Stock Traders Learn to Stop Worrying and Love Bonds

Any number of sentiment and positioning indicators have suggested that many equity investors remain wary of chasing the rally.

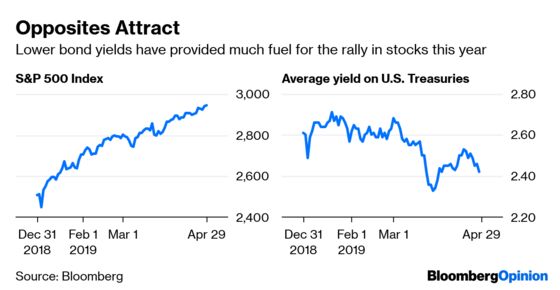

(Bloomberg Opinion) -- Despite this year’s big gains in stocks, with the S&P 500 Index rising more than 17 percent to set an all-time high on Monday, any number of sentiment and positioning indicators have suggested that many equity investors remain wary of chasing the rally. The main reason for the trepidation is the bond market, which has also rallied, driving Treasury yields down to levels that may portend a recession is on the horizon. But instead of debating which market has it right, a growing number of strategists are pointing out how both markets are actually in harmony.

“Let’s put to bed this debate about diverging equities and Treasury yields,” Arbor Research data scientist Ben Breitholtz wrote in a research note Monday. “Risk and safe assets are not reflecting differing opinions about economic growth.” Breitholtz noted that higher equity prices and falling yields are exactly what investors should expect during pauses in Federal Reserve monetary policy, like now. Almost every pause by the central bank has produced the best risk-adjusted returns for traditional portfolios that are 60 percent in stocks and 40 percent in bonds. Plus, Breitholtz notes that economic data in the U.S. and euro zone have been on the mend since mid-February 2019, supporting the S&P 500 and high-yield corporate debt. As for bonds, yields on long-term securities are dropping as inflation slows. Last week, for example, the government said the core personal consumption expenditure index rose just 1.3 percent in the first quarter, matching its smallest increase since 2015. That’s far below the Fed’s 2 percent target. In other words, the economy is expanding — which is good for stocks — and inflation is well under control, which is good for bonds. “The story for April has been pretty straightforward and was reinforced again last week: global growth is stabilizing (for the most part), yet inflation remains weak (for the most part), which means central banks can continue on the very dovish path that began earlier this year,” James McCormick, the global head of desk strategy at NatWest Markets, wrote in a weekend research note.

Over the last 20 years, the stronger the positive correlation between movements in stock prices and changes in bond yields, the better for the stock market, according to Leuthold Group Chief Investment Strategist Jim Paulsen. And the correlation has risen this year. Nevertheless, McCormick sums up why so many investors are hesitant to get all bulled-up on risk assets. “This current Goldilocks environment for financial markets does not feel like an especially stable one,” he wrote. “I can’t help but wonder whether this dovish shift may end badly,” especially with unemployment in major economies so low and wage growth — a leading indicator of faster inflation - starting to pick up.

