Separating the Renault-Nissan Twins Would Be Bloody

Ghosn, who was detained, was indispensable to the collective functioning of Nissan’s alliance with Renault, Mitsubishi Motors.

(Bloomberg Opinion) -- If you depose a king, you’d best have a plan for what to do in the aftermath.

That’s the challenge confronting Nissan Motor Co. CEO Hiroto Saikawa after the remarkable palace coup in which Chairman Carlos Ghosn was dethroned after almost two decades bestriding the global auto industry.

The man who’s widely seen as indispensable to the collective functioning of Nissan’s alliance with Renault SA and Mitsubishi Motors Corp. has been detained on suspicion of breaching Japan’s financial laws. Meanwhile, Renault’s lead independent directors have pointedly stopped short of backing Saikawa’s move. Given all that, returning to the status quo doesn’t look like an option. But it’s not clear that there’s any viable path forward, either.

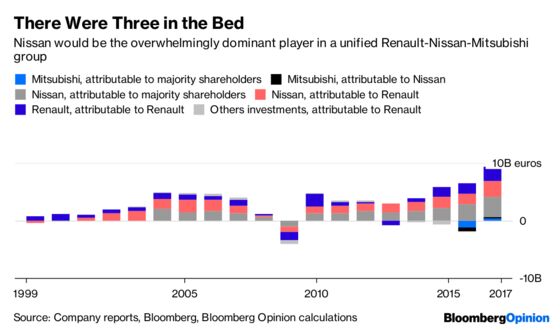

The central problem is that Nissan’s superior earnings and volumes should put it in the driving seat of the alliance — but the setup of the cross-shareholdings binding the companies together means that Renault, and ultimately the French government, won’t let go of the keys.

One option that would no doubt be favored by President Emmanuel Macron, whose approval rating has fallen to just 25 percent, would be a merger of the group that entrenches French leadership. That would secure the position of the world’s biggest carmaker as a national champion and guarantee the security of Renault’s French workforce, who produce about half as much cash flow per head as Nissan’s Japanese employees.

Still, that looks to be definitively off the table for the moment. Ghosn had made setting up some sort of merger his legacy project as he approached retirement age, but even that seemed to have raised hackles back in Japan. If his tentative moves toward a deeper alliance resulted in his own decapitation, it’s hard to see how a more aggressive policy with the backing of the Elysee Palace would do any better.

Another option would be for Nissan to take control of the alliance instead. As a first move by Saikawa toward that end, taking out Ghosn would look like a canny (if brutal) first step. Renault has fallen so far in value that even before its shares slumped 8.4 percent on Monday, Nissan and Mitsubishi would on paper have been able to buy out its shareholders (with the exception of the French state) just using their net cash holdings.

The problem with that option is a thicket of legal hurdles. The French government’s 15 percent stake has double that proportion of votes, thanks to rules granting this benefit to European shareholders who’ve been holders for more than two years. While in theory a generous takeover offer could allow Nissan to go over Macron’s head and appeal directly to similarly endowed European institutional shareholders, it’s hard to believe that the Elysee wouldn’t find further ways to frustrate such an outcome.

That leaves one other option: a dissolution of the group.

It’s probably easiest to see a route to this result. If Nissan bought an additional 10 percent stake in Renault on the market, its holding would rise to 25 percent — a level at which, under Japanese law, the French company would lose its voting rights in Nissan. Were that to happen, Nissan would be able to convene, and prevail in, an extraordinary shareholder meeting to remove Renault directors from its board. Then it could start dissolving the web of joint purchasing and car-platform agreements that hold the alliance together.

Again, though, that seems a strange way to act. For one thing, the costly challenges of electric cars and autonomous vehicles — not to mention the general weakness in the automotive market in 2018 — mean that carmakers should be looking to spread their capex and R&D expenses as widely as possible these days, rather than separating themselves from willing partners.

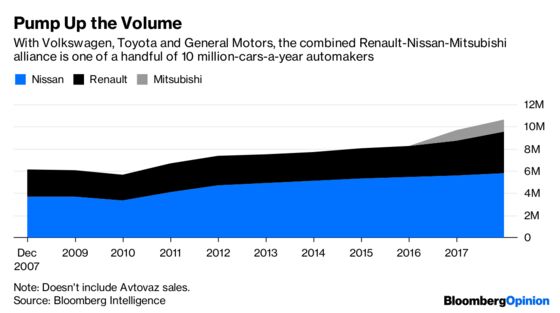

For another, while Ghosn himself is often seen as the linchpin holding the group together, in truth the links run much deeper than that. Alliance cars are now being shifted onto a common modular architecture that leaves them functionally almost identical beneath their badges. Both Renault and Nissan cars are turned out on alliance production lines in India, Russia, Brazil and China. Three out of four power trains are shared by the companies. Synergies across the group will amount to about 5.5 billion euros ($6.3 billion) this year, the alliance says.

And it’s not just about Renault and Nissan. Mitsubishi Motors is bound to the alliance via Nissan’s 34 percent stake, as is Avtovaz PJSC, maker of Russia’s Lada brand, thanks to a Renault holding. Nissan has a joint venture with Dongfeng Motor Group Co. to manufacture its cars and a few Renault models in China. There’s also a smaller equity alliance with Daimler AG encompassing joint development of electric vehicles, engines and power trains. A break would be anything but clean.

Ghosn’s ignominious downfall has perhaps fatally injured the relationship between Renault and Nissan, but it’s hard to see a better option for those involved than trying to somehow piece things back together. For all the bad blood, the two sides have over the years become deeply conjoined. If they end up being separated too aggressively, the hemorrhage could be hard to stanch.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.