(Bloomberg Opinion) -- The Bloomberg Dollar Spot Index rose the most in more than a month on Thursday, which isn’t surprising given that the Federal Reserve raised interest rates again on Wednesday. After all, higher rates tend to attract foreign capital. What is surprising is that traders shouldn’t get used to many more big days for the greenback if JPMorgan Chase & Co.’s all-world analyst Marko Kolanovic is to be believed.

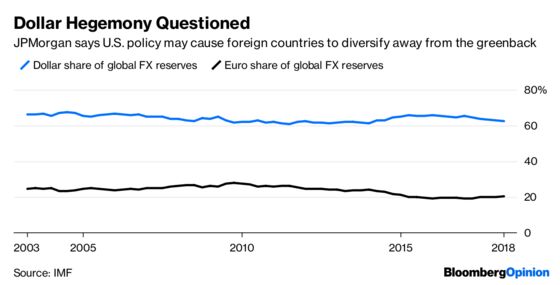

Kolanovic, who has dominated Institutional Investor’s annual rankings of top strategists for a decade or so, was out with a research note Thursday arguing that President Donald’s Trump’s isolationist foreign policy is a “catalyst for long-term de-dollarization.” Put another way, the dollar is in jeopardy of no longer being the world’s primary reserve currency and all the benefits that go along with that, such as interest rates that are lower than they otherwise might be and the government’s ability to fund budget deficits in perpetuity. “With the current U.S. administration policies of unilateralism, trade wars, and sanctions increasingly affecting both friends and foes, the question arises whether the rest of the world should diversify away from the risks of the U.S. dollar and dollar-centric finance,” Kolanovic and his team of quantitative and derivatives strategists wrote in the note, according to Bloomberg News’s Cecile Gutscher. To be sure, this won’t happen overnight, and any shift away from the dollar would take many years, but the warning serves to highlight a topic that is increasingly being discussed. That’s why Friday’s International Monetary Fund report on global currency reserves is most likely to get more attention than usual.

The IMF data will cover the April through June period, when the Bloomberg Dollar Spot Index snapped five consecutive quarterly losses and gained 5.02 percent. Based on that performance, it’s likely the dollar’s share of global reserves edged up from 62.5 percent at the end of the second quarter but still down from the 64.7 percent when Trump took office. “U.S. unilateral policies risk bringing major powers of China, Europe and Russia closer, and such an alliance could profoundly impact the dollar-centric financial system,” the JPMorgan strategists added in the note.

FINANCIAL REPRESSION LIVES

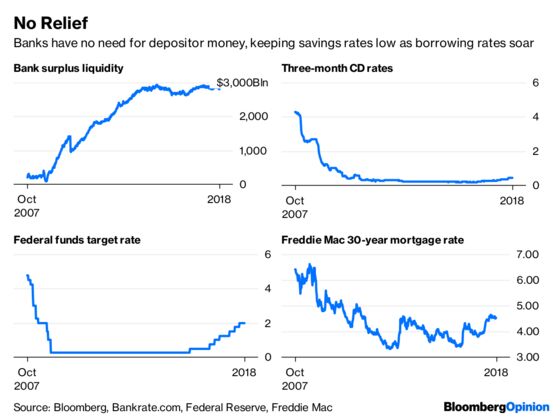

In a press conference Wednesday, Trump lamented the Fed’s decision to raise rates for the eighth time since December 2015 but offered that it’s good for savers. In reality, one would be hard pressed to find any happy savers. Despite the Fed raising its target federal funds rate from near zero in 2015 to the current range of 2 percent to 2.25 percent, rates on three-month certificates of deposit have increased from 0.20 percent to just 0.46 percent on average, according to Bankrate.com. The reason banks aren’t offering higher rates is because they don’t need the money. Fed data show surplus liquidity at U.S. banking institutions stands at $2.80 trillion, up from about $250 billion before the financial crisis. This goes a long way toward explaining the big gains in housing and why the current bull market in stocks, which last month became the longest on record, shows few signs of reversing soon. In short, savers can either watch their purchasing power erode sharply over time by keeping cash in time deposits that pay far less than the inflation rate or funnel their cash into risky assets. Maybe that’s why the S&P 500 Index snapped a four-day losing streak on Thursday.

