(Bloomberg Opinion) -- If you thought Sunday night’s snoozer between the New England Patriots and Los Angeles Rams was painful, just try watching the stock market. After the big rally to start the year, it’s as if U.S. equities are now just moping around, waiting for something good to happen to prove that the gains were built on something a bit more solid than a whiplash-like rebound from oversold levels.

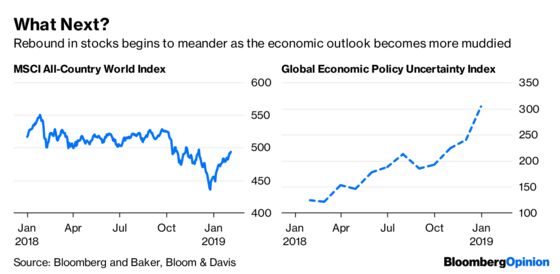

The CBOE Volatility Index, or VIX, mirrors this myopic attitude, falling on Monday to its lowest level since early October. And while Friday’s monthly U.S. jobs and Institute for Supply Management reports helped to damp buyer’s remorse a bit, Monday’s data showing big declines in November factory orders and durable goods orders when more strategists are talking about a coming “earnings recession” should add some angst. But that’s the type of late-cycle, seesaw environment investors should get used to going forward. “We caution against chasing the rally in risk assets, particularly in areas vulnerable to growth downgrades, geopolitical risks or sudden shifts in supply/demand dynamics,” Richard Turnill, BlackRock’s global chief investment strategist, wrote in a research note Monday. Turnill is right to urge caution. The Global Economic Uncertainty Index, a measure of unpredictability in 20 countries with the U.S., China and euro zone being some of the biggest components, has risen to a record amid what seems like higher-than-normal political uncertainty and the very real prospect of another U.S. government shutdown in coming days as well as the U.S.-China trade talks, which are due to wrap up March 1 with or without a deal. Add in the U.K.’s continuing Brexit follies, the fact that Italy’s not-so-insignificant economy has formally entered a recession, and political strife in Venezuela, to name just a few potential headwinds, and one quickly realizes that a lot has to break right for stocks to continue their rally.

“Near-term consensus expectations for economic and earnings growth still appear high, even though we view the risk of a 2019 U.S. recession as low,” Turnill added. “We also see geopolitical risks as a persistent force in markets — with the strategic confrontation between the U.S. and China over technology dominance and threats to European political stability as two underappreciated risks over the medium term.”

THE BOND KING AND THE NEW NORMAL

Bill Gross, a legend on Wall Street who brought bond investing to the masses over a four-decade career, announced his retirement Monday. One thing Gross will be remembered for is helping to popularize the phrase “new normal” in the wake of the financial crisis a decade ago to describe the coming era of subdued economic growth. While the phrase doesn’t get used as much today, it’s still very much in play. That can be seen in the recent turn lower in the global economy after only a brief period in early 2018 when everyone was hyping a global synchronized economic recovery. Data on Thursday showed that Italy — a Group of Seven country — formally entered a recession. All this renewed hand-wringing over the economy is on display in the global bond markets, specifically in the rising amount of global negative-yielding debt, which Bloomberg puts at $8.78 trillion. That’s the most since 2017 and up from about $5.73 trillion as recently as October. In other words, investors wouldn’t be scrambling into safe government debt, bidding up prices and pushing yields below zero, if they thought all was right in the world.

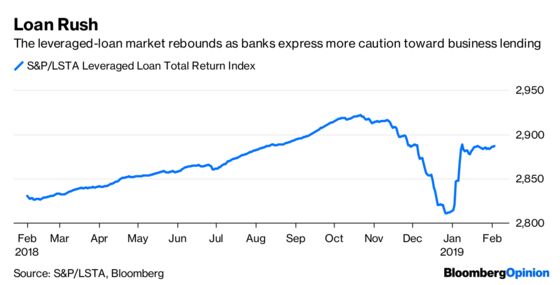

LOAN BANKERS GET CAUTIOUS

The Federal Reserve released its quarterly Senior Loan Officer Opinion Survey on Monday, and the results showed that “demand for loans to businesses reportedly weakened.” This is another data point that should not engender a lot of confidence in outlook for risk assets. Some key excerpts include a note that “demand is expected to weaken for all business loans” and that “banks reported expecting loan performance, as measured by charge-offs and delinquencies, to deteriorate.” This calls into question the recent strong performance of leveraged loans, or those high-risk debt obligations issued and traded among investors like corporate bonds. The S&P/LSTA Leveraged Loan Index surged 2.55 percent in January, rebounding from a similar-sized loss in December to post its biggest monthly gain since March 2016. Perhaps investors see something that the loan officers who are closest to borrowers don’t, but that’s doubtful. The heightened risk-taking and increased role of shadow banks in the leveraged loan market “warrant close monitoring” given the potential for spillover to other markets, a group of global regulators known as the Financial Stability Board said Monday in a report.