SIGNS OF LIFE IN EARNINGS

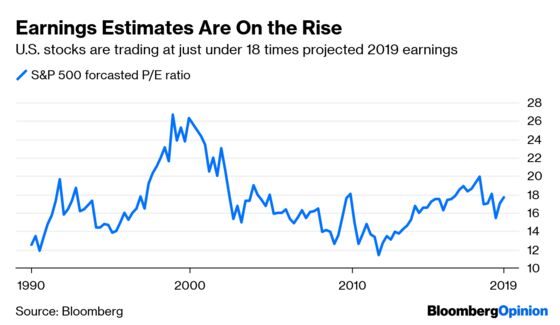

Stocks are also getting support from earnings, which haven’t been as bad as feared. With about half the members of the S&P 500 having reported first-quarter results, earnings are on pace to drop 1.67 percent from a year earlier, much better than the 4.14 percent decline forecast, according to Bloomberg Intelligence. On top of that, expectations for the second quarter are holding steady. “If the S&P 500 is in the midst of an ‘earnings recession,’ it may be the lightest on record,” the BI analysts write in a research note Monday. For the full year, earnings are seen rising by 2 percent to 5 percent, but that’s based on a big jump happening in the fourth quarter. Put another way, analysts’ estimates for members of the S&P 500 suggest the index will show earnings per share of $168.40 for the year, up from $167.97 on April 12 as earnings season was just starting, according to DataTrek Research. So if current price-to-earnings ratios don’t change, the S&P 500 should end the year at 3,162, which is about 7.2 percent higher than Friday’s close. “There’s a lot of things from a macro standpoint that appear to be pretty supportive of the stock market,” Mark Stoeckle, who helps manage about $2.5 billion as chief executive officer of Adams Funds, told Bloomberg News. “The Fed pivoted and trade, at least on the surface, appears to be progressing in the right direction. In addition to that, you see a lot of companies that are reporting some pretty good numbers.”

NO NEED FOR INFLATION PROTECTION

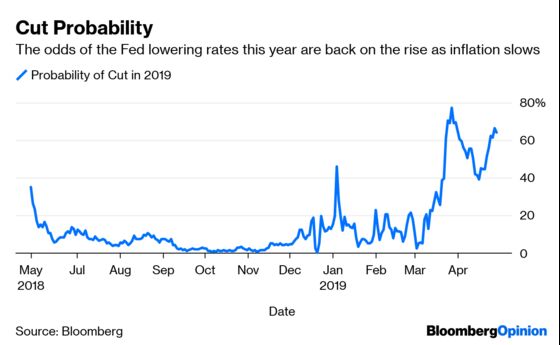

Although Treasuries fell on Monday, the odds of a Fed rate cut this year have risen over the past two weeks to about 65 percent from 40 percent as inflation has slowed, according to data compiled by Bloomberg. “I think the answer has to be yes,” Chicago Fed President Charles Evans said this month when asked whether low inflation could be grounds for a cut. “If core inflation were to move down to, let’s just say, 1.5 percent,” that would indicate the current level of rates “is actually restrictive in holding back inflation, and so that would naturally call for a lower funds rate, at least so that it was accommodative.” By that thinking, monetary policy is more restrictive than any time since 2008, given that the Fed’s 2.50 percent target rate exceeds the core PCE rate by almost 1 percentage point. But this isn’t just a U.S. phenomenon. Prices of tradeable goods rose less than 1 percent in the first quarter, down from gains of 3.7 percent on average in 2018, according to Medley Global Macro Managing Director Ben Emons. Bond traders certainly see little reason to take out protection against the potential for faster inflation. The Bloomberg Barclays Global Inflation Linked Bond Index has lost 0.94 percent this month through Friday, the second-worst performer among the 20 major global bond market indexes, exceeded only by the 1.04 percent drop in Chinese bonds. A rate cut with the economy in decent shape has precedence. Recall that the Fed lowered rates in mid-2003 to stave off deflation even though gross domestic product expanded by 3.5 percent in the second-quarter of that year.

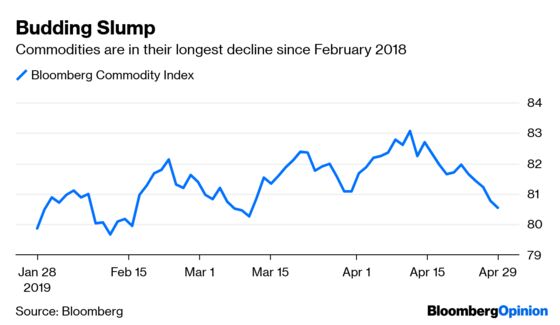

THERE’S NO INFLATION IN COMMODITIES

The commodities markets is often a good barometer of inflation. But despite oil prices having just reached their highest since October, the broader commodities market is going in the opposite direction. The Bloomberg Commodity Index fell for the fifth consecutive day on Monday, its longest slump since February 2018. The gauge is now at its lowest since early March. In addition to relatively soft demand given the slowdown in the global economy, the commodities market is also suffering from oversupply, especially in agriculture sectors. The International Grains Council on Thursday raised its estimate for inventories next season by about 2 percent amid higher output and lower consumption. That may further weigh on prices that have slumped in recent months and comes as money managers’ bearish wagers are near the highest on record, according to Bloomberg News’s Nicholas Larkin. There’s also the potential for rising gasoline prices to damp consumer spending, which could also contain inflation. Prices for a gallon of regular grade gasoline have risen to an average of $2.89 heading into the all-important summer driving season, according to the Automobile Association of America, up from January’s low of $2.23 a gallon. That normally wouldn’t be problem in a strong economy, but sluggish wage growth may be forcing consumers to dip into their savings to service rising debt loads. U.S. government data show the savings rate fell by 0.8 percentage point in March to 6.5 percent, the biggest decline since 2013. And consumer spending, the largest chunk of the economy, cooled for the third straight quarter in the first three months of 2019.

