The Bond Market Just Sent a Disturbing Message

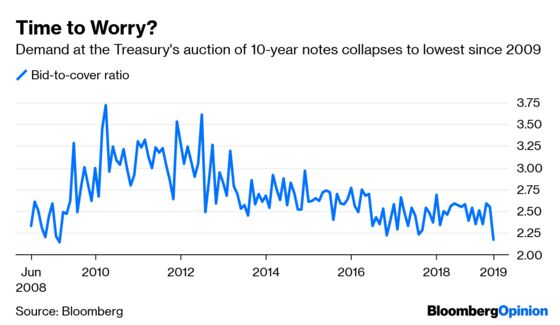

(Bloomberg Opinion) -- Global markets got a glimpse of the unthinkable Wednesday when the U.S. held a key bond auction. The $27 billion sale of 10-year notes – the world’s benchmark securities – didn’t go well at all. It wasn’t a failure; that would have triggered no less than an Armageddon-type event on par with the financial crisis. But the poor demand sure sparked a lot of questions, including whether this was a sign that investors finally had enough of the government’s profligate spending and borrowing.

Investors submitted bids for 2.17 times the amount offered by the Treasury Department, the lowest so-called bid-to-cover ratio since March 2009, hammering home the notion that demand for U.S. bonds isn’t limitless with the government on track to borrow $1 trillion to finance a budget deficit by the same amount. Total U.S. debt is now above $22 trillion, up from less than $10 trillion before the financial crisis. To be sure, it’s too early to say the bond vigilantes have returned, but it’s notable that bid-to-cover ratios and international participation at the auctions has been declining for a few years now. Foreign holders own about 40 percent of the marketable U.S. debt outstanding, down from more than 50 percent pre-crisis. “I wish the buyers could talk to see what it was about this yield that was so unattractive,” Bleakley Financial Group chief investment officer Peter Boockvar wrote in a note to clients. Maybe it was because yields near the lowest since late 2017 “just wasn’t attractive. Maybe buyers aren’t as sanguine as many others that inflation is so benign. Maybe it’s in response to exploding U.S. debts and deficits. Maybe it’s because the cost of hedging on the part of overseas investors has made buying longer-term U.S. Treasuries on a hedged basis just not worth it.

Nothing scares big investors more than the notion that the U.S. could hold a bond auction and nobody showed up. After all, Treasuries are the world’s safest investment, backed by the full faith and credit of the U.S. But on Wednesday, investors sent a message to the Treasury Department that past isn’t prologue when it comes to demand for U.S. debt.

STICKING CLOSE TO HOME

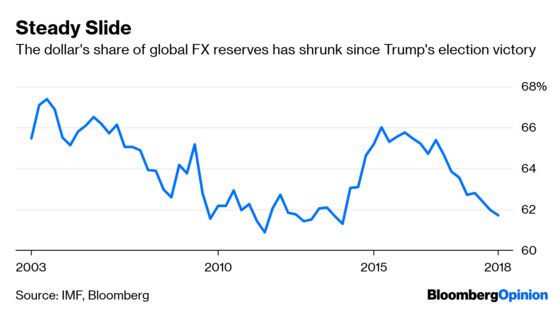

Before ringing the alarm bell too loudly, there’s plenty of evidence that the U.S. is still a desirable place to invest due to its stable political system (that’s no joke) and adherence to the rule of law. At 61.7%, the dollar’s share of global currency reserves is by far the biggest, tripling the euro’s 20.7% share, according to the International Monetary Fund. But that’s not to say things aren’t changing. The dollar’s share is down from 72.7% in the early 2000s, and there’s evidence that investors are more inclined to invest in their home countries. Global foreign direct investment has fallen to the lowest level since 2009, dropping 19 percent last year, according to management consulting firm A.T. Kearney’s newly released Foreign Direct Investment Confidence Index, which is based on its annual survey of 500 senior executives. "Investors perceive that risks are rising in developed markets," according to the report. “Although many developed markets have more transparent governance – a metric highly valued by investors – rising risks, geopolitical and economic alike, do cast some immediate concerns in the short-term horizon.” The U.S. dominated the index for the seventh year in a row, followed by Germany and Canada, according to Bloomberg News’s Marie Patino. China is the only developing country that makes it to the top 10, and 22 out of the top 25 most trusted countries are developed countries.

IS A TRADE DEAL PRICED IN?

