(Bloomberg Opinion) -- Stocks rallied Wednesday, with the S&P 500 Index rising 0.54 percent and the MSCI All-Country World Index logging its biggest intraday gain since June as it climbed as much as 1.90 percent. The moves sparked talk that the much-anticipated “Santa Claus Rally” may have finally arrived after a rough December start for equities. Not to be a Grinch, but to me, the rebound looks less like early Christmas cheer and more like a dead-cat bounce.

What’s concerning about the jump in stocks is that it was all based on vague comments related to the trade war between the U.S. and China. More specifically, President Donald Trump said he’d consider intervening in U.S. efforts to extradite Huawei Technologies executive Meng Wanzhou if it helped him win a trade deal with China. Then the Wall Street Journal reported that Chinese officials are considering giving foreign companies more access to local markets. That’s a lot of considering to build a rally upon, especially when Wall Street analysts are busy downgrading their profit estimates. They have trimmed their forecasts for S&P 500 profits in the fourth quarter to $41.58 a share from $42.66 two months ago, according to Bloomberg News’s Lu Wang and Vildana Hajric. The 2.5 percent reduction is the most at this point in a quarter since early 2017, data compiled by Bloomberg show. While the reduction isn’t all that huge, it’s something new for investors, who have enjoyed mostly upward estimate revisions ever since Trump was elected president. The other thing is that the bulls have argued stocks are cheap, based on estimated earnings. But if those forecasts are coming down, stocks no longer look all that inexpensive.

The bulls do have history on their side. December has been the S&P 500's best month of the year since 1950, with average gains of 1.61 percent, based on data compiled by Bloomberg. But with the S&P 500 down about 3.95 percent for the month even with Wednesday’s rally, the benchmark would have to rise about another 154 points, or a further 6 percent, by year-end to match the average “Santa Claus Rally.” There are always exceptions to the rule.

A BROAD CURVE INVERSION SIGHTED

Last week, a very narrow part of the U.S. Treasury yield curve inverted, with yields on five-year notes falling below those of three-year notes for the first time since 2007. That led to a lot of worrying that the more widely watched difference between two- and 10-year Treasury yields, which was at 13 basis points Wednesday, would soon go negative. This is important because an inverted yield curve has historically preceded a recession. But FTN Financial interest-rate strategist Jim Vogel has found that the curve has, in fact, already inverted if you take inflation into account. By his calculations, real 10-year yields are some 20 basis points below real two-year yields. As for whether this means a recession is on the horizon, Vogel wrote in a research note that “unfortunately, the real yield curve offers little reliable history from previous cycles. But it remains essential to today’s landscape because it represents the best single picture of the economic cost of debt.” In other words, longer-term debt is cheap relative to shorter-term debt, which should provide a boost to companies needing to raise financing.

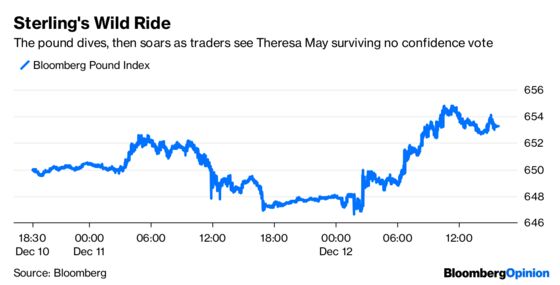

MARKET BACKS U.K.’S MAY

The pound has taken a beating under U.K. Prime Minister Theresa May and her efforts to extricate the country from the European Union. The Bloomberg Pound Index is down about 4 percent for the year and is really no stronger against its major peers than it was in the aftermath of the June 2016 Brexit referendum that caused sterling to plummet. And yet, currency traders seem to think that she’s the U.K.’s best option despite her inability to get the support for her plan to leave the EU. That can be seen in the sterling’s performance over the last 24 hours. Sterling tanked after reports emerged late Tuesday that May faced a vote of confidence in her leadership of the Conservative Party. But then the Bloomberg Pound Index recovered Wednesday, rising as much as 1.17 percent in its biggest gain since Nov. 1 on reports May had enough support to survive a confidence vote. And indeed, she did survive, with Tory members of Parliament backing her by 200 to 117 in the secret ballot.

