Trump? Obama? No, Thank These Three for This Bountiful Economy

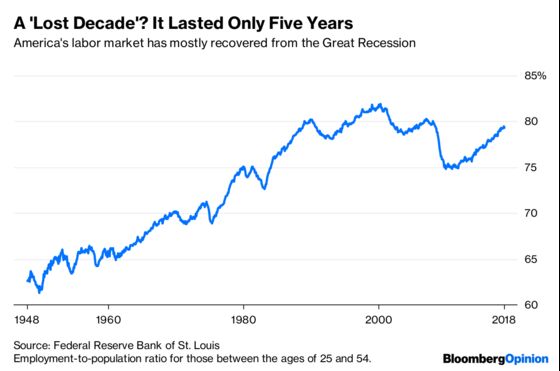

(Bloomberg Opinion) -- In economic terms, Americans have a lot to be thankful for this year. Unemployment is at record lows, more people are actually working (as opposed to dropping out of the workforce), and wage growth is improving for workers on the low end of the scale. Other countries, when recovering after a big financial crisis, have suffered though a “lost decade” of slow or negative growth. The U.S. appears to have lost only half a decade:

Some of this recovery, of course, is due to natural economic forces. Like a violin string that gets plucked by a finger, economies that suffer deeper downturns have more room to bounce back. The Great Recession probably caused the delay of many capital equipment purchases and other investments. Now that more favorable conditions prevail, firms are making up lost ground.

But policymakers can speed up the return of favorable conditions. So who, if anyone, should get credit for the relatively good times? Whom does America have to thank?

Supporters of President Donald Trump, of course, would like to think that he’s responsible. But the evidence for that is pretty slim. Yes, Trump signed a large tax cut in late 2017. Tax cuts can make an economy more efficient, as well as provide some Keynesian fiscal stimulus. Yet analysis shows no correlation between how big of a tax cut an industry got, and how much it boosted hiring and wages. That means that the tax cut has probably only been incidental to the health of the labor market. Meanwhile, Trump’s trade war is unlikely to help U.S. businesses.

There is at least one way Trump could be helping the economy: emotionally. Business sentiment boomed when Trump was elected, possibly as a result of perceptions that Trump is pro-business. Confident businesses tend to invest more. There is a danger that the confidence is unfounded. But for now, it could be adding a tailwind to investment.

If Trump’s role in the recovery has been modest at best, how about his predecessor? The recovery began in earnest during Barack Obama’s second term, and 2015 saw what was probably the strongest annual performance since the crisis. Obama fought hard to pass the American Recovery and Reinvestment Act of 2009, which provided a major fiscal stimulus.

The most important thing that stimulus did was provide money to cash-strapped state governments. That helped states bound by balanced-budget laws keep government workers on the payroll; had those workers been forced into the ranks of the unemployed, the recession would have been worse. European countries that responded to the crisis with austerity measures learned this lesson the hard way.

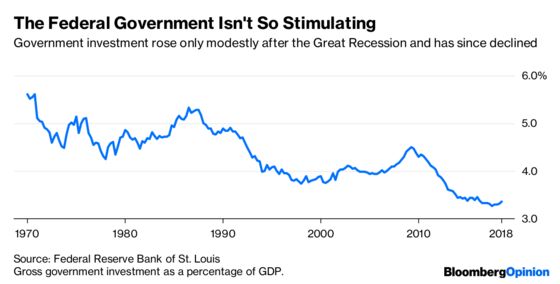

But overall, it was not a great stimulus bill. It was too small, for one thing. Too much of it went to tax credits, even though they are less effective than government spending at stimulating an economy in recession. Government investment, which is the most effective form of stimulus, rose by only a modest amount:

And although Obama’s stimulus helped prevent the Great Recession from becoming a slightly greater recession, its effect was spent by the time the recovery really took off. To his credit, Obama refrained from making the economy even worse. By the same token, the credit he gets for the good economic performance since 2014 should also be modest.

The real hero of the story is probably the Federal Reserve. When the crisis hit, Chairman Ben Bernanke didn’t hesitate. Motivated by his own research on the financial roots of recessions, he abandoned the Fed’s traditional cautious approach. He dropped interest rates to just about zero immediately. He helped save the banking system, using unconventional monetary policy to take huge amounts of toxic mortgage-backed assets off of banks’ balance sheets — assets that eventually turned a profit for the taxpayer.

But unlike fiscal policy, monetary policy didn’t let up. Despite frantic calls to raise rates to avoid creating inflation or financial instability — neither of which materialized — the Fed stayed the course, keeping rates at zero until late 2015 when it became clear a real recovery was underway. It also engaged in repeated rounds of quantitative easing, again in defiance of the skeptics; some of this probably did have the effect of boosting lending and the real economy.

So if you want someone to thank for America’s early exit from the economic hole it dug itself into in the 2000s, thank the Fed. Thank Ben Bernanke for swift and decisive action, and thank his successors, Janet Yellen and Jerome Powell, for maintaining a steady course. Without them, the U.S. might still be mired in a lost decade.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.