Ray Dalio's Risk Parity Trade Is Alive and Well in China

Risk parity trades, made popular by Ray Dalio, have made a nice comeback since the global selloff in March.

(Bloomberg Opinion) -- Risk parity trades, made popular by Bridgewater Associates LP founder Ray Dalio, have made a nice comeback since the global selloff in March. In its simplest form, this strategy assumes that government bonds rally when stocks fall — a dynamic Covid-19 turned on its head when everything was crashing at once.

Now both asset classes are behaving again, and the S&P Risk Parity Index that targets 15% market volatility has returned over 45%. But for the next leg up, hedge funds should consider paying a visit to China.

Risk parity strategies became very popular over the past decade. It’s intuitive, really: In a zero inflation world, long-term bond yields reflect traders’ bets on the broader economy; so when yields rise, it means the outlook is brightening, which is great news for stocks. As a result, these funds often hedge equity risk by owning government bonds on leverage, hoping that a diversified portfolio will weather most storms.

Will this trade continue to shine? March gave us some pause, but even if the negative correlation continues to hold, it becomes harder to execute if (gasp) the Federal Reserve embraces yield curve control. Then government bond yields will be like an Italian soccer player’s stylish hair — immovable.

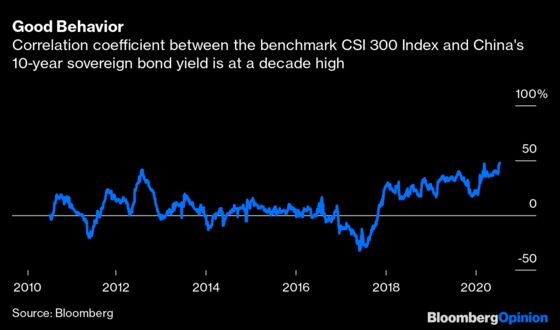

This is where China comes in. In the last three months, the correlation between the benchmark CSI 300 Index and the 10-year government bond yield was at its highest in at least a decade. A surprise rally in stocks met a bearish turn in bonds. More importantly, unlike the U.S., sovereign yields are well above zero, and the People’s Bank of China intends to keep it that way.

But there’s always a twist in China. Unlike the U.S., a rise in government bond yields may not mean a rosier economic outlook. Rather, interest rates are bid up amid a flood of fresh supply.

To help local governments raise cash, Beijing has significantly expanded the municipal bond issuance quota. In the first half of the year, various levels of the government issued a net 3.8 trillion yuan ($543.7 billion), up 54% from a year earlier. This, along with the PBOC’s recent moves to step back from open-market operations, has pressured the bond market.

A busy municipal bond issuance schedule, in turn, is a boost to stocks. This has become particularly relevant for the technology sector. Proceeds have effectively become stimulus checks — in the form of subsidies or even capital injections — waiting to be deployed for China’s tech infrastructure build-out. For cues on whether this equity rally has steam, stock traders just need to look at local governments’ debt raising plans.

Capital from abroad flowed into Chinese government bonds in the second quarter at the fastest pace since late 2018. But yield is only part of the lure. Now that the mainland stock market is staging a surprise rally, bonds can serve as a good hedge should foreigners decide to join the equity party. Of course, since China's economy is still emerging, figuring out the proper market beta to achieve risk parity is more art than science. Nonetheless, this is where risk arbitrage funds can potentially extract long-term value.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2020 Bloomberg L.P.