EM BENEFITS FROM FEAR, NOT GREED

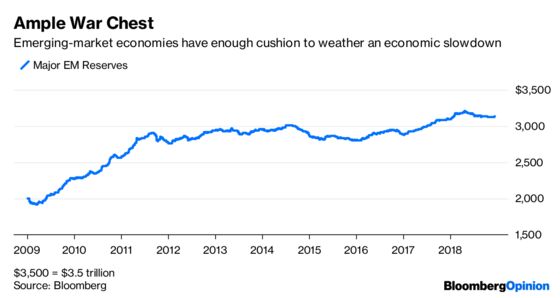

Just like in the U.S., emerging–market investors seem to be ignoring the fundamentals. The MSCI EM Index of equities rallied Wednesday to bring its gain to 4.72 since touching its low for the year on Oct. 29. By contrast, the broader MSCI All-Country World Index is up just 0.75 percent in the same period. Emerging-market stocks are in demand despite a report from the Institute of International Finance showing that its real-time measure of economic growth in these areas has dipped below 4 percent for the first time since May 2016. Perhaps the almost 27 percent drop in the MSCI EM Index between late January and late October has already discounted slower growth. If that’s the case, than the recent rebound in emerging markets could be due to the fact that they are heading into 2019 with what Citigroup calls a high level of “financial resilience” despite lacking any “growth resilience.” Foreign-exchange reserves for the 12 largest emerging-market economies excluding China stand at $3.13 trillion, up from less than $2 trillion in 2009, data compiled by Bloomberg show. “The asset class is much better placed to weather negative shocks to risk appetite than it was earlier this year: external financing gaps have closed, interest rates have risen, currencies are cheaper and EM is broadly speaking an ‘under-owned’ asset class,” Citigroup’s strategists wrote in a report Wednesday.

SOYBEANS ARE MAKING A COMEBACK

The price of soybeans took a big hit earlier this year as the trade war between the U.S. and China escalated. In retaliation for tariffs put on Chinese goods by the U.S., China imposed tariffs on soybeans, which are a top U.S. agricultural export to China. As a result, soybean prices tumbled 24.5 percent between early March and mid-September. But now, the market is making a comeback, with prices rising on Wednesday to their highest since June. Traders are optimistic that a meeting between President Trump and China’s Xi Jinping has led to some tamping down of the trade tensions. In fact, China is making its first sizable purchase of U.S. soybeans since the two countries began their series of tit-for-tat tariffs, according to Bloomberg News’s Alfred Canga, citing a person with direct knowledge of the transaction. Reuters reported earlier Wednesday that Chinese state-run firms bought at least 500,000 tons of U.S. Some commodities traders aren’t impressed. “500,000 doesn’t cut the mustard,” Jim R. Gerlach, president of A/C Trading in Fowler, Indiana, told Bloomberg News. “You’re going to have to see millions of tons, not a half million here and a half million there.” U.S. farmers have been harvesting a record soybean crop over the last few months and inventories are set to surge in the year ahead amid the lack of demand from China.

TEA LEAVES

European Central Bank policy makers meet Thursday, and it promises to be one for the history books. Despite slower economic growth in the region, waning consumer and business confidence, and tepid inflation, the ECB is likely to say that now is a good time to end its asset purchases. If that seems to you like a head scratcher, you’re not alone. But the thinking, at least among the pessimists, is that by stopping asset purchases now after spending a total of $2.6 trillion euros ($3 trillion), the ECB can at least resume the program when the economy worsens and hopefully have some impact. ECB officials have largely downplayed the slowdown, blaming it on temporary issues (such as German car production) and predicting a rebound this quarter. While acknowledging the threats, they’ve stuck to their line even as some numbers suggest the bounce back may not be much to cheer about, according to Bloomberg News’s Fergal O'Brien.

DON’T MISS

Negative Yields Create Case of Bond Trader FOMO: Brian Chappatta

Markets Conclude U.S. Is Riskier Than China: Matthew A. Winkler

Index-Investing Critic Takes Aim, Fires, Misses: Barry Ritholtz

India’s Central Bank Woes Won’t End With New Leader: Daniel Moss

Matt Levine's Money Stuff: Unicorns Leave the Enchanted Forest

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.