This Brexit Delay Is a Bond Market Opportunity

With the EU divorce now months away, there’s plenty of time for the yield-hunters to swoop on U.K. corporate bonds.

(Bloomberg Opinion) -- Brexit hasn't gone away – it's just resting – but the six-month extension agreed with the European Union could turn out to be a capital markets opportunity.

The search for yield is the overriding theme for bond investors this year, and U.K. markets are no exception. From that perspective the window for new sterling-denominated corporate debt sales is open. The question is how much interest there is in taking advantage of it.

Market fundamentals are in excellent shape. The pound is stable versus other major currencies, and the Bank of England is unlikely to raise rates until there is certainty on how the economy will be affected by any resolution to Brexit. This adds up to a smoother ride for planning funding costs and managing foreign-exchange risks.

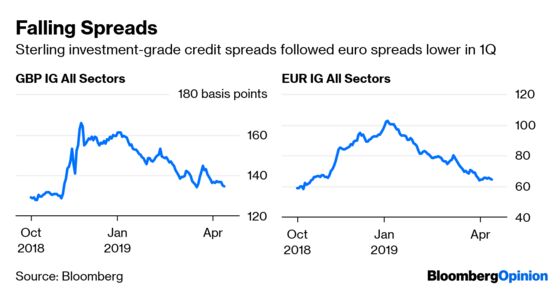

It helps also credit spreads relative to benchmark government debt have tightened in line with those in the U.S. and Europe.

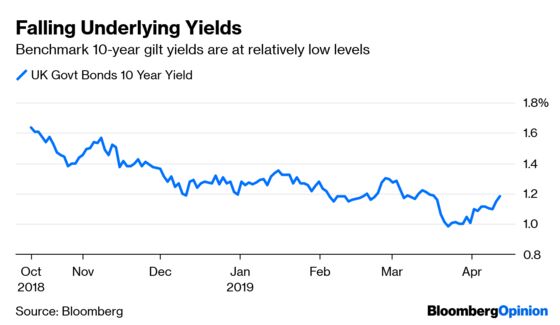

Though underlying government bond yields have risen this month, they are still substantially lower than six months ago. This goes a long way toward lowering the gross issuance cost for corporate issuers.

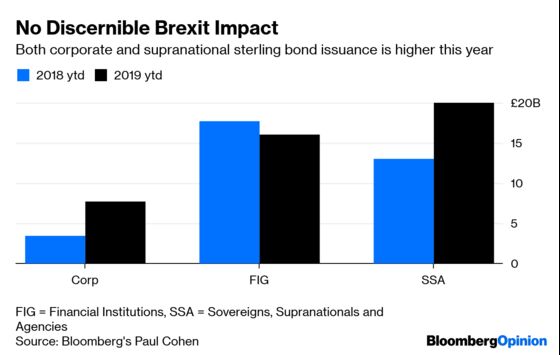

New corporate bond sales in sterling might not be on quite the upswing seen in sales in euros, which rose over 50 percent in the first quarter. Still, they are 30 percent higher than at this stage last year. So far in 2019 there have been about 25 corporate deals denominated in pounds, with Orange SA, Ford Motor Credit Co. , Glencore Plc and Verizon Communications Inc. leading the charge with the biggest deals.

And demand seems to be strong. Yorkshire Water Finance Plc priced a 350 million pound ($458 million) 22-year security on Thursday. It received more than five times the orders than the face amount, even though the spread guidance was tightened by 22.5 basis points by the time the deal completed.

The 40 percent pickup in sales this year in floating rate notes is worth noting, though the dynamics here are somewhat different than in the fixed-rate market. Banks, building societies and supranationals have sold nearly 14 billion pounds of FRNs linked to the Sterling Overnight Index Average this year so far, largely because of the need to replace maturing notes linked to the London Interbank Offered Rate.

The Financial Conduct Authority has heavily encouraged a move away from Libor. Since the European Investment Bank brought the first-ever Sonia-linked deal in June last year it has rapidly become the norm at least for high-grade issuers. Nationwide Building Society is marketing the first residential mortgage-backed bond linked to Sonia, and has even switched its entire balance sheet from Libor to the new rate. The sterling FRN new issuance market is well ahead of both the dollar and euro-denominated markets in switching to the regulator-approved benchmark, and the types of borrowers looking to use Sonia will only increase further.

With the delay to Brexit day alleviating some near-term uncertainty, there’s room for this strong pace of sales to continue in the second quarter. But the pipeline so far looks a bit bare, though Next Group Plc will start a roadshow this week for a 250 million pound 6-8 year security. There’s always a bit of a hiatus around the Easter break, but if there aren’t any deals planned for after that, perhaps it’s time for companies to take a look. For borrowers, it rarely gets much better than this.

It doesn’t necessarily have to last. Bond yields have started to back up – not surprising, given the performance of the S&P 500. Were the U.K. to get involved in a general election or a second referendum, the shift in sentiment away from the current “risk on” mood could hit corporate issuance volumes and spreads. On the other hand, were Brexit to be cleanly resolved, the floodgates for new sales could potentially open.

For now, investor demand is hot as the hunt for yield is in full swing. With sterling currency, credit and interest rate markets becalmed then the brief lull in politics makes for a welcoming environment for corporate issuers.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.