Let Me Count the Ways Stock Markets Are Tanking

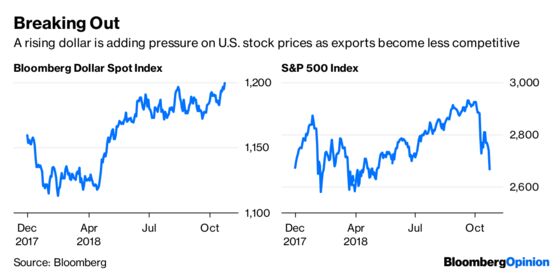

(Bloomberg Opinion) -- Stocks in the U.S. have been under a lot of pressure lately, with the S&P 500 Index giving up its gains for the year on Wednesday after being up as much as 10 percent in late September. The conventional wisdom is that the weakness is largely due to rising interest rates and the prospect for slower profit growth next year. Less talked about, but perhaps just as important, is the dollar, which has been strengthening again for reasons that have nothing to do with confidence in the U.S. and could well add to the recent woes in equities.

The Bloomberg Dollar Spot Index — which tracks the greenback against its major peers — rose on Wednesday to its highest level since mid-2017, breaking out of a trading range it's been stuck in since June. The move higher came as the euro took a tumble following a dismal Purchasing Managers’ Index report that showed euro-area growth slowed to the weakest in more than two years at the start of the fourth quarter as manufacturers suffered from mounting concerns over global trade. But the euro zone is hardly alone. The Citigroup Inc. economic surprise index covering the world's major economies show that incoming data is falling short of estimates by the greatest degree since early July. The bad news for U.S. stock investors, which have watched the S&P 500 Index tumble about 7.5 percent this month, is that a rising dollar adds to what are already tighter financial conditions. It also makes U.S. exports less competitive. Jodie Gunzberg, managing director and head of U.S. equities at S&P Dow Jones Indices, wrote in a blog post in May that the S&P 500 rises 3.7 times more from a falling dollar than a rising one. So, all else being equal, a stronger greenback is a major headwind. That can be seen in the U.S. merchandise-trade deficit: a government report Thursday will likely show it held above $75 billion for the second month in a row in September, marking the first such back-to-back occurrence.

Even before Tuesday's move higher in the dollar, some big companies were lamenting its relative strength. Officials at 3M Co. said on the company's earnings conference call earlier this week that "foreign currency, net of hedging, reduced per-share earnings by $0.08 as the U.S. dollar strengthened against many currencies throughout the quarter." For the full year, 3M now expects an earnings drag from foreign currency "of minus" 5 cents per share versus a prior "estimated benefit" of 10 cents. It's only a matter of time before President Donald Trump starts complaining about a strong dollar again.

MARKET MELTDOWN CONTAGION

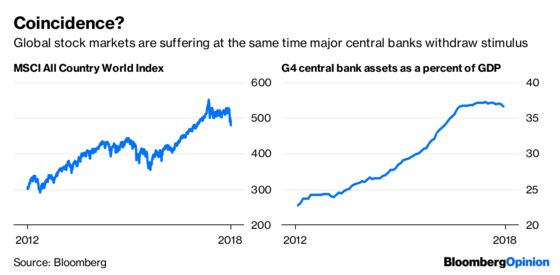

The broad MSCI U.S. Index of stocks fell for the sixth straight day, tumbling 3.11 percent. That benchmark is now down 0.74 percent for the year. But for all the recent focus on the troubles in the U.S. stock market, it's important not to lose sight of what's happening in the much of the rest of the world, where it's much worse. German stocks hit a new low for the year on Wednesday, and are now down 13.4 percent in 2018. French stocks also hit a new low for the year, bringing their losses to 6.77 percent. Italy's down 15.4 percent, while U.K. equities have lost 9.43 percent. Chinese stocks are lower by about 20 percent, and Japanese stocks are down as well. The same is true of Canada and Mexico. The list goes on. In fact, the MSCI All Country World Index is now down 6.97 percent, already making this the worst year since it fell 9.42 percent in 2011. It's not hard to identify the reasons for the weakness in stocks, which range from escalating trade tensions to hawkish central banks. But some strategists wonder whether it's time to start to talking about a global synchronized economic slowdown — or worse. "One could dismiss one or two of these data points as outliers," DataTrek Research co-founder Nicholas Colas wrote in a research note Tuesday in reference to the drop in major equity indexes globally. "But taken as a whole they clearly show global macro concerns over worldwide economic slowing and possibly a synchronized recession."

