Trump’s Stock Market Tweet Isn’t Entirely Bonkers

(Bloomberg Opinion) -- As the S&P 500 Index was headed toward its biggest decline since Oct. 24 on Monday, tumbling as much as 2.12 percent, President Donald Trump tweeted that recent reports of investigations that his administration could face from Democrats who recently won the majority in the House of Representatives were causing “big headaches” for the stock market. Although most pinned the weakness on declines in the shares of Apple Inc., General Electric Co. and Goldman Sachs Group Inc., Trump may not be entirely wrong.

Until a few weeks ago, a Republican-controlled government had been good for the stock market, with the S&P 500 rising 31 percent between the end of 2016 and its record high on Sept. 20. The gains came on the back of big corporate tax cuts and the Trump administration’s efforts to cut red tape for businesses by rolling back regulations. Of course, there were other reasons for the gains, but those were two primary ones. Now, though, market participants worry that if Democrats in the House and the Trump administration spend the bulk of their time issuing and answering subpoenas, there will be less of a chance of passing any kind of legislation that would benefit the economy. That goes for even anything having to do with infrastructure, which is one area that both sides seem to agree needs addressing. Put another way, political gridlock is no longer good for markets facing slower economic growth, tighter monetary policy, inflationary pressures and a slower earnings growth. “We’re skeptical that gridlock improves the 2019 story meaningfully,” Morgan Stanley Chief Cross Asset Strategist Andrew Sheets wrote in a research note on Sunday.

Bianco Research notes that the percentage of economies growing above their one-year average has tumbled to “a paltry” 30 percent, a level that in the past has been followed by “amplified volatility” across global equity markets. That doesn’t bode well for corporate earnings. Even though third-quarter profits exceeded expectations by rising about 25 percent from a year earlier, growth is forecast to slow to about 14 percent for this quarter, according to DataTrek Research, citing FactSet data. That’s still pretty good, but it’s below the 16.7 percent rate forecast at the start of earnings season.

DOLLAR STRENGTH IS AN ILLUSION

Anyone taking a quick glance at the dollar would be forgiven for thinking everything is great with the U.S. The Bloomberg Dollar Spot Index on Monday surged as much as 0.63 percent for its biggest gain since August. Also, the gauge is at its highest level since May. But rather than a reflection of U.S. might, the greenback seems to be benefiting in large part from the euro’s woes. The Bloomberg Euro Index fell as much as 0.68 percent Monday in its biggest decline since August, pushing the gauge to its lowest level since July 2017. The weakness in the shared currency came with the European Commission looking ready to escalate its budget battle with Italy. Traders fear that the string of soft economic data may force the European Central Bank’s Governing Council to lower its economic growth projections at its December meeting, according to Bloomberg News’s Vassilis Karamanis. Goldman Sachs now says that policy makers could be forced to delay the start of rate increases from the end of 2019 if the current slowdown becomes worse than anticipated. Goldman isn’t alone. UBS AG said last week that the ECB would only start increasing interest rates at the very end of 2019, nudging back its call to December from September. It also cut its euro zone growth forecast for next year to 1.6 percent from 1.8 percent. At Deutsche Bank AG, strategist Alan Ruskin says the question is whether the ECB join the global monetary policy normalization in 2019. If it doesn’t, there’s an “early short-circuiting” that “undermines a core part of the multiyear weaker dollar, stronger euro story.”

