Putin Erases the Truth About the Ruble

(Bloomberg Opinion) -- On Tuesday, Russian President Vladimir Putin quietly signed an arcane bill that will alter the appearance of many of the country’s streets and erase one of the few remaining symbols of the economic freedom the country discovered when the Soviet Union fell apart.

The new law prohibits currency-exchange offices from displaying rates to passersby. That may not sound important, unless you know the role of the signs in Russia’s modern history.

In 1937, Josef Stalin established a full state monopoly on currency operations in the Soviet Union. That meant the government set exchange rates that had nothing to do with the ruble’s market value. Exchanging currency at (black) market rates was a crime. It was only on Nov. 15, 1991, a little more than a month before the Soviet Union was gone, that the prohibition was lifted, as President Boris Yeltsin legalized all exchange operations and set off a forex mania.

From that moment, anyone could open a currency-exchange office, and people did — in rented apartments, in buses, in the corners of stores. Most had street signs, and once prices were freed in 1992, these became indicators of the path of the hyperinflation that raged for the next three years. The dollar became Russians’ preferred currency; in the mid-1990s, net imports of U.S. cash exceeded $30 billion a year. The exchange offices were doing brisk business: People who had lost their savings when the Soviet Union collapsed only trusted the dollar under the mattress as a store of value.

Then, in 1998, the exchange signs started changing several times a day again, as Russia defaulted on its domestic debt and stopped supporting its currency. With the internet still in its infancy, the signs were the most useful mass media: Russians didn’t have to wait for the next morning’s paper to know it was time to run and buy something, anything, with any remaining rubles.

In the years that followed, the exchange-office signs showed a more stable ruble, reflecting a return of trust in the national currency. The currency looked more reliable as oil prices rose in the 2000s; in 2006, the parliament banned businesses from linking their prices to the dollar. But the exchange-office signs were by now a habit and a news source for those who didn’t follow current events closely. If the forex rate was shifting, something was up.

In 2014, as the ruble crashed along with oil prices, everybody was watching the signs again. If you couldn’t see one from your window, you could meditate to a special, laconic website called “Russian Zen” that displays the exchange rates of major currencies and the oil price against changing new age backgrounds.

Perhaps the exchange signs were destined to go the way of printed newspapers. But there are other reasons for the government to get rid of them now.

Officially, the Central Bank of Russia, which is behind the new legislation, wants to hurt the country’s many illegal exchange offices, which are not part of licensed banks. Central bank officials have argued that these fly-by-night operations can only exist because they advertise on the street. But the ban will include banks, too.

The change may also be driven by the Russian authorities’ recent dollar allergy related to U.S. sanctions and an expectation of even tougher restrictions. Even though officials say Russia isn’t preparing for a ban on dollars or the U.S. financial system, the central bank has been shifting reserves to gold, euros and the renminbi and cutting or shifting offshore its investments in U.S. debt.

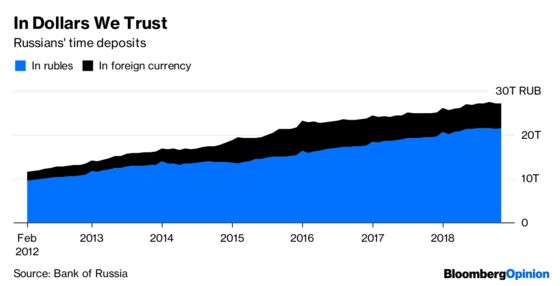

It makes sense to prepare people for a possible conversion of dollar deposits, about 27 percent of the total, if tougher sanctions hit. It also may be prudent to put the surging dollar out of sight of Russians who keep their deposits in rubles and are paid in the currency.

The so-called Donetsk People’s Republic, supported by Russia in eastern Ukraine, banned the signs in June and offers a lesson in the perils of such a move. When the ruble drops — it’s one of the worst-performing currencies, having lost 12.86 percent against the dollar — the pro-Moscow authorities in the “republic” begin to worry that its people might regret not sticking with Ukraine and its Western backers.

I can easily see how the Kremlin could be thinking along similar lines. Putin has been losing popularity, and the message displayed on the exchange offices can hardly help. “The forex signs are the last independent national media outlet,” Moscow scriptwriter Oleg Kozyrev quipped on Facebook. “It told everyone the truth every day. That’s why it got banned.”

I won’t really miss the ugly signs. But I fear there’s more truth to Kozyrev’s joke than the Kremlin dares to admit, perhaps even to itself.

To contact the editor responsible for this story: Max Berley at mberley@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Leonid Bershidsky is a Bloomberg Opinion columnist covering European politics and business. He was the founding editor of the Russian business daily Vedomosti and founded the opinion website Slon.ru.

©2018 Bloomberg L.P.