The Fed Needs a Little Push From the Data for a Pause

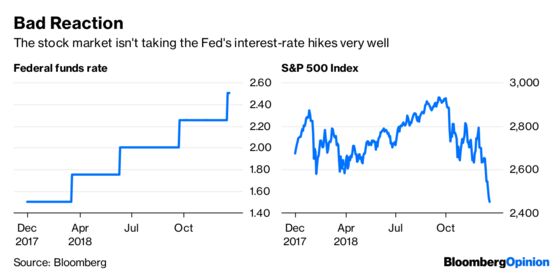

(Bloomberg Opinion) -- One of the reasons for the turmoil in markets this week was that the Federal Reserve was deemed to be not dovish enough in its outlook, seeming to ignore the weakness in equities and other so-called risk assets. To be sure, the Fed will eventually yield and deliver a bigger dose of dovishness, but as we are witnessing now it won’t go down without a fight.

The bar to an extended pause in the pace of interest-rate increases falls every day markets struggle. Indeed, comments Friday by New York Federal Reserve President John Williams make clear that the recent turmoil on Wall Street has not gone unnoticed.

Central bankers behaved this week much as I anticipated a month ago. Despite a sustained and substantial drop in equities, the Fed followed through with their intention to continue tightening monetary policy with Wednesday’s 25 basis-point rate hike. Moreover, they are for the time being sticking to their models, which call for further rate increases over the next couple of years until they reach a level that restrains economic activity.

That said, I anticipate the Fed will in the weeks ahead be forced to address that anxiety shown by investors, much like Williams attempted do on Friday. There is a good chance the Fed will soon take itself off the table for an extended period. It just needs a little push from the data to do it.

So how do we get there? The starting point to that conversation is recognizing that the Fed more likely than not made an error by boosting rates this month. Growth is slowing and inflation remains low while downside uncertainty is on the rise. While the Fed resists reacting to financial markets, the reality is that the downdraft in equities has gone on long enough to warrant additional caution. There is also plenty to worry about on the international side of the equation, from China to Brexit. And finally, policy uncertainty only increases with each passing day of the Trump administration.

There was plenty of reason to shift to a risk management mode at this week’s meeting and take a pass while giving a nod to a January hike. Indeed, the move felt much like the December 2015 rate increase, which also came amidst mounting financial and economic pressures. They both appeared to be model-driven hikes not warranted by the shifting balance of risks.

Hence, I think the Fed has, like in 2015, pushed up against the boundary of appropriate financial conditions. They are now at the edge of neutral in an unstable financial, economic, and political environment. If I am correct and the December hike was an error, they will soon recognize that error via the continued stress on financial markets.

The Fed has already signaled a willingness to give more weight to market developments in future meetings. They added a sentence to the recent Federal Open Market Committee statement that they will be monitoring global and economic and financial developments, a point emphasized by Williams in his CNBC interview. Williams also tried to sooth nervous investors by noting that central bankers are “listening” to markets. Overall, I think they are primed to shift to a more dovish position and all they need is some further softening of the data to push them to the sidelines.

Previously, I discussed some potential data outcomes that would induce the Fed to skip a March hike. Eventually they will realize they need to cushion not just the markets, but also the economy, against the growing uncertainty. With policy near neutral, the continued floundering of financial markets thus only lowers the bar for a pause.

The Fed tends to resist changing course, but when it does change, the shift occurs quickly. Watch for the Fed to stick to its guns and assert more rate hikes are coming, but shift to a more dovish position rapidly when the data softens a notch. That will be good. It’s the key to extending this expansion. This holds true as long as inflation remains under control. If the Fed starts fearing inflation as a more real than imagined threat, they will delay turning dovish. That’s when the game changes in a way that would send markets on an even more volatile path.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Duy is a professor of practice and senior director of the Oregon Economic Forum at the University of Oregon and the author of Tim Duy's Fed Watch.

©2018 Bloomberg L.P.