Powell Embraces the Walkback to the Market's Delight

.jpg?auto=format%2Ccompress&w=200)

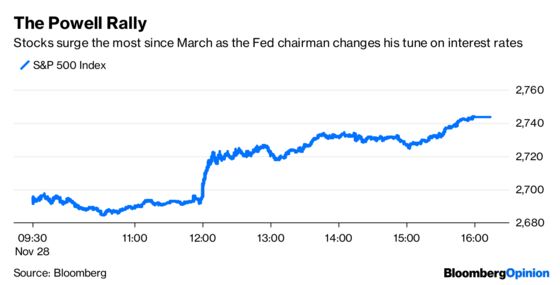

(Bloomberg Opinion) -- Federal Reserve Chairman Jerome Powell is not afraid to admit his mistakes. That was the big takeaway from his speech on Wednesday, when he sent stocks flying higher by saying interest rates are “just below” neutral, or a level that neither stimulates nor restrains growth. Contrast that with his remarks on Oct. 3, when he said that rates were probably “a long way from neutral.”

Sure, plenty of cynics say that Wednesday was the day the “Powell Put” was born or that he caved to criticism from President Donald Trump. But the real reason the S&P 500 Index rallied 2.30 percent in the biggest gain since March is that Powell is showing that as a “markets guy” he’s probably more pragmatic in ways that his predecessors — Janet Yellen and Ben S. Bernanke, who hailed from the world of academia and were devoted to economic models — were not. It’s not just that the S&P 500 had dropped as much as 10 percent on a closing basis since Powell’s comments on Oct. 3, but some pretty significant parts of the economy have been sending distressing signals of late. For example, just a few hours before Powell spoke, the government said sales of new U.S. homes fell in October to the weakest pace since March 2016 as rising borrowing costs and elevated prices keep buyers out of the market. The holiday shopping season has gotten off to a mixed start, which is surprising given that the unemployment rate is the lowest since 1970. Inflation has slowed. And then there’s the intensifying trade war between the U.S. and China. “We have had a good stretch of solid growth by historical standards, but now we are facing a period where significant risks are materializing and darker clouds are looming,” International Monetary Fund Managing Director Christine Lagarde wrote in a blog post Wednesday, referring to the global economy.

“This is very significant because the narrative that Powell was going to hike us into a recession is not nearly as much as a risk as people perceived it to be in early October,” Michael Purves, the chief global strategist at Weeden & Co., told Bloomberg News’s Sarah Ponczek. “I don’t really subscribe to the Powell Put. The market is not down 25 percent. But I would suggest that Powell is reacting to the data. He simply does not have to fight a potential inflation breakout the way some might have thought.”

BOND TRADERS SKIP THE PROTECTION

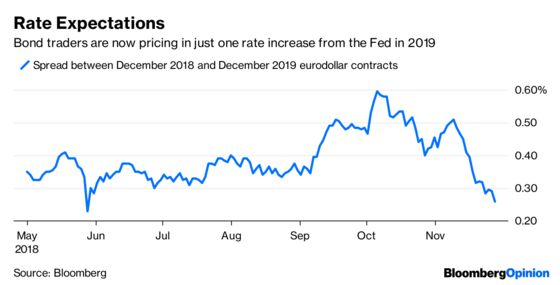

The other way to look at the comments from Powell, who took over as Fed chairman in February, is that he was just correcting a “rookie mistake.” After all, at 2 percent to 2.25 percent, the Fed’s target for the federal funds rate hasn’t changed since he made the “long way from neutral” speech. But that still leaves the question of precisely what the neutral rate is. Most believe it to be around 3 percent, and if the Fed does as widely expected and raise rates again next month to a range of 2.25 percent to 2.50 percent, then it would, by definition, be “just below” neutral. That’s perhaps why the bond market swiftly priced in just one rate hike for 2019. That’s seen in the spread between December 2018 and December 2019 eurodollar futures, which briefly touched less than 25 basis points, the equivalent of one Fed hike. That’s the lowest in six months and less than half the gap from mid-October, according to Bloomberg News’s Alexandra Harris. Even before Powell spoke, bond traders seemed to be betting on a dovish tilt. The Treasury Department’s sale of $18 billion in two-year notes with rates that rise with benchmark rates drew bids of just 2.62 times the amount offered. That’s the lowest bid-to-cover ratio since the government introduced two-year floating-rate notes in 2014. It seems there’s less demand for bonds that protect against rising rates.

POWELL CORRALS THE DOLLAR BULLS

Not everyone was happy with Powell’s comments, namely dollar bulls. The Bloomberg Dollar Spot Index, which measures the greenback against its chief peers, fell as much as 0.69 percent in its biggest decline since the start of the month. Theoretically, the prospect of fewer rate hikes by the Fed may make dollar-denominated assets less attractive on a yield basis than the alternatives. “The Fed has paid lip service to data dependence in the last few years, but data dependence has now arrived,” Alan Ruskin, global co-head of foreign-exchange research at Deutsche Bank AG, told Bloomberg News. “A dollar forecast will only be as good as the next major U.S. data point.Also in theory, this is good for stocks. The rising dollar has been blamed for contributing to the drop in equities because a stronger currency tends to make exporters less competitive. Jodie Gunzberg, managing director and head of U.S. equities at S&P Dow Jones Indices, wrote in a blog post in May that the S&P 500 rises 3.7 times more from a falling dollar than a rising one. So, all else being equal, a stronger greenback is a serious headwind. That can be seen in the U.S. merchandise-trade deficit, which the government said Wednesday grew to a record $77.2 billion in October as exports declined. The deficit has expanded from $64.7 billion in May. The big winners from the dollar’s decline on Wednesday were the New Zealand dollar, Australian dollar, South African rand and Mexican peso. Each of those currencies appreciated more than 1 percent.

