The ECB Has Policy Makers, Not Superheroes

(Bloomberg Opinion) -- Spare a thought for the European Central Bank.

The minutes of the last Governing Council, published on Thursday, show the central bank is in a bind over the state of the euro zone recovery and the next steps to take.

Still, it is hard to see why they shouldn’t be. The economic picture is objectively confusing. The problem is that we have come to rely so much on guidance from central bankers, that we are unable to accept when they are not in the position to anticipate very much.

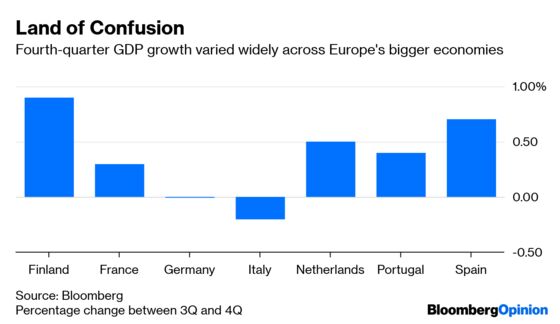

Europe’s central bankers know they are presiding over a slowing economy. Growth cooled to 0.2 percent over the last two quarters of last year, down from 0.4 percent in the first two. The deceleration is starting to affect inflation expectations, which are crucial to ensuring that the ECB can meet its target. Financial conditions, while still favorable, have tightened compared to last year.

The question is just how serious this decline will be and what to do about it. The ECB is considering launching a new round of cheap loans to the banks, which would help to unclog the monetary transmission mechanism particularly in the parts of the currency union where the economy is weakest. But the minutes show that the ECB hasn’t made up its mind yet:

“While any decisions in this respect should not be taken too hastily, the technical analyses required to prepare policy options for future liquidity operations needed to proceed swiftly.”

If you wanted a one-line example of what monetary disorientation can mean, this is probably it.

Remarks earlier this week by some officials signaling a change in sentiment could easily be criticized for being too slow or unhelpful. And yet, it is hard to see how anyone else could do any better than this at this stage.

While growth is coming down everywhere in the euro zone, some countries – Germany and, above all, Italy – are in worse shape than others. Global trade tensions are proving a serious drag on exports – but it is not clear whether they will be resolved, since this largely depends on negotiations between the mercurial U.S. President Donald Trump and his secretive Chinese counterpart, Xi Jinping. On Thursday, the latest batch of data on economic activity was a mixed bag: the purchasing managers index for manufacturing dropped below 50 in February, signalling a contraction for the first time in nearly six years, but the gauge for services showed accelerating growth, with a marked jump for Germany.

Central bankers are grappling with two forces. The first is their decision since the financial crisis to be much more open about the direction of policy. Forward guidance can offer extra accommodation when rates are already stuck near zero by encouraging companies and consumers to borrow in the knowledge that monetary policy will not be tightened for a while. But this can generate an expectation that officials will always tell you what they will do next. When such decision is uncertain, or hinging on confusing data, the credibility of a central bank is bound to suffer more than it would have in the past.

The second is the outsized role monetary authorities have played in the last decade, particularly in the euro zone. Politicians, not central bankers, have responsibility for solving the problems affecting the currency union at the moment. Italy’s recession has a strong self-inflicted element to it: smarter tax and spending decisions in Rome and fewer policies that undermine the country’s competitiveness would go a long way to reducing the risk of a credit crunch. Similarly, were the German government to opt for greater investment spending, this would help to rebalance the economy away from slowing foreign demand.

The ECB has some explaining to do over its recent decisions. The choice to announce the termination of its net asset purchases as soon as last June is beginning to look questionable. But, by the same token, it is wise to give policy makers a bit more time before they announce their next big decision. Better to wait a little longer than to have to change tack soon afterwards.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns and editorials on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2019 Bloomberg L.P.