Stock Traders Seem to Have Overshot to Downside

(Bloomberg Opinion) -- Is the potential for an economic slowdown priced in to financial assets? There’s been no bigger question in global markets after riskier assets such as stocks melted down in December. Judging by the recent performance MSCI All-Country World Index, the answer seems to be yes.

In the U.S., for example, the 19.9 percent plunge in the MSCI USA Index between late September and Christmas Eve left shares trading at their lowest levels since 2013 relative to estimated earnings. Even with the rebound since then, investors are pricing in about a 60 percent chance of a typical recession this year, where earnings drop by 9 percent, according to strategists at JPMorgan Chase & Co. led by Nikolaos Panigirtzoglou. That seems extreme, considering economists surveyed by Bloomberg News put the odds at about 20 percent. Market participants will get a better sense of how Corporate America sees the outlook in coming weeks as companies report fourth-quarter results. The cynics might argue that given the deep slide in stocks last quarter, executives have cover to lowball the outlook so they can look good by beating these lowered expectations later in the year. Although the consensus is for U.S. companies to report greater than 12 percent growth in fourth-quarter earnings, increases in the first quarter are forecast to be less than 4 percent, and less than 5 percent for the second quarter as the benefit of lower tax rates wear off, according to Bianco Research. For the year, earnings are seen rising a bit less than 8 percent.

While that wouldn’t be as good as the greater than 20 percent gains in earnings seen in recent quarters, it would be a nice surprise, given JPMorgan’s analysis that stocks have traded as if a 9 percent decline is likely. On Monday, the MSCI USA Index rallied 0.74 percent, adding to Friday’s 3.45 percent surge. The global MSCI All-Country World Index posted a two-day gain of 3.52 percent, the most since mid-2016. “We have a respectable probability that Friday’s rally and the last week-and-a-half’s rally has more legs behind it,” David Sowerby, managing director and portfolio manager at Ancora Advisors in Cleveland, told Bloomberg News.

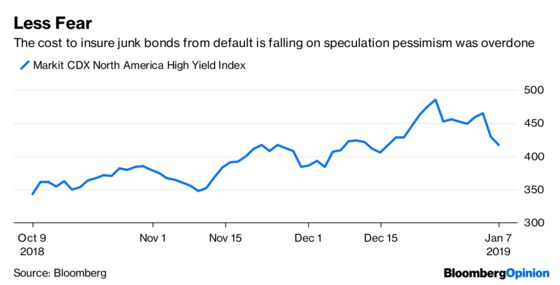

JUNK BOND SELL-OFF TAKES A BREATHER

Speculative-grade corporate bonds and loans are also enjoying a rebound, which would be unusual if fixed-income investors — generally considered more savvy when it comes to the economy than equity investors — were really convinced that a recession was on the horizon. An index measuring the cost to insure speculative-grade corporate bonds with credit-default swaps has posted its biggest two-day drop since August 2015. Morgan Stanley’s credit strategists wrote in a research note Monday that they are turning a bit less bearish, reducing their “underweight” recommendation on U.S. credit markets and recommending investors add “some credit risk tactically,” while noting that “this is not a change in our long-term view.” “We continue to believe that credit is in a bear market, and that a long, slow turn in the credit cycle has begun,” they wrote. As of last week, investors were demanding an extra 5.37 percentage points in yield over benchmark U.S. Treasuries to own junk bonds, up from less than 3.20 percent points in early October. By way of comparison, spreads ballooned to almost 9 percentage points in early 2016. “Valuations just got too cheap, unless you expect a recession and a spike in default activity,” Michael Marzouk, a portfolio manager at Pacific Asset Management, told Bloomberg News in regards to a corresponding rally in leveraged loans.

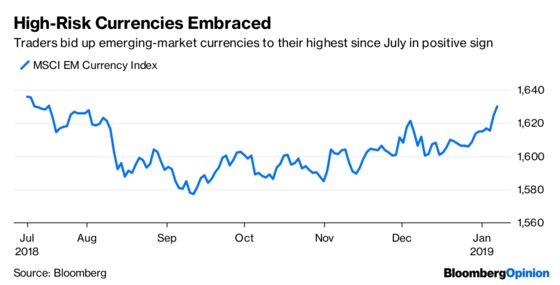

EMERGING MARKETS BACK IN GOLDILOCKS MODE

It would be easy to dismiss the rally in U.S. stocks and junk bonds as just a short-term bounce inside an inevitable bear market brought on by a synchronized global economic slowdown until emerging markets are brought into the conversation. While the outlook for developed economies is rather gloomy, the currencies of emerging markets are enjoying a bit of a renaissance, suggesting any global slowdown may not be too severe. On Monday, the MSCI Emerging Markets Currency Index rose to its highest level since July, having risen in eight of the past 10 weeks. The Brazilian real, South African rand and Russian ruble are leading the gains so far this year, with all three currencies appreciating at least 3 percent against the dollar. Emerging markets have been buoyed by signals from Federal Reserve officials that they might slow the pace of interest-rate increases if U.S. economic growth continues to decelerate. Rate hikes from the Fed was largely blamed for the poor performance of emerging-market assets through the first three quarters of 2018. “The Goldilocks scenario turned to tatters during 2018,” Piotr Matys, an emerging-market foreign-exchange strategist at Rabobank, wrote in a research note Monday as reported by Bloomberg News’s Justin Carrigan. “However, it seems that this expression has been dusted off from the lexicon of financial markets following comments from Fed Chairman Jerome Powell on Friday, who gave severely battered investors what they wanted to hear.”

