(Bloomberg Opinion) -- Federal Reserve Chairman Jerome Powell’s surprising — judging by the market’s reaction — statement that interest rates are “just below” a range of estimates of the so-called neutral level means that monetary policy is no longer on autopilot. Instead, the central bank will be more dependent on the incoming economic data to decide when to raise rates.

But what data will bring the Fed’s rate hiking cycle to at least a temporary pause? I think the data need to be sufficiently weak so as to expect the unemployment rate will move sideways throughout 2019. A December rate hike, which is pretty much in the bag, will put policy rates near the bottom of the range of estimates of the neutral rate, or 2.5 percent to 3.5 percent.

Second, and maybe more important, Powell added this comment regarding policy lags: “We also know that the economic effects of our gradual rate increases are uncertain, and may take a year or more to be fully realized.” Why is this important? As the Fed approached the lower end of the range of neutral, policy was going to become increasingly data-dependent. A big question was how far into the neutral range did the Fed plan to go. Would the Fed be willing to pause at the lower side of those estimates while waiting to see the impact of those past rate hikes? I think Powell just answered that question with a “yes.”

More accurately, though, it is a qualified “yes.” Policy has always been data-dependent. If the data evolve in such a way that rates clearly remain well below neutral, then the Fed will push deeper into the range of estimates before pausing. But if the data stumble, the Fed will stop sooner than later.

Now, let’s think about the calendar. Expect a rate hike in December. Then assume the Fed retains the path of gradual policy adjustment and takes a pass on the January meeting. That leaves the March meeting as the next likely time to hike rates. Finally, assume inflation remains under control.

Between now and March we will see almost four months of data. That’s enough for the Fed to skip a rate hike in March — and perhaps in following meetings — if it is soft enough. So, what would that data need to look like?

At the risk of oversimplification, a combination of a retrenchment in housing and manufacturing combined with slower job growth sufficient to hold the unemployment rate steady would be enough to push the Fed to the sidelines. A similar combination of data is what prompted the Fed to change course the last time they successfully engineered a soft landing, which was in 1995.

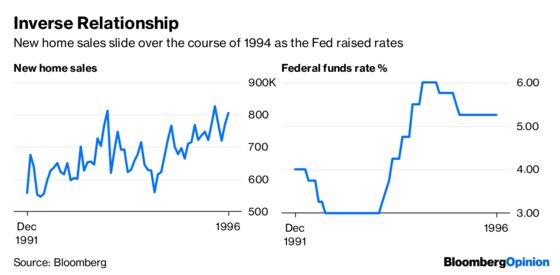

First, housing softened as the Fed hiked rates in 1994:

The same is happening now. New home sales are down 24 percent from the peak in November of last year. One down, two to go.

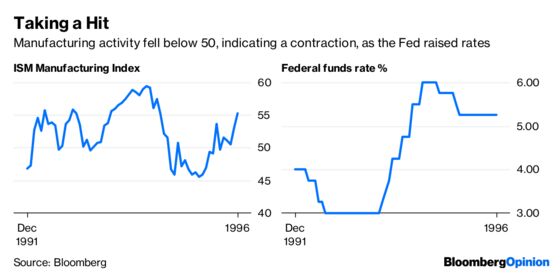

Next, manufacturing weakened, illustrated by a decline in the Institute of Supply Management composite index:

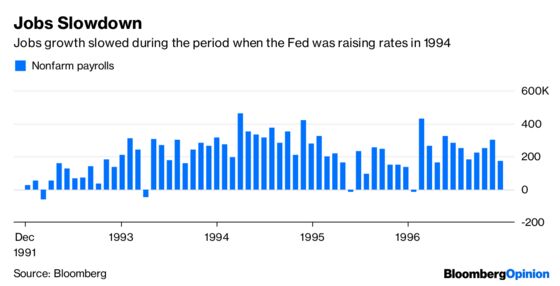

Shortly after, job growth slowed as well:

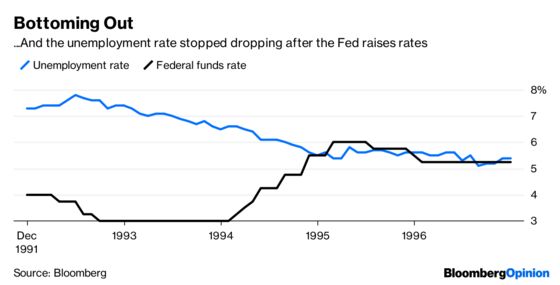

The pace of job growth was sufficient to hold the unemployment rate steady:

It’s not out of the question that a similar pattern of data could emerge between now and March. As noted earlier, housing has already slowed. This combination would be sufficient to push the Fed to the sidelines for an extended period of time. In 1995, the Fed actually did more than sit on the sidelines; they cut rates later in the year. But we aren’t ready for that discussion yet.

To be sure, the above is a sample of the entire range of data that would combine to influence the Fed’s decision. Most important, though, is that the data downshift sufficiently to steady the unemployment rate.

This prediction is arguably not consistent with the Fed’s forecasts. In the Summary of Economic Projections, the median policy maker anticipates the Fed can’t pause as long as unemployment remains below the estimates of the natural rate of unemployment. In other words, stable unemployment rates aren’t enough to justify holding rates steady. In practice, however, the Fed doesn’t hike rates when economic conditions shift such that the unemployment rate is moving sideways. In a low inflation environment, the Fed will instead tend to lower estimates of the natural rate of unemployment.

If the data shift in this direction by March, the Fed will likely hold rates at the lowest end of the neutral rates estimates. If not, the Fed will feel comfortable pushing rates deeper into the range of neutral rate estimates. And if inflation starts picking up to a sustainable rate of 2.5 percent, the Fed will push into the high range of the neutral estimates.

In other words, maybe the Fed delivers no rate hikes in 2019. Or, maybe they deliver four 25 basis-point increases. It’s data-dependent. But if manufacturing follows housing and stumbles in the next couple of months while job growth eases, the actual outcome will likely be at the lower end of that range.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Duy is a professor of practice and senior director of the Oregon Economic Forum at the University of Oregon and the author of Tim Duy's Fed Watch.

©2018 Bloomberg L.P.