EU Leaders Are Ready for Hard Brexit. EU Firms Aren’t.

(Bloomberg Opinion) -- As Prime Minister Theresa May continues to bang her head against a hard Brussels wall, the probability that the U.K. will leave the European Union without an orderly separation agreement increases with every wasted day.

The biggest loser if that happens would be the U.K., but the EU countries also have a stake. They haven’t neglected preparations for a no-deal Brexit, but there appears to be a sizable gap in preparedness between governments and businesses, which are still having a hard time believing in a no-deal outcome.

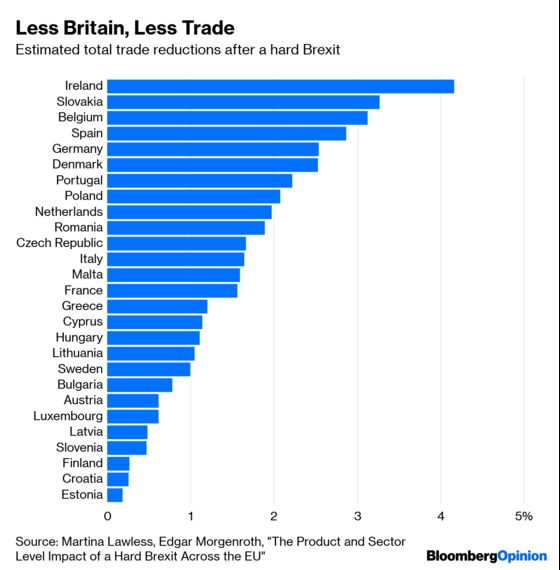

Last year, a team of International Monetary Fund researchers published an estimate of Brexit’s long-term economic impact on EU member states: An output decline of up to 4 percent for Ireland but no more than 1 percent for the others if no deal is reached. Other studies have also predicted a comparably small impact. Perhaps the best way to understand what a hard Brexit is going to do to European economies is to estimate the trade losses that will result from applying World Trade Organization tariffs. Irish economists Martina Lawless and Edgar Morgenroth have done the calculations using sector-level data.

The more important trade is for a country, the more these losses will hurt.

Ireland has a higher trade-to-economic-output ratio than all EU countries except Luxembourg. Combined with a high estimated trade loss, that means Ireland is the most exposed country, followed by Slovakia, Belgium and the Netherlands. Not coincidentally, Ireland, the Netherlands and Belgium have been especially focused on Brexit preparedness.

Ireland’s contingency plan is 70 pages long. It shows a thorough understanding of the anticipated change. Funds have already been allocated for hardware and software to produce the extra documentation needed if trade shifts to WTO terms. Provisions have been made for extra inspection bays and truck parking at ports, as well as for extra staffing where new border barriers will require it. The government, with the European Commission’s help, has identified the legislation that will need to be amended by the end of March if the U.K. appears ready to crash out of the EU as now scheduled on March 29.

It’s impossible fully to insulate Irish businesses from the consequences of a hard Brexit, but the government has tried. For 2019, it created a 300 million-euro ($342 million) loan scheme to help affected companies in addition to another, shorter-term 300 million-euro program started last year. Farmers are getting subsidies to compensate export losses and deal with the potential increase in red tape at the border.

The Irish government even runs a special Twitter account for preparedness updates. But anecdotal evidence suggests that Ireland’s actual readiness for a hard Brexit at the end of March may not be all that high. The ports’ expansion hasn’t gone fast enough, and disruptions are likely in the first weeks after the rules of trade change. Transport companies haven’t hired the new staff necessary to deal with customs declarations.

“We are, to put it bluntly, screwed” in the event of a cliff-edge Brexit, Simon McKeever, head of the Irish Exporters’ Association, told an industry conference in January.

The Dutch and Belgian governments have created special web portals on Brexit preparedness, including versions of a “Brexit impact scan” — a questionnaire that businesses, and in the Netherlands also local officials, can answer to get recommendations on how to prepare. As in Ireland, thousands of people in the Netherlands and Belgium have attended Brexit orientation events. Tens of thousands have gone through the “scan.” One might think Dutch and Belgian businesses would know enough to be ready.

And yet, at the end of 2018, the last time the Dutch Chamber of Commerce updated the “Brexit Barometer” it uses to assess the preparedness level of its businesses, 58 percent had made no preparations for a no-deal scenario and 34 percent said they had no idea what it would mean for them.

In Belgium, Finance Minister Alexander De Croo said last month that 80 percent of local companies that do business with the U.K. weren’t ready for a new customs regime.

In some countries that will be hit relatively hard by a cliff-edge Brexit, such as car-industry hub Slovakia, not even the government is doing much beyond adjusting some legislation in line with EU recommendations and deciding on the status of stranded Britons (in most EU countries they’ll be given a year or more to apply for residency). Slovakian Prime Minister Peter Pellegrini has said the country’s economy will keep growing fast regardless of Brexit. “If many companies decide to leave the United Kingdom as a result of a hard Brexit, it may even be an advantage for Slovakia,” he said.

Like neighboring Poland, Slovakia is also hoping its citizens will come home from the U.K. after Brexit to help alleviate a labor shortage; it’s even held events in London calling on Slovaks to return.

Bigger countries will feel a smaller impact and face higher absolute losses. But Germany, France and Spain also face gaps between their governments’ strong awareness of what a cliff-edge Brexit would mean and skepticism by businesses that such an event is plausible.

The German Association of Industry and Trade Chambers has created a Brexit preparedness questionnaire similar to those used by the Dutch and Belgian governments, and a representative of the association said in late January that it had been downloaded 23,000 times in the previous two months. But when asked whether German business was prepared for a hard Brexit, Martin Wansleben, the group’s head, replied that he couldn’t understand how that was possible:

You don’t know exactly what’s going to happen with the customs duties. You also don’t know, and this is a very important point, whether you can actually put the customs duties, which increase the price of your products for England, on top of the prices. Will the English pay more in the future, or will that be on their margins? And you don’t know what will happen to economic development in England, because there are difficulties there. So I don’t think you can really prepare for chaos.

The preparedness gap between governments and businesses is likely to affect the outcome of May’s negotiations with the EU.

Irish and continental political leaders and the top EU officials feel they’ve done a lot to prepare for every Brexit-related eventuality. Indeed, it’s difficult to expect more from them than they’ve already done. They’ve analyzed the necessary regulatory changes, drafted and passed legislation, put aside funds and conducted outreach.

Their well-deserved confidence that they’ve done their homework helps them negotiate firmly with May. As far as they’re concerned, disaster won’t strike them even if no deal is reached — and indeed, while a hard Brexit would cost the EU many billions of euros, its impact is unlikely to be devastating.

On the other hand, as Brexit Day approaches, it’s likely that increasingly anguished cries from business executives will reach the political leaders’ ears. Entrepreneurs who didn’t take precautions because a hard Brexit seemed too insane to contemplate will finally get worried, too late to avoid losses and chaos. That prospect strengthens May’s otherwise weak hand and bolsters hope for a last-minute compromise.

To contact the editor responsible for this story: Jonathan Landman at jlandman4@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Leonid Bershidsky is Bloomberg Opinion's Europe columnist. He was the founding editor of the Russian business daily Vedomosti and founded the opinion website Slon.ru.

©2019 Bloomberg L.P.