This Activist Investor Should’ve Believed More in His Plan

(Bloomberg Opinion) -- Spoke too soon.

The last time I wrote about our old friend Richard “Mick” McGuire, Activist Investor, I gave him credit for knowing how to make a buck, though I was admittedly dubious about the value of his so-called shareholder activism. In particular, I pointed to the 2017 returns of his hedge fund, Marcato Capital Management LP, which were stellar: up 21 percent.

But hey, you know what they say in the investment biz: “Past performance is no guarantee of future results.” Sure enough, McGuire’s 2018 results were a big letdown to his investors; Marcato ended the year down 12 percent. (By contrast, the S&P 500 index was down 4 percent last year.) According to Bloomberg, McGuire’s hedge fund shrank by $300 million, from just under $1 billion to a little less than $700 million.

A year and a half ago, when I first got interested in the 42-year-old Bill Ackman protégé, I wanted to find out whether McGuire actually knew anything about how to fix troubled companies— or whether his real goal was to make money on the inevitable run-up brought about by his cage-rattling.

At the time, he had Buffalo Wild Wings Inc. in his sights, a midsize company whose stock had dropped 26 percent over the previous 18 months. Claiming the company needed to improve its “four-wall margins” and transition to a model that “reduces the capital intensity” — yadda, yadda — McGuire launched a proxy fight to replace four board members. And he won! Three of McGuire’s four board candidates were voted in by shareholders, the chief executive resigned, and for all intents and purposes, the company was his.

Alas, Buffalo Wild Wings under McGuire didn’t do much better than under the previous management. In December 2017, McGuire was bailed out by Roark Capital Group, a hedge fund with actual experience in turning around restaurant chains. It bought the company at a price that locked in a nice gain for McGuire.

McGuire’s second foray in 2017 was aimed at Deckers Outdoor Corp., maker of Ugg boots, Teva sandals, Hoka sneakers and other fashion footwear. His list of Deckers’s sins was long: The company didn’t have an outside board member with fashion or retail experience. Its chairman, Angel Martinez, was busy running for mayor of Santa Barbara, California, instead of overseeing the company. It consistently missed its targets for margin growth and earnings per share. It had too many retail outlets. Its expenses were growing faster than its revenue. And on, and on.

McGuire demanded that the company put itself up for sale. When the Deckers board refused, he launched his second proxy fight of 2017, this time vowing to replace the entire board. Although he later pared that back to three board members, when the vote was held in December, he was soundly defeated.

Or was he? Once investors knew McGuire was gunning for Deckers, the stock started to rise, going from the high 40s to the mid-70s. Martinez resigned as chairman, just as McGuire had demanded. Most tellingly, Marcato’s activist push appears to have focused Deckers to do exactly the things McGuire had been calling on it to do.

And it worked! As 2018 progressed, Deckers closed some retail stores. It reignited its best brands, starting with Ugg. It regained control of its expenses. It added two independent directors who had retail and fashion experience. (One of the new directors was a former top Nike executive.) It boosted margins.

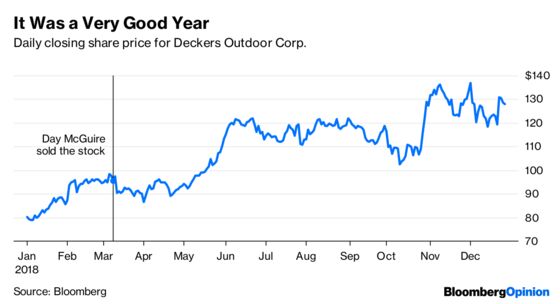

All the while, the stock kept climbing, from $79 in January to $95 in March to $137 in December. (It stood at $128 when 2018 ended.) In all, Deckers Outdoor rose 38 percent last year. When the company held its quarterly conference call in late October, it was a love fest, with the analysts falling all over themselves to congratulate the company on its results. It saw year-over-year increases in revenue, gross margins, operating income and earnings per share.

Not all of this was the result of the McGuire plan. (He declined to comment for this column.) According to Sam Poser, who follows the company for Susquehanna International Group LLP, a key factor was Deckers’s ability to reduce its inventory — which McGuire rarely mentioned when he was attacking the company — and to come up with new products, including slippers. Plus, he said, “there was a ton of bad weather last winter,” which helped drive Ugg sales.

Still, the company largely followed McGuire’s blueprint and was rewarded with a rising stock price. Except that McGuire was no longer around to enjoy the fruits of his ideas; he dumped Marcato’s position on March 8, a day when the stock hit $95 a share. Thus he missed the bulk of Deckers’s 2018 gain — a gain that was in no small part the result of his pressure and his ideas.

Now, one can’t be too critical of a hedge fund manager who sells a position that has more than doubled. He bought Deckers to make money for his investors — and he succeeded. But once he’d gotten his pop in the stock, he bailed.

Which is too bad. Had he stuck with Deckers, his 2018 would have been considerably less painful. But to do that would have required McGuire to actually believe in his ideas for fixing the company. Instead, he played the company for a quick gain.

The former is what real shareholders do. The latter is what “shareholder activists” do.

Although let’s not get too carried away: The S&P 500 index was also up 21 percent in 2017.

To contact the editor responsible for this story: Stacey Shick at sshick@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Joe Nocera is a Bloomberg Opinion columnist covering business. He has written business columns for Esquire, GQ and the New York Times, and is the former editorial director of Fortune. He is co-author of “Indentured: The Inside Story of the Rebellion Against the NCAA.”

©2019 Bloomberg L.P.