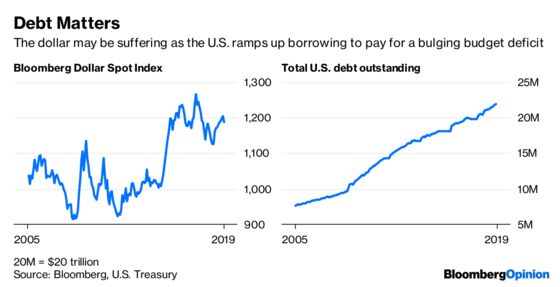

DOLLARS AND DEBTS

The government may be shut, but the Treasury Department is open, and it said Monday that the amount of U.S. debt outstanding as of year-end was $21.974 trillion, an all-time high. What that means is that the government added $1.48 trillion of debt in 2018, almost triple the $515.9 billion added in 2017, as the U.S. increased borrowing to help make up for the revenue lost by slashing corporate tax rates. A number of strategists have cited the rising debt load and widening budget deficit as a reason for the recent weakness in the greenback. The Bloomberg Dollar Spot Index, which measures the currency against its major peers, fell on Monday to its lowest since October. The International Monetary Fund released its quarterly report on global foreign-exchange reserves on Dec. 31, which showed that the dollar accounted for 61.9 percent of worldwide reserves at the end of the second quarter, the lowest level since the end of 2013. “As we’ve been warning for a while now, a U.S. recession — when it happens — will be the game-changer for the dollar and would likely push it into a multi-year downtrend as the Fed cuts rates and the budget deficit blows out,” the currency strategists at Brown Brothers Harriman wrote in a research note Monday. “The only thing limiting the dollar’s losses recently is that things in the rest of the world aren’t looking too good, either.”

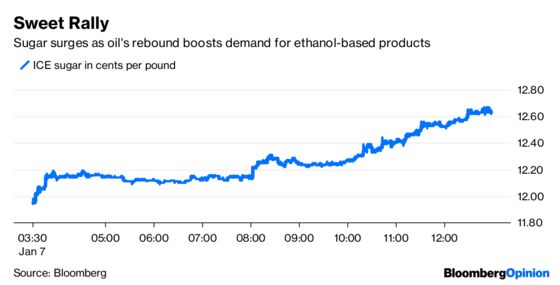

SUGAR’S ON A SUGAR HIGH

All eyes in the commodities market Monday were on sugar, which posted its biggest rally since April 2016 by rising as much as 6.20 percent. It was rare bright spot for a commodity that has fallen 17 percent over the past 12 months. Oddly enough, the rally appears tied to the rebound in oil prices amid news that OPEC is following through on its pledge to cut output. The thinking is that rising oil prices will help boost demand for cane-based ethanol from Brazil, which happens to be the world’s biggest sugar producer. More specifically, Brazilian sugar mills may switch to the biofuel to take advantage of higher prices, limiting supplies of sweetener from the world’s largest exporter, according to Bloomberg News’s Gerson Freitas Jr. and Lynn Thomasson. Motorists in Brazil have become used to filling the tank with ethanol after a change in government policies on gasoline pricing made the cane-based fuel more competitive. Hedge funds and other large speculators don’t think the gains in sugar will last. They cut their bullish white sugar bets by 3,677 net-long positions to 5,787 contracts in the period ended Jan. 1, weekly ICE Futures Europe data on futures and options show.

TEA LEAVES

There’s no end in sight to the U.S. government shutdown, which means the normally steady release of economic data has slowed to a trickle. As such, there’s the chance that those releases that don’t come from the government and don’t usually get top billing will suddenly get a lot more scrutiny. The National Federation of Small Business’s Optimism Index is one such report. Due to be released on Tuesday, the median estimate among economists surveyed by Bloomberg is for a fourth consecutive decline, to 103 for December from 104.8 in November. That’s still a very high level, given that the index was below 95 in the months before Donald Trump was elected U.S. president in November 2016. What market participants want to keep an eye on is the percentage of respondents who expect the economy to improve. In November’s survey, that percentage collapsed to 22 percent, the lowest since November 2016 and down from 33 percent in October. And as we now know, the economy slowed markedly in December. As Bloomberg Economics notes, small businesses benefited from tax reform in 2018, but those benefits are going away. Also, a split Congress implies there is likely to be less benefit from relaxed rules and regulations.

DON’T MISS

Has the Stock Market Established a Bottom?: Mohamed A. El-Erian

The Positives Top the Negatives for Stocks: Charles Lieberman

Baby Boomers Will Be a Drag on Stock Market Rebound: David Ader

Economy Is Finally Coming Through for Workers: Barry Ritholtz

Saudis Slash Oil Output. Get Ready for Trump Tweets: Julian Lee

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.