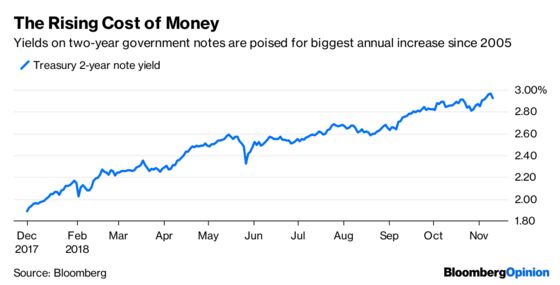

BOND MARKET FACES A TEST

The rising dollar wouldn’t be such as problem for the stock market if U.S. economic growth was accelerating, but it’s not. In fact, growth is forecast to slow to 3.1 percent this quarter and 2.9 percent in 2019 from 3.5 percent in the third quarter and 4.2 percent in the April through June period, according to the median estimate of economists surveyed by Bloomberg. Even so, that should still keep the Fed on its path of raising interest rates again in December and possibly three more times in 2019. “It wouldn’t be surprising to me that we would need to go up again in December and at least a couple of times next year,” Federal Reserve Bank of San Francisco President Mary Daly told Bloomberg News in her first interview on policy since she became head of the regional Fed branch on Oct. 1. “In my modal expectation, I think that’s what will be needed.” She voted for the first time at the Fed’s policy meeting in November and will vote again at the Dec. 18-19 meeting, at which officials are expected to hike for the fourth time this year, according to Bloomberg News’s Jeanna Smialek. Higher rates should support the dollar and weigh on bonds, pushing yields higher. Rising bond yields have also received a lot of the blame for the turbulence in stocks of late. Just last week, the average yield on U.S. bonds of all types reached 3.66 percent, the highest since the start of 2010. The bond market faces a test Wednesday when the government releases its Consumer Price Index report for October. The median estimate of economists surveyed by Bloomberg is that core consumer prices, which strip out food and energy, rose 2.2 percent from a year earlier, the third consecutive month it has risen by that amount. If it exceeds that level, then look for bonds to suffer and the dollar to gain, which would both be bad for stocks.

WHO’S IN CHARGE IN MEXICO?

No one is sure what to believe in Mexico these days. The country’s stock market tumbled late last week by the most since 2011 when officials in the political party of President-elect Andres Manuel Lopez Obrador, who is known as AMLO, floated the idea of eliminating fees on ATM cash withdrawals and balance requests, as well as commissions charged for printing bank balances and transfers to other banks. That’s good news for consumers but not so good for banks and the international investors who own their shares. AMLO quickly called a press conference on Friday to assure investors that there would be no banking law changes in the near future. But on Monday, Senate members of the Morena party backed the proposals, contradicting AMLO. Mexico’s benchmark stock index dropped as much as 2.47 percent to the lowest since March 2016. The peso fell as much as 1.18 percent against the dollar. “We have seen this sort of thing before when outsiders come to power,” Jan Dehn, the London-based head of research at Ashmore Group, which oversees $76 billion, told Bloomberg News. “Either AMLO shows them who is boss or he appears weak. These are teething problems, but it is important that AMLO handles them right.” As the strategist at Brown Brothers Harriman put it in a research note to clients Sunday, “it’s clear that markets had gotten to sanguine about political and policy risk in Mexico.” It will be interesting to see how the Bank of Mexico responds. It meets Thursday, and policy makers are forecast to raise interest rates by 25 basis points to 8 percent.

DIAMONDS ARE FOREVER. THEIR HIGH PRICES AREN’T.

It’s hard to find any business that is as tightly controlled as the one for diamonds. De Beers is the world’s biggest producer of diamonds and sells gems at 10 sales a year in Botswana to a select group of customers. The buyers are expected to specify the number and type of diamonds they want and then carry out the purchases at a price set by De Beers, according to Bloomberg News’s Thomas Biesheuvel. But an interesting thing happened on Monday. De Beers reduced prices by as much as 10 percent for low-quality stones in what may be the latest sign that the bottom end of the market is in turmoil, which seems to be weighing on the top end. The average price for a top 25 quality, 1 carat diamond with a clarity between internally flawless with no inclusions or marks on the surface to very slight inclusions has dropped to its lowest since January. That only serves to underscore how the diamond market has been in a funk for years now, with prices tumbling by almost half since 2011. While De Beers routinely changes prices at its sales, it has historically favored restricting supply as a tool to manage the market. The business of low-end diamonds, which tend to be small and flawed, is struggling because of too much supply. Top cutting centers, such as Surat in India, have been squeezed by lower profit margins and the depreciation of the rupee, which has lost more than 12 percent of its value this year. There’s also concern that De Beers’s introduction of man-made gems will add competition, especially at the bottom end of the market, Biesheuvel reports.

TEA LEAVES

Market participants may get their first sense of what a divided Congress has done to the psyche of American businesses when the National Federation of Independent Business releases its monthly sentiment index on Tuesday. The group’s small-business optimism index, which started in 1974, has soared to a record under the Trump administration. Some strategists think the gauge has been skewed higher under Trump because small-business owners tend to be Republicans. Whether that’s true or not, the respondents have clearly been stoked by lower corporate tax rates and deregulation efforts by the White House. But with the Democrats back in control of the House, it’s hard to see the corporate tax cuts becoming permanent or further efforts to deregulate companies and industries.

DON’T MISS

The Fed Policies Have Markets Staring at Purgatory: Tim Duy

Markets Will Continue Their Tug of War: Mohamed A. El-Erian

If OPEC Thought Its Job Done, 2019 Will Be a Shock: Julian Lee

Italy Gets Starvation Rations From Mario Draghi: Marcus Ashworth

There’s Less to Private Equity Than Meets Eye: Stephen Gandel

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.