Trump’s Impeachment Is Already Hurting the Economy

His erratic response — and Democrats’ response to it — is increasing political and economic uncertainty.

(Bloomberg Opinion) -- The U.S. economy has been amazingly resistant to the weaknesses afflicting the global economy — until now. Dual threats arising from President Donald Trump and his 2020 Democratic rivals will test its resilience.

Major economic indicators in Europe and Japan have sagged this year, but the U.S. economy has remained startlingly healthy. On one level, this isn’t hard to understand: Congress passed a deficit-exploding tax cut in 2017 and has approved record increases in spending, both of which gave a shot in the arm to the economy.

The economy was so close to full employment, in fact, that many feared accelerating inflation and little extra growth. Both of these predictions were wrong. Real economic growth exceeded 3% in the middle of 2018 before falling back due to trade uncertainty, a slowing world economy and the U.S. Federal Reserve’s tightening monetary policy.

The Fed undoubtedly overreacted to the prospect of inflation over the last year. Yet its more recent about-face makes it among the most responsive central banks in the world. Its lowering of interest rates has cushioned the U.S. economy and even led to mini-revival in housing, the most cyclical part of the economy.

But the economy isn’t out of the woods yet — and it’s the executive branch weighing on the outlook.

First, there is the impeachment inquiry. It’s tempting to think that Trump’s impeachment may prove to be the same sort of non-event as Bill Clinton’s. This is mistaken. The possibility of impeachment chastened Clinton’s presidency, but it is driving Trump’s to distraction.

The president is becoming ever more erratic in his tweets. He is inflaming partisan tensions and driving uncertainty higher. Trump has said that a deal with China is imminent, but it’s impossible to see how this behavior improves his negotiating position. It’s also hard to see how an enraged Trump swallows his pride and accepts a deal from the Chinese that fails to achieve his ambitious and misguided goal of closing the bilateral trade gap.

Worse still, the president’s behavior may be driving Democrats to the left. As it seems more likely that Trump will self-implode, some Democratic candidates have released increasingly punitive tax plans. Even former Vice President Joe Biden is exploring the idea of a tax on Wall Street. This makes sense in an environment where Trump is aggravating partisan differences; the incentive for Democrats is not to cooperate with Republicans but to take advantage of growing anger on the left.

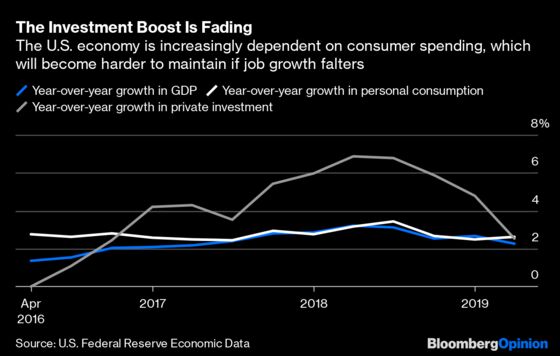

This combination — an erratic and impeachment-threatened Republican president, and his increasingly radical Democratic opponents — puts U.S. business in a double bind. Despite booming demand, now is not an ideal time to consider new major investments. Any CEO who can is surely trying to wait until after 2020.

That very caution, in turn, can sow the seeds of economic weakness. As companies continue to pull back, job growth may slow. Slowing job growth will weaken consumer spending, which will justify further retrenchment.

Is this sort of doom loop inevitable? No. It’s possible that the U.S. economy could stumble through the next few quarters without falling into recession. It’s possible that the Fed could cut interest rates still further. It’s even possible that Trump could become more quiet and focused. It’s not likely, however — and that should worry all Americans.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

©2019 Bloomberg L.P.