Saudi Arabia’s Oil Ministry Gets The Royal Treatment

Al-Falih’s sudden opportunity to spend more time with his family may reflect displeasure with where oil prices are.

(Bloomberg Opinion) -- It seems to me that Khalid Al-Falih, just ousted as Saudi Arabia’s Energy Minister, is better off out of it. Imagine waking every morning wondering how you’re going to spend that day appeasing two masters. One of them, a capricious force capable of fueling instability in the Middle East. The other, the oil market.

Having recently been stripped of his industry and mining portfolios as well as the chairmanship of Saudi Arabian Oil Co. – known as Saudi Aramco – Al-Falih’s latest demotion is more of a coda than a coup. This being Saudi Arabia, especially under the current rule of the King and his son Crown Prince Mohammed bin Salman, there is naturally the whiff of intrigue. A more straightforward explanation is that the oil crash and long-delayed initial public offering of Aramco have claimed another scalp.

Aramco’s new chairman is Yasir Al-Rumayyan, a board member running the sovereign wealth fund that is due to receive the world’s biggest ever round of seed funding from the IPO. He is also a close adviser of MBS, as the crown prince is known. Meanwhile, the new energy minister will be Prince Abdulaziz bin Salman, an energy ministry veteran who just happens to also be the half-brother of MBS.

Look, it is a kingdom. Which has been the problem all along. Aramco’s IPO, gargantuan as it might ultimately be, is in itself an expression of the realization that, as economic models go, a patronage system funded by oil rents looks so 20th century. Ali Al-Naimi, Al-Falih’s predecessor as energy minister, was in the job for 21 years. Now Saudi Arabia will have switched ministers twice in the space of three, suggesting – to use an unfortunately apt metaphor – the permafrost is melting. Remember, MBS sprung the notion of selling off a sliver of the country’s crown jewel as an integral part of his wider objective of promoting the idea of economic reform. He also threw out a valuation of $2 trillion, which was unfortunate because (a) just don’t do that ahead of an IPO, and (b) it never looked realistic.

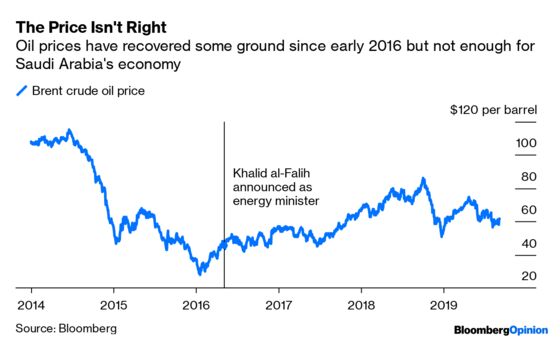

There is speculation Al-Falih’s sudden opportunity to spend more time with his family reflects displeasure with where oil prices are. If true, it reeks of delusion. The fact that oil prices remain anchored around $60 despite rising tension with Iran – with Tehran tweaking things up again this weekend – and OPEC+ showing uncommon restraint on supply speaks to the difficulty Al-Falih, or anyone, faces in trying to push them higher.

On that front, rising bankruptcies and the virtual closure of the equity and high-yield markets to U.S. frackers offers more hope to Saudi Arabia’s committed oil bulls. And yet Saudi Arabia’s very efforts to support prices work against this trend, and don’t help with faltering demand growth either. Equally, though, Al-Naimi’s earlier strategy of trying to crush shale with low prices proved too painful for his country and, perhaps more importantly, his bosses.

As it is, unless oil prices rise closer to $100 a barrel and are expected to stay there, the world’s money managers aren’t going to price Aramco anywhere near $2 trillion (see my back-of-the-envelope scribblings here). And while $100 a barrel forever represents utopia for Saudi Arabia and other petro-states, it would constitute economic dystopia everywhere else – which renders it pure fantasy.

It is, therefore, hard to see what Al-Falih’s replacement could do in terms of oil policy that is vastly different from the current course. Rather, this looks of a piece with MBS’s earlier moves to centralize control.

This has implications for the apparently revived IPO project. Putting close allies and family members into key positions at Aramco and the energy ministry suggests we have entered the phase where MBS just wants this thing done, no questions. In doing so, however, it throws the spotlight once again on Aramco’s duality. Separating the ministry from the chairmanship of the company was pretty standard in terms of trying to bolster Aramco’s commercial identity, albeit undercut by the identity of the replacement. Now the ascendancy of a royal to the energy ministry, breaking with past tradition, reinforces the sense that the wider reform project looks a lot like an old-fashioned exercise in consolidating power.

All else equal, this should raise the risk premium attached to Aramco, which, as I wrote here, rivals oil prices as the biggest determinant of valuation. While Tokyo has now apparently moved ahead in planning for an international listing, a domestic listing may offer a way of saving face somewhat. Even if it skews the country’s roughly $500 billion stock market, MBS could at least count on local banks and the wealthy to buy some small part of Aramco at a favorable price level and not sell. This IPO should have been the capstone on Saudi Arabia’s reform program. Right now, it looks like the kingdom is sticking with what it knows best.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.