The Tables Are Turning on Emerging Markets

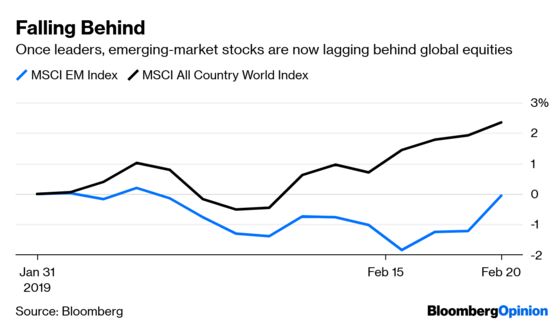

(Bloomberg Opinion) -- Emerging markets made it through the turmoil in late 2018 relatively unscathed. The MSCI Emerging Markets Index of equities actually rose 1.03 percent over the final two months of the year, compared with a decline of 5.97 percent in the MSCI All-Country World Index. That outperformance continued in January, but the tables have turned in February with the 0.14 percent gain in the emerging-market benchmark trailing the 2.32 percent surge in the broader market despite emerging markets posting their best day in six weeks on Wednesday by surging as much as 1.50 percent.

Investors jumped on the emerging-market bandwagon last month, leading the remarkable turnaround in risk sentiment globally from the dark days of December. But that’s the problem. A number of influential investors and strategists now say it’s time to reconsider the prospects for such assets, raising concern that a reversal in sentiment could drag global markets lower just as they led them higher. A combination of potentially hawkish Federal Reserve surprises and already stretched performance has persuaded HSBC Holdings Plc strategists including Max Kettner to turn cautious on emerging-market assets, while Bank of America Merrill Lynch strategist Ralf Preusser thinks developing-nation bonds are vulnerable to positive U.S. data releases, Bloomberg News’s Cormac Mullan reports. “Might now be the time to reduce EM exposure in portfolios tactically, that is over three months? We think it is indeed time for a breather,” the HSBC strategists wrote in a research note. In another sign that optimism is waning, investors added money to emerging-market exchange-traded funds at the slowest pace this year last week. Inflows into U.S.-listed funds that invest across developing nations as well as those that target specific countries totaled $313.1 million in the five days through Feb. 15, according to Bloomberg News’s Aline Oyamada. That’s a fraction of the $3.97 billion inflow in the previous week.

What’s important to know is that emerging markets are increasingly having a bigger impact on the direction of asset prices given how fast their economies have grown. Based on a study by PricewaterhouseCoopers Global, the seven largest emerging-market economies could grow around twice as fast as the Group of 7 on average in the years ahead. As a result, six of the seven largest economies in the world are projected to be emerging economies in 2050 led by China (1st), India (2nd) and Indonesia (4th).

IGNORE BONDS AT YOUR PERIL

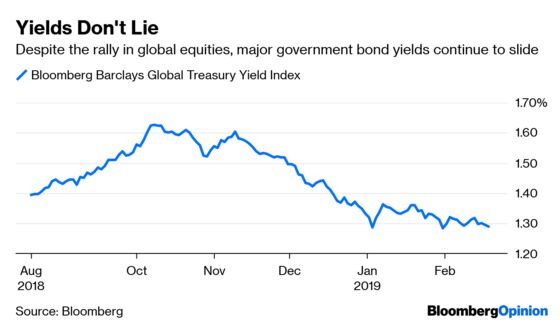

Having digested the minutes from the Federal Reserve’s last meeting in January, bond traders can now turn their attention to the two main geopolitical risks that remain outstanding: trade talks between the U.S. and China and the rising possibility of a so-called hard Brexit, in which the U.K. crashes out of the European Union without a negotiated deal. As the top-ranked interest rate strategists at BMO Capital Markets point out, neither of the impending deadlines of March 1 or March 29 appear set in stone, and either one could be extended. “Whether this dynamic increases the probability of a comprehensive agreement, or merely kicks the can down the road, is difficult to discern ahead of time,” but the fact that 30-year government bond yields in Germany, Japan and the U.S. “are all back at late-2016 levels suggests that markets aren’t exactly anticipating a global synchronized acceleration anytime soon; if anything, the opposite.” In other words, don’t dismiss the signals being sent by the global government bond market. When it comes to U.S.-China trade talks, an extension of the deadline may not be seen as positive news, as it just means that investors will have to continue to deal with more uncertainty when the Global Economic Uncertainty Index, a measure of unpredictability in 20 countries with the U.S., China and euro zone being some of the biggest components, has risen to a record. What that means is that any misstep on the policy front could have an outsized negative impact on riskier assets, as the bond market seems to expect.

STOCK BULLS SEARCH FOR MEANING U.S. equities have modestly outperformed the rest of the world this year, with the MSCI US Index gaining 11.3 percent compared with a 9.34 percent increase in an MSCI index of global stocks that excludes the U.S. Such performance raises the question of whether U.S. stocks have risen too far, too fast, especially with the possibility of an earnings recession looming. After all, an 11 percent gain would be good for any full year, and February isn’t even over yet. But the bulls are searching hard for trading patterns that would suggest the good times have further to go. Keith Lerner, the chief market strategist at SunTrust Private Wealth Management, has zeroed in on stocks in the S&P 500 Index that exceed their 50-day moving average. Lerner has found that more than 90 percent were above the threshold Friday for the first time since March 2016 based on data compiled by Bloomberg, according to Bloomberg News’s David Wilson. The earlier instance was among 14 that Lerner cited since 1990, and the S&P 500 rose all but once in the next three and 12 months after those moves. That sounds tempting, but DataTrek Research notes that analysts on average have been cutting their price targets for individual stocks despite this year’s rally in the S&P 500. Currently, that aggregate price target is 3,059, representing an 11 percent expected return over the next 12 months, down from a forecast if 3,094 in early January. That’s one trend going in the wrong direction for the bulls.

