Forget the Midterms. The Real Action Is in Stock Buybacks.

(Bloomberg Opinion) -- The broad market for equities as measured by the MSCI USA Index of stocks rallied Monday. That gauge has now risen in four of the past five trading days, an impressive performance given how bleak the outlook for stocks seemed to be a week ago. One might be tempted to link the rebound with optimism for some change in Washington with the midterm elections coming on Tuesday. That would be a mistake for a number of reasons.

Instead, this mini renaissance in stocks is all about buybacks and the expectation that companies will ramp up repurchases now that earnings season is winding down. That, too, might be a mistake-in-waiting. U.S. flow of funds data from the Federal Reserve point to a deceleration in the repatriation of dollars held overseas by companies, according to JPMorgan Chase & Co. strategists led by Nikolaos Panigirtzoglou. They wrote in a report late Friday that the 15 U.S. companies with the highest cash holdings reported so far in the third quarter experienced a decrease in those holdings of just $6 billion during the period. That compares with a reduction of $47 billion in the second quarter and $80 billion in the first quarter. In addition, announced U.S. buybacks have been decelerating, culminating in a weak October. Although many might say the slowdown in October was due to companies taking a break as they reported earnings, the JPMorgan strategists pointed out how buybacks peaked for the year in July, which was the height of second-quarter earnings season. “If this trend continues, the extra boost that U.S. repatriation provided to U.S. equity and bond markets via share buybacks and corporate bond redemptions is largely behind us,” the strategists wrote.

If the comments from JPMorgan sound both familiar and confusing at the same time, you’re not going crazy. JPMorgan’s all-world analyst Marko Kolanovic issued a report last week that discussed the possibility that the October “rolling bear market” turns into a “rolling squeeze higher” into the end of the year. One reason he cited was the notion of a surge in corporate stock buybacks after earnings season. It’s not unusual for different parts of the same Wall Street firm to issue seemingly contradictory calls. The strategists would say it promotes a healthy debate. Perhaps, but it also shows that nobody has the same crystal ball.

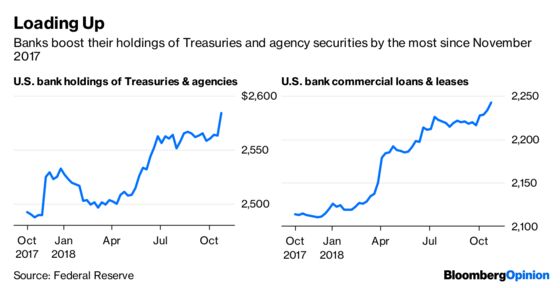

BANKS BINGE ON BONDS

Fed data released late Friday showed that U.S. commercial banks added $21 billion of Treasuries and government agency securities to their holdings in the week ended Oct. 24, the most since November 2017. That boosted their holdings to a record $2.58 trillion. There are two ways to think about this. The pessimists might say that the buying frenzy suggests that the nation’s banks, which are in the best position to get a feel for the economy in real time, are worried and feel it’s a good time to stock up on super-safe assets. Indeed, most economists are forecasting a marked slowdown in growth in coming quarters as the economy comes down from a “sugar high” as the benefits from this year’s corporate tax cuts fade and rising debt loads bite. Also, if the Democrats regain control of the House, it could lead to political gridlock and thwart Republican efforts to further juice the economy. That would be bad for equities. The other way to think about all this is that it’s logical that banks would load up on bonds because more of them are outstanding. Total marketable U.S. government debt outstanding has risen to $15.3 trillion from about $4.5 trillion before the financial crisis. Plus, at 3.71 percent, yields on government-related securities are the highest since 2008. But what’s truly interesting is that banks have also stepped up their lending. After three months with little change, U.S. commercial loans and leases jumped in October, rising $26.2 billion to $2.24 trillion. That suggests banks are bingeing on bonds because they sense a bargain rather than a looming economic threat.

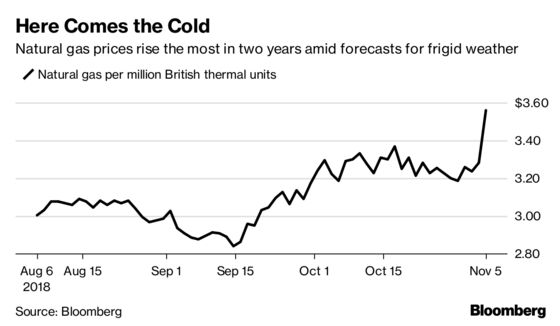

NATURAL GAS MAKES A MOVE

The eyes of the commodities market were on oil as U.S. sanctions on Iran took effect. They should have been on natural gas, which soared as much as 8.89 percent on Monday for its biggest intraday gain since October 2016. Prices are now up about 20 percent for the year. The surge came as forecasts turned sharply colder for the eastern and central regions of the U.S. One weather model shows the icy blast extending into Thanksgiving, according to Commodity Weather Group LLC, a pattern also seen in the winter of 2013-2014 when the “polar vortex” sent gas prices to a six-year high, according to Bloomberg News’s Naureen S. Malik and Christine Buurma. The rally underscores the market’s vulnerability to supply constraints as stockpiles enter the winter at a 15-year seasonal low. Demand has surged amid record exports and as power plants and industrial users burn more of the fuel at home and abroad. Though production from shale basins has climbed to an all-time high, gas bulls are betting that the output gains won’t be enough to meet heating needs. Money managers’ net-long bets on gas are hovering near a nine-month high, U.S. Commodity Futures Trading Commission data show. Hedge funds are “going to go for what’s hot, and it’s natural gas,” Bob Yawger, director of the futures division at Mizuho Securities USA Inc., told Bloomberg News. The jump in natural gas prices may offset some of the good news for consumers from the recent drop in oil prices, which has resulted in the lowest gasoline prices since March.