WHEN CONVENTIONAL WISDOM FAILS

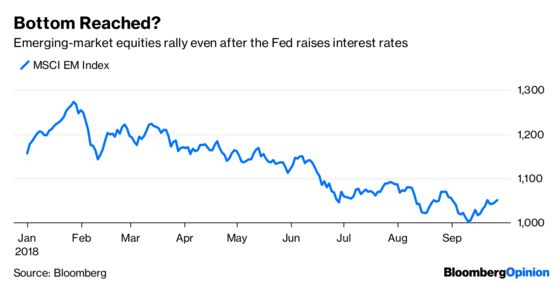

Most market participants blame the big sell-off in emerging markets this year on the Fed’s rate increases and a stronger dollar. That sounds logical, but only if you’re willing to overlook some inconvenient truths, such as a banner year for emerging markets in 2017 even though the Fed boosted rates four times in 12 months. On top of that, emerging markets reacted quite favorably to Wednesday’s Fed rate increase, with the MSCI EM Index of equities rising 0.91 percent over the course of two days and the MSCI’s sister index of EM currencies jumping 0.44 percent. After EM equities fell as much as 21.2 percent this year through Sept. 11 and EM currencies depreciated as much as 8.76 percent, perhaps the slump in the MSCI indexes has run its course. Bonds of Argentina, a country that has been a big source of turmoil in EM this year, rallied on Thursday, a day after the IMF boosted the size and upfront disbursements of a record credit line that insures that the nation’s financing needs will be covered through next year’s presidential election. More and more big money investors are saying it’s time to jump back into EM. Jordi Visser, the chief investment officer at the $1.7 billion hedge fund Weiss Multi-Strategy Advisers and one of the few people who earlier this year predicted a “significant correction” in emerging-market assets, said recently that a rebound may be looming.

OIL AND YEN DON’T MIX

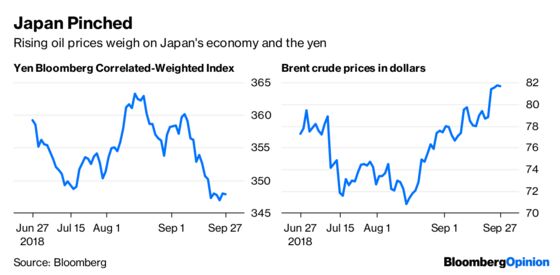

Japan’s currency is under pressure, with the Bloomberg Correlated-Weighted Index of the yen versus its major peers dropping 4.3 percent since mid-August. The yen fell on Thursday to its weakest level against the dollar since December. To understand what is happening to the yen, you need to understand what is happening in the market for oil. Brent crude has risen to its highest level since 2014 this week, reaching $82.55 a barrel. West Texas Intermediate isn’t far behind, rising above $70 a barrel from about $50 a year ago. This puts Japan in a significant bind — more so than even potential tariffs threatened by the Trump administration — because its economy is dependent on importing oil. Bloomberg Intelligence economist Yuki Masujima put things in perspective in a research note Wednesday. He figures that an increase in U.S. tariffs on imports of Japanese cars to 25 percent could reduce Japanese car makers’ profits by 1 trillion yen ($8.2 billion). A rise in oil prices to $80 a barrel from $70, though, could deal a heavier blow, reducing Japan’s trading gains by 1.7 trillion yen. “Japan relies heavily on imported oil, so a price decline could deliver a significant boost to its terms of trade,” Masujima wrote.

TRUMP SAID WHAT?

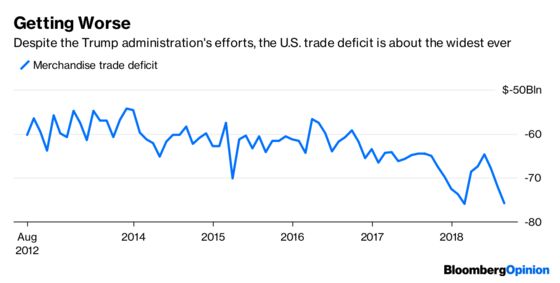

Trump said this week that the tariffs that he has imposed on other countries have had no effect on the U.S. economy. That was before Thursday’s Commerce Department report on the merchandise-trade deficit, which unexpectedly grew in August to $75.8 billion, the widest in six months and close to a record. A decline in food, industrial supplies and auto exports primarily accounted for the bigger shortfall, according Bloomberg News’s Shobhana Chandra. On top of that, Chandra reports that a separate report from the department signaled corporate investment took a breather, with business-equipment orders at U.S. factories falling in August after a run of strong gains while shipments of those items slowed. Economists at JPMorgan Chase & Co., Amherst Pierpont Securities and Capital Economics trimmed their estimates for third-quarter gross domestic product growth. Before Thursday’s data, the median estimate in a Bloomberg survey was for 3 percent expansion. “The data are grim,” Ian Shepherdson, chief economist at Pantheon Macroeconomics, wrote in a research note, referring to the August goods-trade gap. “The administration’s narrative, that the second-quarter drop in the deficit was a result of their trade policies, has now fallen apart, as it was always likely to do.” If the economy is slowing, then it’s increasingly unlikely that yields on benchmark 10-year Treasury yields can remain above 3 percent much longer.

TEA LEAVES

Despite the lowest unemployment rate in 20 years, one would think that U.S. workers are enjoying huge raises, but they aren’t. There are plenty of theories for why that is, from the diminishing influence of unions to technological advances. The Commerce Department will provide an update on the situation Friday when it releases its monthly data on personal income and spending for August. The median estimate of economists surveyed by Bloomberg is that incomes jumped 0.4 percent last month, but they have been disappointed before. That was what they forecast for July only to see the number come in at 0.3 percent. Personal spending is seen rising 0.3 percent after increasing 0.4 percent in July.

DON’T MISS

Higher U.S. Yields Should Worry Europe: Mohamed A. El-Erian

Why America Ended Up With a Two-Track Economy: Barry Ritholtz

Investors Expect to Be Rewarded for Risk, Right?: Nir Kaissar

Bitcoin Runs on Paranoia, and That’s the Beauty of It: Elaine Ou

Forget Tantrums, Emerging Markets Are the Haven Now: Shuli Ren

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.