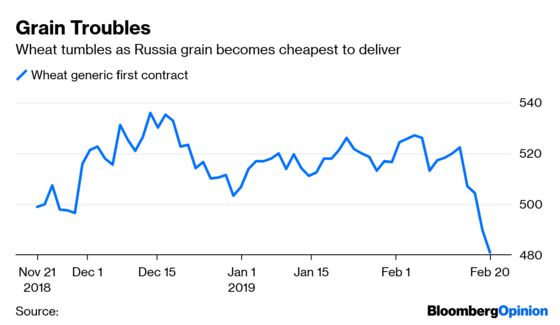

COMMODITIES RALLY. JUST DON’T TELL WHEAT FARMERS. The commodities market is having a moment, rising every day this week. In that period the Bloomberg Commodity Index rose as much as 2.31 percent in its biggest three-day gain since the start of October. Perhaps the move is tied to comments made by President Dnald Trump that trade talks with China, the world’s largest consumer of raw materials, are going well. If true, then maybe China’s economy will stabilize. Heavy equipment machinery company Caterpillar Inc. gave some credence to such notions on Wednesday when Amy Campbell, head of investor relations, said in a presentation at a conference that the pace of equipment replacement in the Asian nation is at normal levels. Just don’t tell wheat farmers. The price of the grain fell to its lowest since July on Wednesday, hurt by signs that U.S. exports are struggling to compete with global oversupply. Also, Egypt had a wheat tender that could bring about the “worst scenario” for American and European supplies, according to Bloomberg News’s Isis Almeida and Salma El Wardany. With prices slumping, Russian grain has made a comeback to the list of cheapest offers, according to traders familiar with the process. On top of that, French supplies, which were expected to be competitive, turned out more expensive than Romanian and Ukrainian wheat, after freight costs are included, said the traders, who asked not to be identified because they’re not authorized to speak to the media. There were no U.S. offers.

SWEDEN HAS FALLEN AND IT CAN’T GET UP

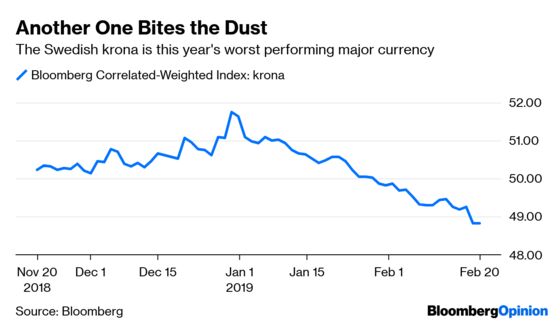

The Swedish krona did nothing on Wednesday, basically ending unchanged against a basket on nine other developed-market peers. But that’s a significant victory for a currency that has been beaten down badly this year as poor economic data thwart the Riksbank’s plans to finally start raising interest rates out of negative territory for the first time in more than four years. The krona has depreciated some 5.63 percent this year to an all-time low against the basket as measured by the Bloomberg Correlated-Weighted Indexes. The latest blow came on Tuesday in the form of a weaker-than-forecast inflation report. Consumer prices with a constant interest rate rose an annual 2.0 percent in January, below the 2.3 percent median estimate by economists surveyed by Bloomberg and the 2.4 percent predicted by the central bank. Sweden’s economic growth is forecast to slow to 1.3 percent this year from 2.2 percent in 2018, according to a survey by Bloomberg News. The troubling thing is that Sweden is just one example. More and more large economies and central banks are grappling with subpar data, which is why more and more market participants are expecting a global synchronized slowdown. In fact, the data in major economies is coming in below estimates at a degree that is among the worst seen over the past five years, according to the Citigroup Economic Surprise Indexes.

TEA LEAVES

In many ways, the euro zone is ground zero when it comes to concerns about a budding synchronized economic slowdown. The median estimate of economists surveyed by Bloomberg is that the currency bloc’s economy expanded at an anemic 1.5 percent annualized rate in the fourth quarter. The forecast for all of 2019 isn’t any better at 1.4 percent. That’s why market participants will be keeping a close eye on the PMI manufacturing reports due out Thursday for a sense of just how rapidly economic conditions are deteriorating. The good news is that it appears things are stabilizing. IHS Markit Economics’ composite purchasing managers’ index is seen little changed at about its lowest level since late 2014 with a reading of 51.1 for February. The European Central Bank signaled at its last meeting that it was in data-watching mode in the run-up to its next meeting on March 7 as it tries to assess the nature of the euro area downturn and how long it is set to last, the strategists at RBC Capital Markets wrote in a research note. “The February flash ‘PMIs,’ therefore, represent one of the more significant data points ahead of that next gathering,” they added.

DON’T MISS

The U.S., Not China, Is the Real Currency Manipulator: Shuli Ren

China’s Recession-Proof Economy to Get a Stress Test: Noah Smith

Trump Tariff Threat Leaves EU Looking for Plan B: Lionel Laurent

How Frightening Are Subprime Auto Loans?: Brian Chappatta

Glencore Brings Thermal Coal’s End a Step Closer: David Fickling

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.