DOVES ARE A DYING BREED

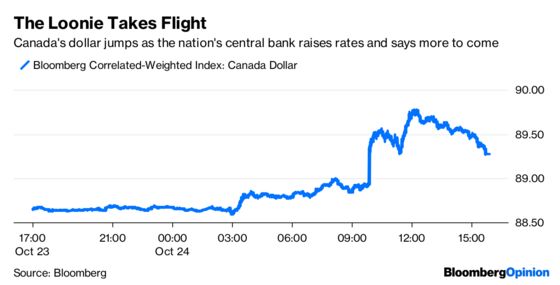

Speaking of hawkish central banks, the Bank of Canada sent that nation's currency soaring Wednesday by raising interest rates for the third time this year and acknowledged for the first time in more than a decade it expects to completely remove monetary stimulus from the economy. That's central banker code for “further rate hikes are on the way.” The Bloomberg Correlated-Weighted Index for the Canada dollar, which measures the currency against its major peers, rose as much as 1.27 percent in the biggest gain since December. By that measure, the so-called loonie is now the best performing major currency over the past three months. “The reality is the economy is running at its capacity and it is no longer needing stimulus, and so it’s our job to prevent the thing from overheating,” Governor Stephen Poloz told reporters at a press conference after the decision. That's the type of talk that is spooking investors, who see central bankers looking for any excuse to raise rates despite mounting evidence of softness in the global economy. The decision to boost rates comes just a few days after Canada's government data showed a decline in both retail sales and inflation. Economists surveyed by Bloomberg see Canada's economy expanding at a tepid 2.2 percent rate this year and 2.1 percent in 2019. The nation's stock market didn't take kindly to the move, as the benchmark S&P/TSX Composite Index fell as much as 1.88 percent to its lowest level since September 2017.

CORPORATE DEBT ADDS TO JITTERS

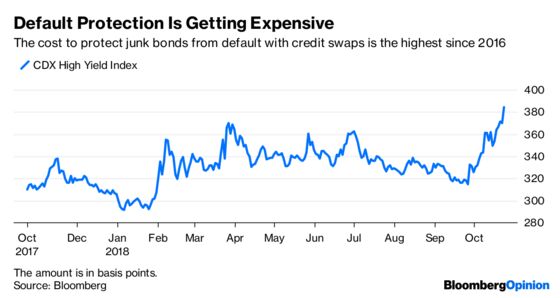

More than a few market participants are pointing to the seemingly benign reaction in credit markets, especially junk bonds, as evidence that the selloff in stocks is nothing to get too worried about. “High yield is not confirming the downside move in equities and high yield is usually right,” Tom Lee, head of research at Fundstrat Global Advisors, wrote in a note. "Macro developments impacting equities also impact high yield — for instance, late-cycle fears would hit both as would earnings-per-share-risk from trade tensions." Perhaps, but there's one measure of the health of credit that sending up a red flag: credit-default swaps. An index of the derivatives shows that investors are paying the most since 2016 to protect against defaults by high-yield borrowers. A debt binge has boosted U.S. nonfinancial corporate debt to $14.8 trillion as of mid-2019, the Institute of International Finance said in a research report Wednesday. What's most concerning is that the despite the booming U.S. economy, close to 20 percent of borrowers — mainly smaller ones — are facing difficulty in covering interest expenses. "The problem is particularly acute for small-cap firms—more than half have very weak interes- coverage ratios," the IIF said in the report. Other metrics showed that the corporate debt-to-GDP ratio stands at about 72 percent, just below its all-time high in early 2008. Alternatively, the debt-to-assets ratio is the lowest since 2007, "reflecting the significant rise in the market value of corporate assets and robust growth in firms’ balance sheets." True, but that ratio means little if borrowers can't service their debt.

MORE PRECIOUS THAN GOLD?

Looking for a haven to hide out from the market turmoil but are too scared about owning government bonds, with central banks sounding a bit too hawkish and concerns about inflation stirring? In that scenario, gold might be the obvious choice, but there's another metal that's poised to become even more precious. Palladium climbed to a record this week on concern about tighter supplies of the metal, which is mainly used in catalytic converters that curb vehicle emissions, bringing its gain for the year to 6.11 percent. Gold, meanwhile, is down 5.54 percent. The price of palladium is now the highest relative to gold since 2002. Not only is it the best-performing precious metal this year, but it could be more expensive than gold by early next year, according to Bloomberg News's Marvin G. Perez, who cited James Cordier, the founder of Optionsellers.com. The rally in palladium accelerated in recent days amid growing political tensions between the U.S. and Russia, one of the top producers of the metal. More broadly, the metal has been supported by consumers turning toward gasoline cars, which tend to use more palladium in autocatalysts, instead of diesel. Output will trail demand by 481,000 ounces this year and deficits will persist through 2020, leading to the “tightest” market in two decades, Citigroup said in a note in late September.

TEA LEAVES

Will the third time prove to be a charm? The first two auctions this week of coupon-bearing notes by the U.S. Treasury Department were met with indifference despite the big rebound in the bond market as investors seek a haven from the sell-off in equities. At Tuesday's sale, $38 billion of two-year notes drew bids for 2.67 times the amount offered, below the average over the past 12 months of 2.78 times. Then on Wednesday, the auction of $39 billion in five-year notes drew a bid-to-cover ratio of 2.30 times, the lowest since February 2017. Perhaps the soft demand has something to do with the increased borrowing by the U.S. government to pay for a soon-to-be $1 trillion budget deficit. The sizes of the two- and five-year note auctions were both the most since 2010, when the government was reducing its borrowing as the financial crisis began to pass. The government's debt auctions wrap up for the week on Thursday with the sale of $31 billion in seven-year notes. Another bad reception could get bond traders to rethink the rally.

DON'T MISS

What's Wrong With the 2 Percent Inflation Target: Paul Volcker

How Trump's Attacks on Powell Are Helping the Fed: Karl W. Smith

Put Down the Charts. Oil's Rally Isn't Over Yet: David Fickling

Stocks Are On the Brink of a Bear Market: Stephen Gandel

Boeing Is the Big Exception to Earnings Gloom: Brooke Sutherland

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.