THE FLIGHT TO EMERGING MARKETS

The rush into leveraged loans mimics what is happening with emerging markets. Investors added $3.9 billion to stock and bond ETFs across developing nations as well as those that target specific countries in the week ended Friday — the most in more than a year and the 16th consecutive week of inflows, according to Bloomberg News’s Aline Oyamada. In contrast to the money moving into many other so-called risk assets, the flows into emerging markets look justified. After all, emerging markets had a rough 2018, with the MSCI EM Index of equities falling almost 27 percent between late January and late October. A lot of that poor performance was due to fallout from a few troubled countries, such as Turkey, Argentina and South Africa. But on the whole, emerging-market economies held up. Plus, in the aggregate, emerging-market economies are in a better position than ever before to weather a downturn. Foreign-exchange reserves for the 12 largest emerging-market economies excluding China stand at $3.15 trillion, up from about $3.10 trillion at the end of 2017 and less than $2 trillion in 2009, data compiled by Bloomberg show. In his report, BlackRock’s Turnill wrote that the firm favors emerging markets over developed markets outside the U.S.

GOLD IS EXPENSIVE NO MATTER WHAT CURRENCY

Regardless, it’s hard to ignore the angst being signaled by the price of gold, which has surged about 12 percent since mid-August to just above $1,300 an ounce. While the naysayers might say gold’s price is only back to where it was in May, that’s the wrong way to look at the action in one of the world’s most visible haven assets. The better way to understand what’s going is through flows and the fact that the price of the metal is at a record high in 72 currencies other than the dollar, according to Cumberland Advisors. Global holdings of gold through exchange-traded funds surged 70.6 metric tons in January, bringing assets to the highest in almost six years, according to Bloomberg News’s Ranjeetha Pakiam. The worldwide ETF hoard totaled 2,280.8 tons as of Thursday, up for a fourth consecutive month, according to data compiled by Bloomberg. The increase in January was the biggest monthly expansion since February 2017. Bullion demand has also been increasing after the Federal Reserve signaled that interest-rate increases could be off the table for now. Higher rates dim the allure of gold, which pays no interest. “What began as safe haven flows during rising volatility and risk-off flows has become a story of policy uncertainty and central bank accommodation,” Arbor Research & Trading analyst Peter Forbes wrote in a research note Monday.

TEA LEAVES

The U.S. president’s annual State of the Union speech is usually little more than a PR event. And the one scheduled for Tuesday night sounds little different, with the White House billing it as an optimistic plea to “bridge old divisions, heal old wounds, build new coalitions, forge new solutions and unlock the extraordinary promise of America’s future.” That may be so, but there’s also the chance that the speech contains some market-moving news. If Donald Trump uses the event to put in motion a plan to declare a state of emergency over border wall funding, that could upend negotiations to keep the government open, which would not be taken well by markets, according to the strategists at Brown Brothers Harriman. While the government is temporarily funded until Feb. 15, House Speaker Nancy Pelosi has said that the House-Senate conference committee needs to get a deal done by Friday to leave time for votes. Also, trade remarks may influence equity sectors from footwear to auto parts, while pharma stocks may be volatile if the president zeros in on drug-cost reforms, and financials and housing may be overlooked, according to Bloomberg News’s Felice Maranz.

DON’T MISS

The Fed ‘Put’ Applies to Both the Economy and Markets: Tim Duy

The Dumb Money Is Finally Starting to Smarten Up: Jared Dillian

Fed Won’t Tap Brakes Until It’s Ready for a Recession: Conor Sen

Bill Gross Is a Cautionary Tale for Bond Kings: Brian Chappatta

Zero Rates Went From Japan Exotica to Global Norm: Daniel Moss

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.