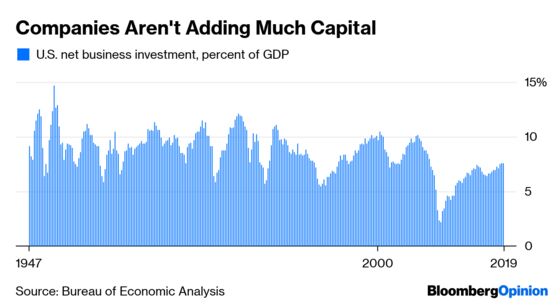

Worse, the meager growth is coming from a low level. Consider the amount by which capital spending exceeds depreciation — that is, compensates for the aging of previous investments and actually adds to the country’s capital base. In the first three months of 2019, this net investment amounted to $1.6 trillion, or 7.6 percent of gross domestic product — higher than in recent years, but still low compared with other economic expansions.

Granted, it’s possible that the level doesn’t reflect the potential of the investment. Maybe companies are putting their money into new-economy projects that, like Twitter or WhatsApp, aren’t as capital-intensive as, say, a tractor factory. Or maybe advanced technologies will allow them to get a lot more bang for each buck.

Barring such a paradigm shift, though, the investment picture isn’t encouraging. The federal government will have to borrow an added $1 trillion through 2027 to pay for the corporate tax breaks. So far, it’s hard to see what the country is getting in return.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Whitehouse writes editorials on global economics and finance for Bloomberg Opinion. He covered economics for the Wall Street Journal and served as deputy bureau chief in London. He was founding managing editor of Vedomosti, a Russian-language business daily.

©2019 Bloomberg L.P.