Nomura Could Use a Fresh Twist on an Old Story

CEO Koji Nagai’s cost cuts and tightened focus on fixed-income trading for institutional clients are producing results.

(Bloomberg Opinion) -- After stumbling badly for two years, Nomura Holdings Inc. has finally regained its footing. But can the Japanese bank succeed in the race to capture market share in China and avoid tripping over a demographic hurdle at home?

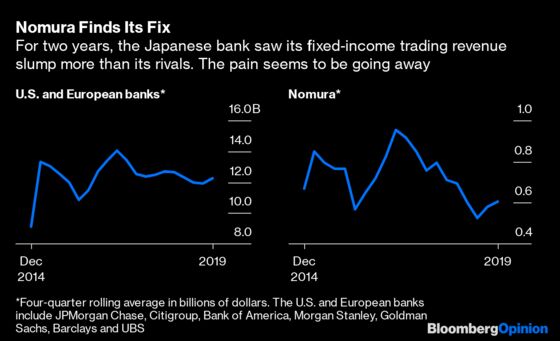

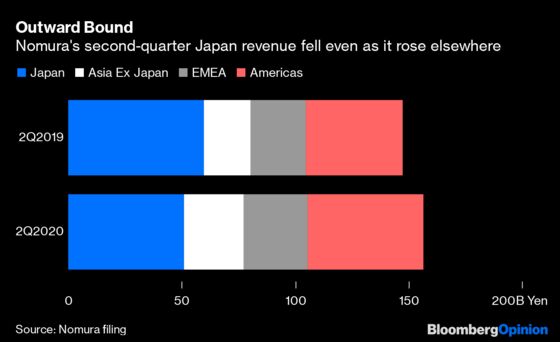

CEO Koji Nagai's cost cuts and tightened focus on fixed-income trading for institutional clients are producing results. On Tuesday, Nomura posted pretax income of 128.5 billion yen ($1.2 billion), bumped up by a 73 billion yen gain on the sale of a stake in a research affiliate. The wholesale banking business, while slightly weaker than in the June quarter, nevertheless garnered four times as much in income as a year earlier. Out of the four regions in which Nomura operates, net revenue fell from a year earlier only in Japan, cementing a recovery that got under way three months ago with the investment bank’s first overseas profit in six quarters.

Headcount has shrunk to 27,630 from 28,549 in September last year. Pruning employees and trimming product lines can only go so far, though. Investment-banking revenue is flat, while revenue and income from the retail brokerage business are both shrinking. Nagai needs a new growth engine to insulate earnings from whimsical investor sentiment in the fixed-income market.

China could be that locomotive. In 2017, Beijing announced plans to lift restrictions on foreigners participating in financial services businesses — from investment banking to wealth and asset management. Nomura received approval to control a securities business in China in March, joining JPMorgan Chase & Co. and UBS Group AG in having that privilege.

Nomura's more immediate goal is to develop a wealth management and institutional brokerage business in China, people familiar with the matter told Bloomberg News last month. Its local venture, along with Shanghai-based minority partner Orient International (Holding) Co., will focus on clients with a minimum of 3 million yuan ($425,000) of investable funds.

The allure of China is understandable: The country now has almost 4.5 million adults with wealth in excess of $1 million. That’s 1.5 times Japan’s millionaire population, according to Credit Suisse Group AG. At the same time, persuading China’s rich to park their money with a Japanese bank won’t be a cakewalk.

Where Nomura can compete against global heavyweights like UBS as well as strong local rivals such as China Merchants Bank Co. is in targeting the country’s internet entrepreneurs. A wealth management relationship with a startup boss can often mean the chance to lead a financing round, especially in a market that’s seen venture-capital financing drop by more than three-fifths this year. Besides, being a banker to Masayoshi Son’s SoftBank Group Corp. can also help open doors.

Gaining the China license won’t be an instant fix. The franchise will take years to be fully up and running. Nomura currently has no onshore presence in the country; building out infrastructure and hiring staff will take time.

Even with the shares gaining 45% since first-quarter results on July 31, not one of the 12 analysts tracked by Bloomberg who follow Nomura has a “buy” recommendation on the stock. Blame that pessimism on an aging society. Japan is getting too old to seek risk: An estimated 80% of shares inherited from people who die are sold into the market. No wonder then that Nomura’s retail brokerage business, which still garners roughly 30% of its total revenue, continues to bleed cash and securities.

Nagai can’t do much about Japan’s demographics. But to attract millennial customers, he needs to step up investment in newer digital technologies and younger talent.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.