Debt Market Gives Payday Lender a Taste of Its Own Medicine

CNG Holdings plans to sell $310 million of bonds, promising a 12% interest rate to investors who can stomach its business model.

(Bloomberg Opinion) -- “The consensus choice for the payday chain that exhibited the least scruples.”

That’s how Gary Rivlin, who spent years exploring the fringes of subprime lending and wrote the book “Broke, USA: From Pawnshops to Poverty, Inc .— How the Working Poor Became Big Business,” described Check ’n Go in a 2011 article for The Daily Beast. Check ’n Go is one of two payday loan brands run by Cincinnati, Ohio-based CNG Holdings Inc., which has 951 outlets in 26 states. Customers with weak credit scores often use payday lenders to obtain short-term loans at high interest rates.

Now CNG is hoping to raise some cash in the corporate-bond market with a similar approach.

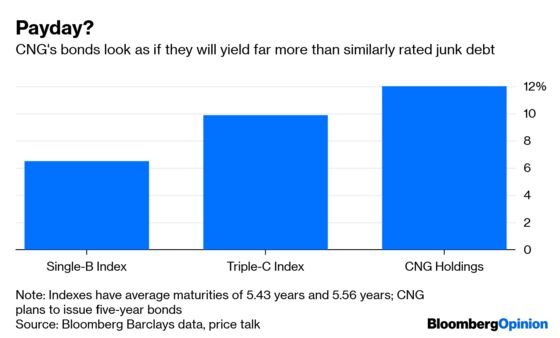

The company plans to issue $310 million of five-year securities this week, with investors being told to expect a whopping 12% coupon, Bloomberg News’s Molly Smith reported. And even at such a lofty interest rate, the bonds might still price at a discount, meaning the overall yield will be even higher. Only two U.S. deals in 2019 have offered a higher payout, data compiled by Bloomberg show. One was from Affinion Group Holdings Inc., which conducted a distressed exchange, and the other was from Egalet Corp., which issued the securities amid a restructuring.

That’s not exactly a flattering peer group for a company that was just upgraded to B by S&P Global Ratings. While that’s still considered junk, it doesn’t suggest any sort of default is imminent. In fact, the proceeds of the coming sale would be used to refinance debt that’s otherwise due in 2020, effectively pushing out maturities, which credit raters view favorably. On top of that, the Trump administration has taken steps to weaken the Consumer Financial Protection Bureau, the chief regulator of the payday lending industry. That should be a boon to a company like CNG.

What, then, explains the outsized yield being tossed around to entice investors? It might be a simple case of people just not liking the idea of lending their money to a company known for being a payday lender.

Type “CNG Financial Corporation” into the CFPB’s consumer complaint database and more than 1,100 entries appear dating back to August 2013. A former Check ’n Go store manager in Washington said that it “deliberately targets black communities,” the Columbus Dispatch reported in 2007, though the company called the statements “false and reckless.” John Oliver went after the practice in a 2014 episode of his HBO show “Last Week Tonight.”

And the aforementioned 2011 article from The Daily Beast? It’s titled “America’s Worst Subprime Lender: Jared Davis vs. Allan Jones?” Davis is president of CNG Financial. Allan Jones is the CEO of Check Into Cash Inc., another payday lender with “only” 417 CFPB complaints.

Of course, much of this coverage is from years ago, and there’s a reason for that. In addition to states toughening up on payday lenders (including Ohio), CNG is also ahead of its peers in diversifying away from that business and into longer-term installment loans, which demand more extensive underwriting (like actually verifying pay stubs or employment confirmation). Just 25% of the company’s net revenue came from payday loans as of the end of 2018, according to analysts at Moody’s Investors Service, though they noted in their May 2 report that an installment loan “still has many features of the payday product.”

As I’ve said before, companies that provide loans to weaker borrowers can serve a important function in some communities. CNG’s website, naturally, states this benevolent view: “At our core, we are a family of brands dedicated to helping people make ends meet — with products and services designed to cover short-term money needs. Each day, we have a unique opportunity to make a difference in people’s lives. We’re committed to doing that in a way that is responsible and within their means.”

That commitment will be put to the test given that the CFPB is on the verge of finalizing a re-proposed rule that would roll back a crucial element: that a lender assess a customer’s ability to pay before extending a loan. According to Bloomberg Intelligence, 67% of potential customers for payday loans wouldn’t meet that requirement, which would cost the industry billions of dollars in revenue. Under the revised proposal, companies could still freely lend to that group.

And yet, even with that favorable stance, CNG is still offering a yield higher than 12%. That may be the bond market’s way of signaling it doesn’t expect the CFPB to be defanged forever. Some expect payday lending to be a flashpoint in the 2020 U.S. presidential election, particularly among Democratic candidates like Senators Elizabeth Warren of Massachusetts and Bernie Sanders of Vermont. Industry lobbying groups will almost certainly mobilize in opposition. As far as pricing risks go, regulatory regime change is a tough one.

CNG is coming to market amid a boom in dodgy deals and with U.S. high-yield bonds returning an impressive 8% so far this year. Investors in junk debt have had few scruples in 2019, and for good reason. CNG is counting on that attitude to win the day.

Moody's measures profitability through net income to average managed assets. It has a single-A "profitability score," according to the May 2 report. Pretty much every other part of the scorecard is decidedly junk, from asset quality to industry risk.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.