U.S. stocks managed a small gain on Wednesday after starting the week with their biggest two-day selloff of the year as the S&P 500 Index slid more than 2 percent. With the U.S. and China scheduled for trade talks Thursday and Friday, traders spent much of the day trying to work out whether a deal is priced in to stocks. RBC Capital Markets Chief U.S. Economist Tom Porcelli thinks he has the answer. “This is a good time to remind folks that the tariff tantrums have significantly suppressed equity market performance,” Porcelli wrote in a note to clients. He claims the S&P 500’s 15% year-to-date gain is deceiving and is really more a function of a rebound from the steep plunge at the end of last year. “The reality is that despite significant corporate tax relief that kicked in last year – and boosted the bottom line meaningfully – in the wake of the trade skirmish with China that began in late January of last year, the S&P 500 has returned through the May 7 close a grand total of 1.6%,” Porcelli wrote. “If we strip out inflation, broad equities are down about 1% in that span. By that token, a ‘done deal’ on trade doesn’t seem to be priced in.” So, given the painful selloff in stocks Monday and Tuesday, here’s something for the bulls: The spread between the S&P 500’s earnings yield – a proxy for how much equities “pay” shareholders – and the 10-year Treasury yield is currently 2.9 percentage points, according to Bloomberg News’s Sarah Ponczek. (The wider it is, the cheaper stocks are.) Strip out the last five months, when stocks fluctuated wildly, and the relative payout of stocks over bonds is the highest since 2016.

THE QUIET MARKET

They say it’s always the quite ones you have to worry about. And in the global markets, currencies are almost mute. While measures of volatility in stocks – and even interest rates - has jumped, those for currencies are oddly subdued. The JPMorgan Global FX Volatility Index was at 7.01 on Wednesday, down from 9.36 in early January. Put another way, the gauge has rarely been lower since before the financial crisis. Reasons for why this is include structural changes that have made the currency market more about flash volatility events due to specific gaps in liquidity, according to Bloomberg News’s Liz Capo McCormick. Positioning dynamics and recent idiosyncratic forces (aside from Trump’s rhetoric) are also capping fluctuations, she adds. “What the market tends to experience more now is not a rise when it happens in all assets but instead flash-crash episodes,” Steve Barrow, head of currency strategy at Standard Bank, told Bloomberg News. “Currencies that are moving, such as those in emerging markets, are due to specific domestic factors.” The thing to know here is that more than $5 trillion of currencies trade each day, making it the deepest, most liquid market in the world. So the fact that the market is in a state of relative calm should be a reassuring signal, and that the U.S. and China will ultimately come to a trade deal without causing too much more damage to the global economy.

TIGHT SUPPLIES

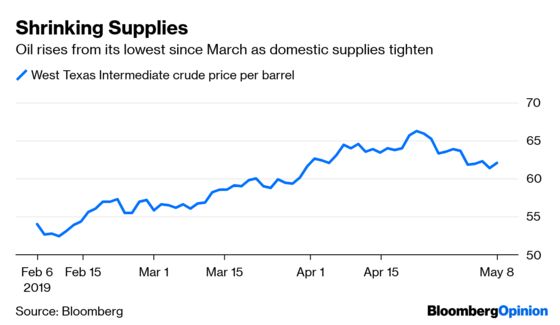

President Donald Trump is known for lobbing tweets toward OPEC, imploring the cartel to open the spigots and boost supply in order to lower the price of oil. Perhaps a better target might be U.S. producers, though that might not make good political sense. West Texas Intermediate crude prices rose the most in more than two weeks on Wednesday, gaining as much as 1.58 percent to $62.37 a barrel as a surprise drop in U.S. supplies added to evidence of a tightening global market. The Energy Information Administration said domestic crude inventories shrank by almost 4 million barrels last week, defying expectations for an increase, according to Bloomberg News’s Alex Nussbaum. The decline in oil stockpiles was the first in the U.S. in three weeks, and came alongside a drop in gasoline and distillate supplies that could generate more demand for crude going forward. But with imports from Saudi Arabia slipping to an all-time low as OPEC and its allies continued to restrict output, the pressure is on oil prices to move higher.

TEA LEAVES

One of the big surprises this year is how key global economic data has done better than expected. Both the U.S. and euro zone gross domestic product reports for the first quarter exceeded expectations, and Bloomberg Economics says there’s a good chance that the U.K. does as well when its numbers are reported Thursday despite an escalating Brexit crisis that’s divided Parliament and the government. Britain’s GDP rose 0.2 percent in February after a 0.5 percent jump in January. That means the economy will expand 0.5 percent in the first quarter if GDP was unchanged in March, Bloomberg Economics figures. That’s also the median estimate of economists surveyed by Bloomberg News. The data may provide a small boost to U.K. Prime Minister Theresa May as she awaits a final decision on the length of the delay to Brexit. European Council President Donald Tusk has rejected her request for a brief postponement and a longer period risks a backlash that could further destabilize the U.K., both politically and economically, Bloomberg Economics says.

DON’T MISS

Trade Talks and the Two Key Market Implications: Komal Sri-Kumar

A U.S.-China Trade Deal Doesn't Matter Anymore: Michael Schuman

‘Smart Beta’ Might Not Be Very Smart After All: Noah Smith

Value Investing Is Back in China, Thanks to Trump: Shuli Ren

A Tale of Two Central Banks With the Same Problem: Daniel Moss

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.