ICELAND IS HEATING UP

Iceland is rarely — if ever — in the spotlight, but it came extremely close on Monday. The OMX Iceland All-Share Index had a huge day, rising as much as 5.28 percent in what would have been its biggest gain since 1993. A late pullback left the 18-member benchmark up a still impressive 3.91 percent, good for its biggest one-day rally since 2014. The surge came after the nation’s central bank late Friday cut its special reserve ratio imposed on some foreign investments in half, to 20 percent, according to Bloomberg News’s Ragnhildur Sigurdardottir. The move was done to shore up the local currency, the krona, which had slumped 14 percent from its 2018 high amid concern that economic growth was slowing amid troubles in the nation’s booming tourism industry and contentious wage talks. Unions are seeking wage increases of more than 40 percent over the next three years for the lowest paid workers. It didn’t receive a lot of attention, but Iceland’s economy was among the hardest hit when the financial crisis struck a decade ago, causing its currency to depreciate rapidly. As recently as earlier this year, the central bank was hesitant about lifting measures defending the currency on concern that doing so could lead to a repeat of the type of practices that caused its economy to crash in 2008. The change in the reserve requirement precedes a rate-setting meeting Wednesday. Economists are split as to whether the seven-day term deposit rate will be held at its current level of 4.25 percent or whether a hike is coming, Sigurdardottir reports.

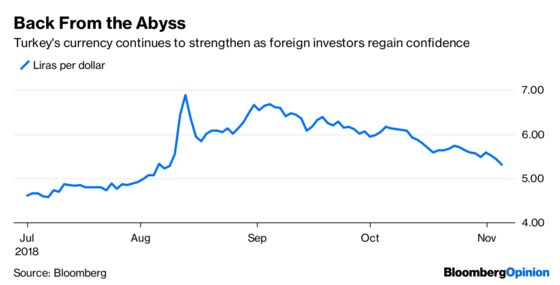

TURKEY’S ON THE MEND

Things couldn’t have looked bleaker for Turkey at the end of August. President Recep Tayyip Erdogan had tightened his grip on power and installed his son-in-law as the economy czar, raising questions about the central bank’s independence. Also, Turkey was facing off against the U.S., which was threatening sanctions over the detention of American pastor Andrew Brunson on terrorism and espionage charges. But Turkey looks to be on the mend, at least from the view of financial markets. Brunson is back in the U.S. and the lira has appreciated 29 percent since its low on Aug. 13. Also, Turkey’s stock market is benefiting from signs of improved economic performance while the cost to insure the nation’s debt against default has come way down. Data on Monday showed that producer prices slowed for the first time in nine months and core inflation rose less than the median estimate in a Bloomberg News survey, according to Bloomberg News’s Constantine Courcoulas. There are also signs that relations between the U.S. and Turkey may be thawing, with Erdogan saying over the weekend that he had talked with U.S. President Donald Trump and the two planned to meet in Paris on Nov. 11-12.

TEA LEAVES

U.S. voters head to the polls Tuesday in the highly anticipated midterm elections. Surveys suggest the Democrats will retake the House while Republicans retain control of the Senate. In other words, get ready for policy gridlock. Normally, as the Wall Street cliché goes, gridlock is good for markets because lawmakers can’t do anything that would harm to the economy. But that’s unlikely to be the case this time, at least in the short term. The consensus among market participants is that if the elections play out as expected and the Democrats gain control of the House, that would be a negative for equities and the dollar while boosting bonds. The thinking is that the Democrats would block further business-friendly actions that would worsen the U.S. fiscal situation. Think middle-class tax cuts. There would also be less of a need for further interest-rate increases by the Fed. But if the Republicans retain control of both chambers, then expect to see a rally in stocks and the dollar while bonds continue to weaken. Of course, markets have a way of doing the one thing that causes the most amount of pain, so don’t be surprised if expected reactions fail to come true. Remember how everybody thought a Trump presidency would be bad for risk assets? That only lasted a few hours on election night.

DON’T MISS

Best Tool for Understanding Markets and Trump: Barry Ritholtz

Hedge Funds, Mom and Pop Agree on Midterm Trade: Brian Chappatta

Fed’s Rosy Outlook Snubs History: Danielle DiMartino Booth

Tech Stocks Are Down, But Don’t Ignore FANG Put: Stephen Gandel

Diverging Economies Will Drive Markets: Mohamed A. El-Erian

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.