Maybe We Have the Economic-Growth Equation Backward

(Bloomberg Opinion) -- Productivity drives all long-term increases in economic output. And although rising inequality and other forces have caused wages to increase more slowly than productivity, wages won’t grow in the long term unless the economy becomes more efficient at turning inputs into economic value. More fundamentally, gains in the economy’s productive power make the world seem less like a zero-sum game, where the only way to get rich is to beggar one’s neighbor.

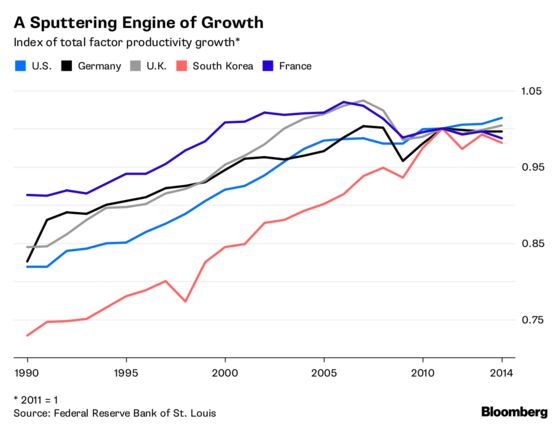

Starting in about 2005, something ominous happened to the global economy -- productivity growth began to stagnate:

Much ink has been spilled over the question of how to raise productivity growth. Typical answers include spending more on research and eliminating regulations that hold back innovation.

These are all ideas worth considering, but they share one important characteristic -- they are, fundamentally, about the supply side. They reflect a view of the economy as split into two basic components -- a long-term trend driven by technological and institutional factors, and a temporary fluctuating cycle of booms and recessions driven by aggregate demand. In this view, policies like monetary easing and fiscal stimulus can potentially help dig an economy out of a recession, but they can do little or nothing to raise potential output in the long term.

This supply-side view of sustainable growth permeates modern economics, from undergraduate classrooms to cutting-edge macroeconomic models to the writings of economics pundits. This is why supply-side solutions such as research spending and deregulation dominate the productivity discussion. But it may be time to momentarily step away from economic orthodoxy and look at demand-based policies to help boost productivity.

During the 2016 presidential primary campaign, some supporters of Bernie Sanders argued that their candidate’s spending proposals would substantially raise long-term growth. This claim was pooh-poohed by mainstream Keynesian economists, and in fact the numbers the Sanders supporters were throwing around were almost certainly too high. But the discussion did manage to revive an interesting concept known as Verdoorn’s Law.

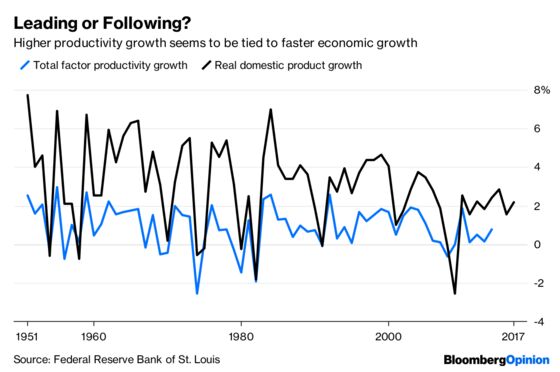

Verdoorn’s Law, named after Dutch economist Petrus Johannes Verdoorn, describes a correlation between output and productivity -- when growth is faster, productivity also grows faster. You can see this correlation in the data:

That correlation persists even when more careful statistical techniques are used. Macroeconomists Iván Kataryniuk and Jaime Martínez-Martín found a robust relationship across a large number of countries.

The standard, mainstream interpretation is that productivity is driving the cycle -- that improvements in technology or government policy cause booms, and that innovation slowdowns or policy mistakes cause busts. That fits with the narrative that, for example, advances in information technology powered the roaring economy of the late 1990s.

But careful analysis of the data suggests that technological improvements probably aren’t actually driving the business cycle. That leaves open the tantalizing possibility that the reverse is happening -- that high levels of aggregate demand also drive up productivity.

There are several ways this could happen. First, recessions tend to destroy workers’ productivity, because their skills and networks deteriorate when they’re out of work. So doing more to minimize job losses in recessions can help the economy be more productive.

But even more importantly, it’s possible that economic booms cause companies to invest more in new technologies -- the latest machine tools, the best software -- and to develop new business models around the latest innovations. New ideas don’t just instantly make companies more productive -- the companies have to put some work and money into incorporating those new ideas into their businesses, both physically and organizationally.

That’s where the demand side comes in. When aggregate demand is high, and companies are scrambling to expand and meet the flood of orders, the investments they make may push productivity permanently higher. The fast productivity growth of the late 1990s and early 2000s may not have been simply a lucky result of widespread use of new computer and internet technologies; it might be that a boom in demand caused companies to adopt those new technologies more rapidly.

That may or may not be the case -- it’s very hard to tell, and much more research is needed. But the mere possibility suggests that running the economy hot, through continued monetary and fiscal stimulus, is a better idea than people realize.

Typically, the choice of whether to apply macroeconomic stimulus is thought of as a tradeoff between unemployment and inflation. With both unemployment and inflation low, the Federal Reserve appears to be comfortable with the current policy stance -- Fed Chairman Jerome Powell has seemed to suggest that he would be comfortable with slightly higher interest rates.

But the chance for additional productivity gains from high aggregate demand -- call them Verdoorn effects -- should inform this calculus. It means that there is additional upside to keeping rates lower for longer, besides simply putting the last few unemployed Americans back to work. Other rich countries, too, should think twice before they raise their own interest rates.

Raising productivity growth is such an important and difficult task that policy makers should employ any tool that might get the job done -- even if it isn’t yet accepted in mainstream macroeconomics.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.