(Bloomberg Opinion) -- A funny thing happens when the economy booms: Investors crawl out on thinner and thinner limbs. It’s happening right now in the bond markets, where the only part that is lucrative is usually the least appealing to all but the nerviest players: distressed state and local governments with the lowest credit ratings (or none at all). Think of bankrupt Puerto Rico, tobacco settlements with diminishing revenues, and the not-yet-finished New Jersey Mega Mall.

Investors can’t get enough of this junk while shunning Treasuries and similar investment-grade securities. For them, the risk remains tolerable as long as times remain good. So they watch with the most interest for hidden signs of economic weakness even when the economy expands.

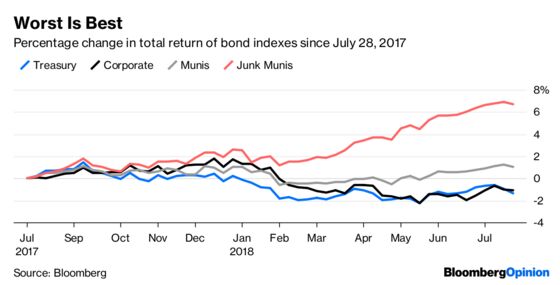

That’s another way of saying that times must be good if demand exceeds supply for the highest-yielding, riskiest government debt. Excluding municipal junk, the year so far is the worst two quarters in the bond market since 2013, which happened to be the turning point in the recovery from the meanest recession since the Great Depression. The Commerce Department said last month that second-quarter gross domestic product increased 4.1 percent, the most since 2014. The chairman of the White House Council of Economic Advisers, Kevin A. Hassett, predicts a four-quarter growth rate of more than 3 percent, which would be the highest in 13 years.

Such robust data helps explain why junk munis outperformed the rest of the U.S. bond market over five years, three years and during the past 12 months, according to data compiled by Bloomberg. Bondholders lost money in 2018 owning investment-grade U.S. government, corporate and municipal debt. In contrast, they have a total return (income plus appreciation) of 4 percent with junk munis. The appeal is reinforced by the record investment in the VanEck Vectors High-Yield Municipal Index ETF, the largest exchange-traded fund tracking junk munis.

Among the 62 U.S.-based high-yield mutual funds with assets greater than $1 billion and at least three years of history, eight of the top 10 performing funds this year are focusing on municipal debt. The No. 1 Oppenheimer Rochester High Yield Fund, which outperformed its peers over five and three years, is beating the market for state and local government debt by 8 percentage points with especially large holdings of Puerto Rico, Ohio, Alabama, Wisconsin and District of Columbia securities, according to data compiled by Bloomberg.

The favorite for many of the top funds are Sales Tax bonds sold by the Puerto Rico Sales Tax Financing Corp. The securities, which are in default, are rated “highly speculative” by Moody’s and have no rating from Standard & Poor’s. They’ve almost doubled in price, from 43 cents on the dollar in January to 82 cents. Tobacco debt, such as California’s non-rated $1.7 billion June sale due in 2047 and backed by its share from the state’s 1998 legal settlement with cigarette makers, similarly rallied to more than 102 cents on the dollar as soon as they traded, according to data compiled by Bloomberg.

To be sure, any evidence that the expansion is on its last legs could make high-yield municipal bonds the first casualty of the downturn. For now, the bond market isn’t forecasting that scenario.

In the meantime, the largest offering of unrated municipal bonds last year — the $1.1 billion raised to finish the American Dream complex in New Jersey’s Meadowlands (a bet against the demise of shopping malls) is among the more profitable investments in the market, trading at 115.8 cents on the dollar — better than anything rated investment-grade.

(With assistance from Shin Pei)

To contact the editor responsible for this story: Jonathan Landman at jlandman4@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matthew A. Winkler is a Bloomberg Opinion columnist. He is the editor-in-chief emeritus of Bloomberg News.

©2018 Bloomberg L.P.