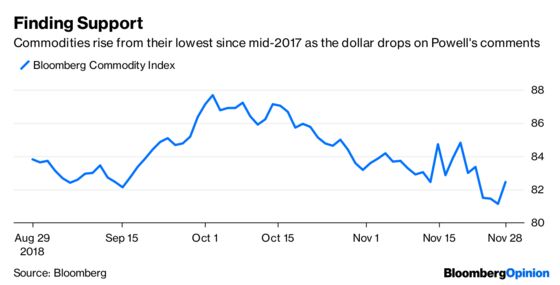

COMMODITIES SURGE, BUT MAYBE NOT FOR LONG

The drop in the dollar gave a boost to the market for raw materials, with the Bloomberg Commodity Index rising as much as 2 percent from its lowest level since mid-2017. Commodities are largely traded in dollars, so a lower greenback tends to make them more affordable. Some of the biggest gainers were palladium, which rose to another record, copper, soybeans, sugar and corn. Energy-related commodities were notable losers, with oil falling as much as 2.91 percent to extend its bear market. Oil traders looked past the Fed to a U.S. inventory report that showed a 10th consecutive rise in crude stockpiles, adding to concerns about a global glut. The Energy Information Administration reported nationwide crude stockpiles climbed by 3.58 million barrels last week to the highest in a year as imports rose, according to Bloomberg News’s Alex Nussbaum. Still, it’s unlikely a falling dollar will have a lasting impact on commodities demand. Of more importance is the global economy, which is slowing and is largely responsible for the Bloomberg Commodity Index’s 11.4 percent drop since it’s the year in late May through Tuesday. In addition to warning that global growth may be slowing more than forecast, the IMF’s Lagarde also urged countries to cut spending where possible so they have more room to respond if the economy weakens further. Central banks should take a “gradual, well-communicated, and data-dependent path” toward higher interest rates, she wrote in the blog post.

POWELL JUICES THE EMERGING-MARKET RENAISSANCE

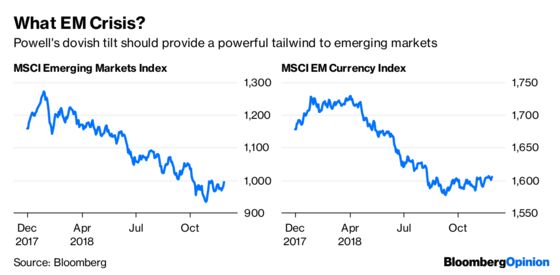

Remember how just a few months ago everyone was talking about a looming crisis in emerging markets given the big drop in their equities and currencies? You don’t here that much anymore, thanks to a quiet rebound that may only get stronger after Powell’s dovish tilt. The MSCI Emerging Market Index of equities jumped as much as 1.47 percent, bringing its gain to 6.31 percent since late October. The MSCI EM Currency Index rose as much as 0.35 percent, bringing its gain to 1.77 percent since bottoming out for the year in September. In many ways, talk of a crisis in emerging markets stemming from a rising dollar was always largely overblown, mainly because they are in a much better fiscal situation than ever. Foreign-exchange reserves for the 12 largest emerging-market economies excluding China stand at $3.13 trillion, rising from less than $2 trillion in 2009, data compiled by Bloomberg show. Whether the rally in emerging markets can continue may depend largely on this week’s meeting between Trump and President Xi Jinping of China at the Group of 20 summit in Argentina at the end of the week. “Any hint of cooperation between the U.S. and China towards stemming the tit-for-tat tariff escalation would be a major boost for market sentiment going into year-end,” Paul Greer, a money manager at Fidelity International in London, told Bloomberg News. “We’d likely see a weaker dollar, EM currency appreciation, tighter emerging-market credit spreads and lower risk premium on local bonds.”

TEA LEAVES

Powell’s comments basically made clear that the Fed will be “data dependent” when it comes to future rate increases. Well, market participants will get their first big look at how consumers reacted to the market turmoil that started early last month when the government on Thursday releases its data on consumer spending for October. The median estimate of economists surveyed by Bloomberg News is for an increase of 0.4 percent, the same as in September, which was the lowest since February. Real personal spending, which is what actual expenditures are after accounting for inflation, is seen rising just 0.2 percent, which would also be the lowest since February.

DON’T MISS

New U.S. Yield Curve Is Racing Toward Inversion: Brian Chappatta

Why the Bull Market's More Fragile Than It Looks: Stephen Gandel

Why Valuations Don’t Matter Much in Emerging Markets: Shuli Ren

A Strange Expansion Might Set Up a Mundane Recession: Noah Smith

Pimco Extracts Its Pound of Flesh From Italy: Marcus Ashworth

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.