PizzaExpress Is About to Be Sliced Up

PizzaExpress is headed for a debt restructuring. Expect its senior bondholders to take a big slice of the company.

(Bloomberg Opinion) -- A troubled British consumer brand with an illustrious past. Too much debt. A big Chinese investor. Sound familiar?

PizzaExpress Ltd., which is preparing for debt talks with creditors, is being compared to Thomas Cook Group Plc, the travel operator that collapsed last month. The 54-year-old restaurant chain isn’t in as precarious a state as Thomas Cook was for much of this year. But it needs to learn some lessons from the unhappy fate of the British tour operator.

Owned by the Chinese private equity group Hony Capital, PizzaExpress has been hurt by similar “casual dining” chains opening too many outlets and a consumer slowdown. Some rivals have collapsed, such as Jamie’s Italian, while others have closed stores, like Prezzo.

PizzaExpress has been expanding in China too, which hasn’t paid off. Like-for-like sales outside the U.K. fell 7.5% in the year to Dec. 30 2018, the last accounts available. Its high borrowings are another worry, with total debt of 1.1 billion pounds ($1.3 billion) at the end of 2018. The group made a 55 million-pound loss last year, compared to a pretax profit of 28.7 million pounds in 2017.

Fortunately it isn’t as much a hostage to consumer confidence as Thomas Cook. People booking a meal on a Saturday night won’t worry too much whether the the restaurant will still be there on Monday. When you’re booking a holiday, you want to know the tour operator will still be in business to fly you there and to get you home. That fear added to the death spiral at Thomas Cook.

Nevertheless, PizzaExpress is headed for a debt restructuring, which will probably be tortuous. It had 47.9 million pounds of cash on its balance sheet at the end of 2018, and made cash from operating activities of 33.3 million pounds that year. It doesn’t face an immediate liquidity crunch.

Yet its revolving bank credit facility is maturing in August 2020, and its bonds are falling due from August 2021, so it needs to make sure it has adequate future financing in place. If Thomas Cook is any guide, it better sort this out sooner rather than later.

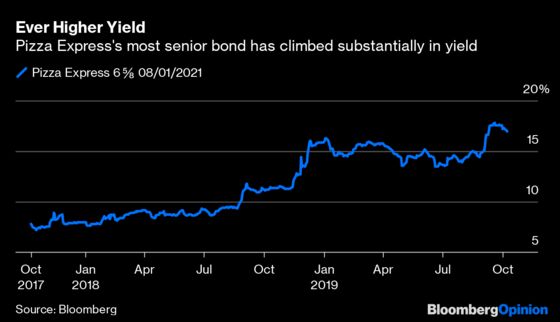

There are several parts to PizzaExpress’s debt, which will suffer different fates. Alongside a 500 million-pound loan from Hony, there are two outstanding public bonds totaling 665 million pounds ($812 million) which mature in two and three years’ time. They will probably be restructured if the group is to survive.

The power resides with the holders of the most senior 465 million-pound bond, due in August 2021. That still trades relatively close to full value at 85 pence in the pound. These investors will have significant clout in this restructuring negotiation, and it’s no surprise that they’ve formed a committee to represent their interests. One possible outcome is that they swap their debt for a majority stake in the British PizzaExpress business.

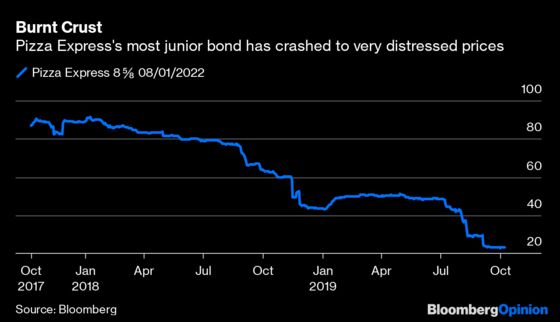

The more junior bond due in 2022 will be second in the queue and its holders won’t be looking forward to much recompense. But that is reflected in the bond’s knockdown price of about 20 pence in the pound.

Even if bondholders do take control of the U.K. business — as Debenhams’ debt investors did in April and Thomas Cook’s lenders and note-holders tried to do recently — PizzaExpress’s difficulties won’t be over. Supply and demand in the casual restaurant sector is starting to match up again, given all the recent closures. But Brexit uncertainty is weighing on consumers, as weak September retail sales demonstrated.

At least PizzaExpress has a chance to sort out its dough before things become terminal.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.