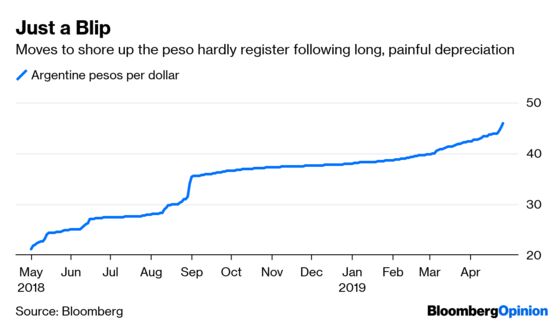

ARGENTINA TAKES DRASTIC ACTION

The foreign-exchange market was focused on Argentina Monday, where the peso rose as much as 3.77 percent for its biggest gain since the start of October after the central bank said it would step up intervention in the currency market. The peso’s problems have been well known and persistent, but before declaring the sizeable gain on Monday as a turning point, consider that the currency is still down about 54 percent over the past 12 months. Then consider that this is the fourth change in currency policy in six weeks, which suggests that the authorities are floundering around for a solution to the peso’s weakness. "It’s a bit uneasy, the need to frequently adjust their strategy and increase firepower," Daphne Wlasek, macro strategist at XP Investments in New York, told Bloomberg News. But, "any measure to ensure the FX stability is positive." The central bank said it will start to sell dollars to stabilize the peso, overturning a previous pledge not to intervene if the currency remained within a limited trading band, according to Bloomberg News’s Patrick Gillespie and Jorgelina do Rosario. Argentina’s central bank had $71.9 billion in foreign reserves as of Friday that it can tap to stabilize the peso. The new measures follow a tough week for Argentina bonds, with some yields rising to as high as 20 percent from 13 percent as inflation reached 55 percent. The peso depreciated almost 9 percent last week, driven mostly by a poll that showed market-friendly President Mauricio Macri could lose a runoff vote this November against his populist predecessor, Cristina Fernandez de Kirchner.

TEA LEAVES

In a busy week for global economic data, the euro-zone gross domestic product figures due to be released Tuesday will be among the most closely watched. The median estimate of economists surveyed by Bloomberg projects the region’s economy expanded by 0.3 percent in the first quarter from the final three months of 2018. Although that headline number won’t get anyone’s heart racing, there should be plenty of evidence that the euro zone may be on the mend. Given the amount of trade that the region does with the rest of the world, the results could support the idea that perhaps the global economy is stronger than believed. “The balance of risks around the euro-area outlook is finally shifting,” Bloomberg Economics wrote in a research note Monday. “GDP growth probably remained subdued in (the first quarter), but the high-frequency hard data, which are better indicators than the surveys, suggest there’s room for an upside surprise.” That’s not a lonely thought. “Europe’s economy looks to be on the cusp of recovery — a potential support for the region’s lagging risk assets,” Richard Turnhill, BlackRock’s global chief investment strategist, wrote in a research note Monday. “We expect the European economy to pick up pace in the second half of 2019. Financial conditions have eased significantly since the start of the year, and China’s stimulus efforts could boost capital spending — a potential boon for Europe’s manufacturers.” To be sure, it’s too early to sound to sound the all clear. As Turnhill notes, trade tensions between the U.S. and Europe may heat up, and while economic fallout should be manageable, there’s the potential for an “outsized” impact on markets.

DON’T MISS

The Fed Might Have Drawn Markets Into a 'Dove Trap': Tim Duy

Questions to Hang Over No-Drama Fed Meeting: Mohamed A. El-Erian

The Junkiest Corporate Bonds Divide Wall Street: Brian Chappatta

Trump’s Tax Cuts Aren’t Doing What They Should: Mark Whitehouse

Dirty Russian Oil Has Made a Fragile Market Worse: Julian Lee

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.