Nissan’s Silent Minority Deserves to Be Heard

All shareholders are supposed to have a voice. At Nissan Motor, only France’s Renault SA seems to have one.

(Bloomberg Opinion) -- All shareholders are supposed to have a voice. At Nissan Motor Co., only France’s Renault SA seems to have one.

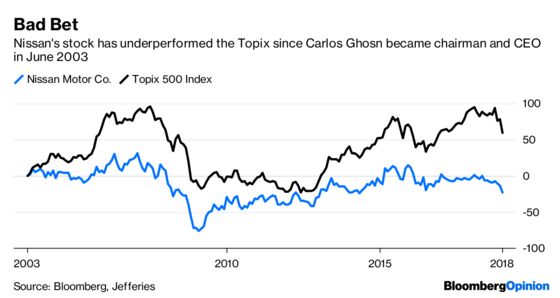

Since the arrest of Carlos Ghosn in November, the Japanese automaker has been wading through a long list of corporate governance failures. Last week, CEO Hiroto Saikawa said fixing them was his main priority. Meanwhile, Nissan investors have tossed and turned over every detail of the imprisoned executive’s unavoidable exit.

They might be better served questioning Renault’s outsize role in the Japanese company, which has effectively stonewalled minority shareholders including Japan’s Government Pension Investment Fund, Daimler AG and a host of international asset managers.

Renault’s major stake is a legacy of sorts. After rescuing Nissan decades ago, it now owns just over 43 percent of the company. Yet there’s little transparency about the agreement that governs this alliance, only part of which is in the public domain. That looks like a grave omission of information for publicly listed companies with a cumulative market capitalization of more than $60 billion.

As a result, getting clarity on the path that extracts the most value for the remaining 57 percent of stockholders – full independence from Renault – is close to impossible. Several scenarios detailing the companies’ future relationship after Ghosn’s removal have been war-gamed, but few investors or observers can be sure about the exact terms.

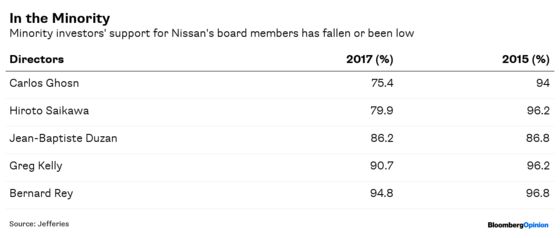

It’s quite possible that the blow from the Ghosn debacle would have been less severe if minority shareholders were heard in the first place. In 2017, most of them voted to remove the legendary auto boss, according to Jefferies Japan Ltd.’s Zuhair Khan, but he stayed on with Renault’s backing. The same support kept Jean-Baptiste Duzan – a retired Renault executive who became a so-called independent director of Nissan – on the board.

Japan Inc. has historically ignored its smaller shareholders, though the country’s latest corporate governance code gives vague assurances they can actually exercise their rights, including the ability to file a shareholder lawsuit and seek an injunction.

As we’ve written, the last thing Nissan needs is the weight of Renault: The 1999 rescue has run its course. Unwieldy and time consuming as it may be, an end to the alliance may be the only way forward if Nissan wants to regain its competitiveness in its largest target markets by sales – the U.S. and China. On Monday, Bloomberg News reported the Securities and Exchange Commission is investigating whether Nissan accurately disclosed its executive pay in the U.S., citing people familiar with the matter. That only deepens its problems.

The financial upside of the alliance is much clearer for Renault. Its stake in Nissan is worth more than 80 percent of its market capitalization, according to CLSA Ltd. Nissan has increasingly brought more to the table, while taking on the risk of the French company. In 2017, Renault’s 2.8 billion euro ($3.19 billion) affiliates income (mostly from Nissan) was larger than its own 2.6 billion euro figure. The more than 700 million euros of dividends from the Japanese company boosted cash flows and helped fund the 916 million euros of dividends to its own shareholders, according to Moody’s Investors Service.

Operationally, the two companies merged their production systems to create the “Alliance Production Way.” Yet France was never known for being an industrial or manufacturing powerhouse like Japan. From Silicon Valley to Yokohama and Detroit, Nissan has research and development centers sprinkled across the globe and has been behind the companies’ technological advances. On a unit cost per vehicle basis, Renault has benefited from the partnership because it makes mass-market cars.

So, if all of Nissan’s shareholders had a voice, what would the company do next? Under various clauses in the agreement that governs the companies’ alliance, the Japanese carmaker could raise its stake in Renault to 25 percent from the current 15 percent, and dilute the French company’s voting rights. The caveat is that this can only happen if there’s evidence of Renault’s “interference” in board matters. Given the company’s control, it’s unclear how the board could come to that conclusion in a balanced way.

In an interview at Davos with Bloomberg TV last week, France’s Finance Minister Bruno le Maire said the first job at hand for Renault’s new management team “is to consolidate the alliance between Renault and Nissan.” The French government has a 15.01 percent stake in Renault. Meanwhile, the alliance put out a statement in November that the boards of Renault, Nissan and Mitsubishi Motors Corp. (added in 2016) have “individually and collectively – emphatically reiterated” their commitment to the two-decade-old partnership.

Through all those platitudes, we still can’t hear the minorities.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.