Starbucks Can’t Afford Any Slip-Ups In China

Its ambitious expansion there is on track but not roaring, and it faces challenges — including a feisty homegrown competitor.

(Bloomberg Opinion) -- If you were worried that Starbucks Corp.’s Thursday earnings report would add to the gloomy picture that Apple Inc. recently painted of the Chinese consumer, you can relax.

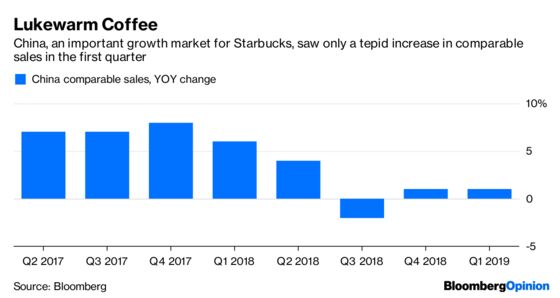

The coffee giant said comparable sales grew 1 percent over a year earlier in China. It’s not exactly a roaring increase, but it’s the same pace of growth that Starbucks recorded on this measure in its previous quarter, so it shows the company hasn’t seen a sudden disturbance to its business there.

And yet, investors shouldn’t feel excessively comforted by Starbucks’s latest showing in China, which the company has called its “second home market.” It remains at the low end of what the Starbucks has promised over the long term, and is significantly slower than what it was even a year ago.

Starbucks’s performance in China isn’t being shaped so much by political brinkmanship or economic headwinds; instead, it faces more prosaic challenges.

First, Starbucks is feeling the heat of an insurgent competitor. Luckin Coffee, a Chinese startup, has been on a tear, as my colleague Nisha Gopalan has noted. It launched a little more than a year ago and quickly has gained traction, helped by its focus on speedy delivery and discounts. Luckin is valued at $2.2 billion, Bloomberg News has reported, and it plans to grow to an eye-popping 4,500 locations by the end of 2019. For context, Starbucks has been in China since 1999, and as of December, it had about 3,700 stores there.

Starbucks is playing defense, including entering a partnership with Alibaba Group Holding Ltd. that allows it to offer delivery. But Luckin has come on extraordinarily fast and strong, and Starbucks is seeing the effects.

That’s not to say Starbucks is moving slowly with its own expansion these days. The company has said it is opening a store about once every 15 hours in China as part of a push to create a portfolio of 6,000 locations by 2022. The idea is to make sure it has early-mover advantage, blanketing the country with cafes even before a robust coffee-drinking culture has widely taken hold.

There’s logic to that strategy, but it’s not without downsides. In fact, it is likely weighing on the company’s comparable sales growth in the near term as new locations cannibalize business from old ones. Starbucks executives have said the bulk of its long-term sales growth in China is going to come from opening new stores, not from comparable sales growth. But I still can see why it might make investors skittish that older stores aren’t building more of a following.

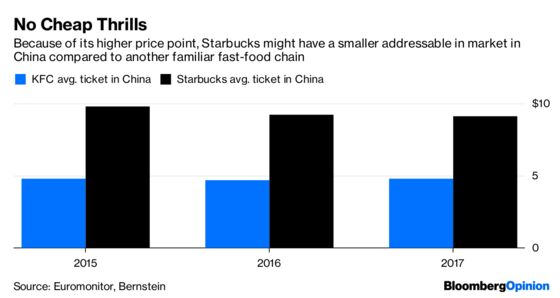

That’s especially true when you consider the challenges Starbucks faces in penetrating markets beyond top-tier cities such as Shanghai. As Sara Senatore, a restaurant-industry analyst at Bernstein has noted, Starbucks’s relatively high prices make it more difficult for the chain to make inroads in metropolitan areas where incomes aren’t as high. This challenge could be exacerbated if China’s economy darkens.

Starbucks can ill afford misfires in China. While its U.S. comparable sales exceeded analysts’ expectations this quarter, rising 4 percent from a year earlier, the growth was once again fueled entirely by higher average checks. Transactions, a proxy for traffic, were flat from a year earlier, suggesting it has work to do in its home market.

If it could rev into higher gear in China, it might be easier to overlook those signs of saturation in the U.S.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

©2019 Bloomberg L.P.