(Bloomberg View) -- Has the U.S. economy finally achieved that elusive so-called escape velocity?

Sure, Federal Reserve Chairman Jerome Powell said in testimony to Congress on Feb. 27 that "some of the headwinds the U.S. economy faced in previous years have turned into tailwinds," comments that led market participants to begin pricing in four rate hikes this year. And the jobs data for February, released Friday, added fresh fodder to that perception. But what should we think when two notorious Fed doves echo the new chairman verbatim?

Fed Board Governor Lael Brainard has always been judicious in using FedSpeak; her public appearances are few and far between and noteworthy for that very reason. It was telling that a March 6 speech was titled "Navigating Monetary Policy as Headwinds Shift to Tailwinds."

Chicago Fed President Charles Evans used similar phrasing -- "headwinds have become tailwinds" in a CNBC interview on Friday that followed the release of the stronger-than-expected jobs data for February.

Investors should pay heed to the news that the most dovish Fed officials are on board with a more aggressive tightening path. After all, the doves’ chief aim has been to pull idled workers back into the workforce and to reverse the assumption that droves of able-bodied workers have been sidelined indefinitely. And that’s exactly what’s happening.

Beyond the headline number of 313,000 employees added to nonfarm payrolls last month, the real excitement came from the household survey data, which produces the unemployment rate and showed job gains of 785,000. Of those, 446,000 went to those aged 25-54, a cohort Powell cited many times in his inaugural congressional testimony.

In all, the number of those not in the labor force but capable of working fell to 95.4 million from 96.7 million. Looked at slightly differently, on a non-seasonally adjusted rate, more than 1.55 million workers rejoined the labor force, the largest single increase since 1991.

As encouraging as the news is, what investors should care about, and what markets theoretically reflect, is what’s to come. Looking over the near-term, the news is even better, which explains the markets’ euphoric reaction to the jobs data.

The average time a worker was unemployed in February fell to 22.9 weeks, the shortest since May 2009. Delving deeper, the percentage of workers who’ve recently left their jobs and were unemployed for fewer than five weeks rose to 42 percent, the highest since late 2006. In the case of this particular "good" unemployment rate, the higher it is, because an increase indicates that workers are jumping ship for better opportunities, a sign of building wage inflation.

So, demand for workers is far outstripping supply. The hard data are corroborating the soft data of recent months, if not years: Securing skilled laborers is as challenging as anything employers can recollect.

Nonetheless, the latest numbers also had some troublesome signs that should be on investors’ radars. Retailers added 50,000 employees to their payrolls in a month of announcements of accelerated store closures. Since February, news has hit that Claire’s stores would file for bankruptcy protection and that Toys ‘R’ Us is on the cusp of liquidation. Clearly, something is amiss.

The latest Challenger, Gray & Christmas layoff data provide some insights. The number of employers that cite cost-cutting as the reason for reducing payrolls has fallen to near zero; those citing store closures and restructuring have picked up in recent months. Both of these trends seem set to continue. In the meantime, look for a rise in layoffs tied to M&A in the aftermath of a rash of tie-ups stemming from the tax reform legislation.

On a more fundamental level, what are the odds that the demand for labor is sustained? In February, the construction sector added 61,000 jobs, the biggest increase in 11 years. Over the last four months alone, it has added 185,000 new jobs.

A warming trend after a brutally cold January probably played a part. And the four-month surge in hiring was preceded by three hurricanes and two wildfires. Still, strong single-family housing starts suggest builder demand for new construction could offset waning demand as repairs from the storms are completed.

Manufacturing has similarly benefitted from idiosyncratic forms of demand, namely a weak dollar and strong sales of supplies to rebuild and repair storm damage. Notably, demand for temporary workers was the strongest in 17 months, a sign that the need for workers is spread wide across a number of sectors.

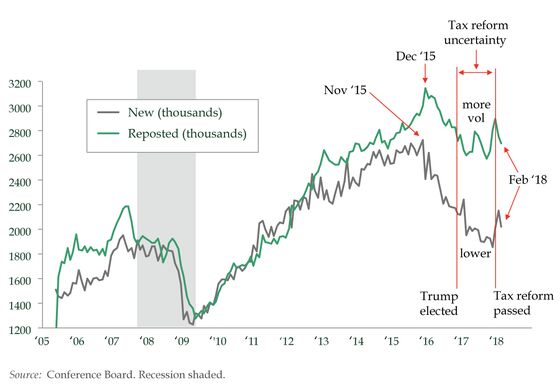

The Conference Board’s help-wanted series offers perspective about whether these trends will continue. After peaking in late November 2015, new ads began a slow march lower. Over the past few months, though, signs of life have re-emerged.

Dig a bit deeper and net out jobs that are reposted month-in and month-out and you see a similar breakout to the upside. Both new positions and repostings will continue to rise if the strengthening demand for workers persists.

Tightening cycles are no trifling matter. More often than not, the Fed overtightens into recession, fearful of the danger of an overheating economy. Still, employment lags all other economic data. Fed officials would be best served tracking as much real-time data as possible and checking their inclination to seasonally adjust their thinking at the door.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Danielle DiMartino Booth, a former adviser to the president of the Dallas Fed, is the author of "Fed Up: An Insider's Take on Why the Federal Reserve Is Bad for America," and founder of Money Strong LLC.

To contact the editor responsible for this story: Max Berley at mberley@bloomberg.net.

For more columns from Bloomberg View, visit http://www.bloomberg.com/view.

©2018 Bloomberg L.P.