(Bloomberg Opinion) -- The Guardian recently reported a startling development — according to the charity Oxfam, a handful of the world’s richest people got much richer in 2018, while half of the world’s population got much poorer. On Twitter, writer Anand Giridharadas summed up the dire implications:

When Giridharadas urges us not to “be Pinkered” into complacency, he’s referring to psychologist Steven Pinker, whose books convey the message that life for large numbers of people has been improving.

By this point, everyone knows — or ought to know — that inequality has been rising within most developed countries. This has been made clear by a steady drumbeat of statistics, as well as economist Thomas Piketty’s landmark 2014 book “Capital in the Twenty-First Century,” which confirmed that inequality has generally increased within rich countries since about the middle of the 20th century. Nor can anyone ignore the glaring disparities between the global ultra-rich, who gathered at Davos, Switzerland, this week to ski and network and praise themselves, and the billions of people in poor countries who still subsist on just a few dollars a day. To anyone who is upset about these disparities, Oxfam’s numbers simply add one more call for alarm.

But the charity organization’s dire reports should be taken with a grain of salt. The truth is that wealth inequality, though substantial, probably isn’t skyrocketing.

First of all, Oxfam’s numbers look dubious. If the wealth of half of the world’s people really fell by 11 percent in one year, as Oxfam says, it would signal the coming of an enormous global recession. But 2018 economic growth numbers look healthy — the International Monetary Fund estimates that almost every economy in the world grew last year, with only a small handful of exceptions. That suggests something funny is going on with Oxfam’s data.

One reason might be that wealth is inherently hard to measure, especially in developing nations. In those countries, much wealth tends to be held in the form of real assets, like houses owned by poor farmers, or informal businesses, like a family-run food stand in a big city. There are typically no well-functioning, transparent financial markets for these assets, so it’s hard to get a reliable estimate of their value.

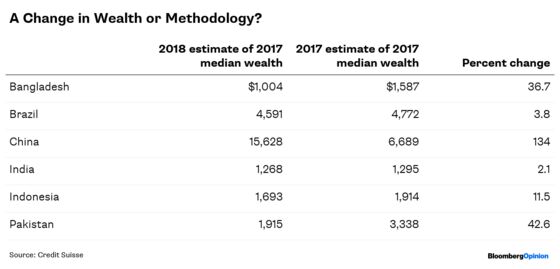

That’s not to say that the global poor have lots of hidden wealth squirreled away. Instead, what it means is that changes in the estimated value of wealth in developing nations are likely to come from changes in the assumptions of the researchers doing the estimation, or changes in data availability. This can be seen in Oxfam’s numbers. Oxfam gets its wealth data from Credit Suisse, which provides yearly updates to its estimates. Comparing the 2017 wealth estimates to the 2018 updated estimates for 2017, we can get an idea of how much these numbers tend can vary:

These differences can’t be coming from actual wealth changes, since both estimates are for 2017; they come from data revisions. As you can see, sometimes these data revisions are small, but other times very large — for China, the difference is more than twofold! Even for rich countries, the data revisions can be big — for Japan, the difference was about 18 percent.

If data revisions are regularly this big, then Oxfam’s assertion that wealth inequality went up substantially in 2018 could easily be illusory.

In rich countries, meanwhile, wealth depends mostly on asset prices, especially the prices of stocks and real estate. As anyone who lived through the 2008 financial crisis keenly remembers, these prices can be affected by investor sentiment that has little to do with the real underlying value of physical assets — and thus little to do with how much of the world’s actual resources people get to consume. If investors decide to pay higher prices for shares of Amazon.com Inc., Jeff Bezos’ wealth goes way up, but the real value of Amazon’s business might be the same as the previous day. For closely held companies, where many rich people derive their wealth, it’s even harder — if one investor overpays for a small piece of Uber Technologies Inc., the whole company’s valuation can go up by billions of dollars, but that really just reflects the excessive optimism of that one investor.

This means that big swings in the wealth of the world’s top billionaires don’t usually represent changes in the amount of real, physical resources they command — it doesn’t show that they are “monopolizing progress,” as Giridharas puts it, to any greater degree than before.

Wealth comparisons are always hard to do, but they’re even harder when comparing across countries. Big swings in exchange rates can dramatically change the amount of real foreign resources — Nigerian oil or Australian bauxite — that Jeff Bezos’s billions would be able to buy.

Finally, as many other writers have noted, wealth calculations include debt, much of which is held by people in rich countries who actually aren’t that poor. By the official definition, when Donald Trump declared bankruptcy, he was poorer than a debt-free subsistence farmer in Somalia. Thus, reported shifts in the wealth of the world’s so-called poorest people can reflect changes in debt rather than swings in the real-asset holdings of the actually destitute.

So although it’s good to be concerned with wealth inequality, reports such as Oxfam’s shouldn’t be cause for alarm. The world is a very unequal place, but 2018 probably didn’t make it much worse in any meaningful sense. The real story of 2018 was a positive one — rapid global growth that raised living standards in poor countries such as Ethiopia, India, Bangladesh and Indonesia. Thanks to that growth, global inequality of income — which can be measured more reliably than wealth — is actually falling.

So yes, the vast wealth of the Davos set may be annoying, and countries such as the U.S. and China should tax them more. But ultimately, the fate of the world’s poor will depend much, much more on economic growth than on how much rich countries choose to tax their wealthiest citizens.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2019 Bloomberg L.P.