Markets Struggle With the Meaning of ‘Substantially’

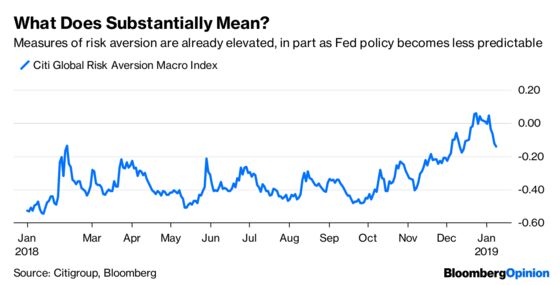

(Bloomberg Opinion) -- Over the years, the Federal Reserve has used rather ordinary words and phrases to describe its attitude toward monetary policy that have nevertheless beguiled investors as to their true meaning. For example, what exactly constitutes a “gradual” pace of interest-rate increases? Fed Chairman Jerome Powell may have just come up with a new one for market participants to debate: substantially.

At the Economic Club of Washington, D.C., on Thursday, Powell said the central bank is sticking with its process of shrinking its balance sheet assets to a more normal level, which removes stimulus put into place to revive the economy after the financial crisis and recession a decade ago. The balance sheet, which reached a peak of $4.52 trillion before falling to a recent $4.06 trillion, “will be substantially smaller than it is now” though bigger than it was before the crisis, Powell said. He said he didn’t know the exact level. This is important because many investors and strategists contend that the expanding balance sheet was one of the primary drivers of the big gains in equities and riskier assets in recent years. And the reason riskier assets performed so badly in late December was because Powell, during his press conference after raising interest rates on Dec. 19, largely dismissed the building turmoil in markets and suggested the balance sheet rundown that began in late 2017 would remain on a sort of autopilot. But what markets truly want is some clarity on what Powell and the Fed think the appropriate size of the balance sheet should be and how fast it will get there. Is it closer to the less than $1 trillion it was before the financial crisis, or the midpoint of $3.52 trillion since then or something else? Powell and the Fed probably don’t know the answer, but it’s sure to become a hot topic anytime Powell gives a speech or holds a press conference after a monetary policy meeting.

“I’m tired of the game of semantics when it comes to what Federal Reserve officials say,” Bleakley Financial Group chief investment officer Peter Boockvar wrote in a note to clients after Powell’s comments. “I guess we’ll then wait for his next speech so everyone can then ask him what ‘substantially smaller’ means.”

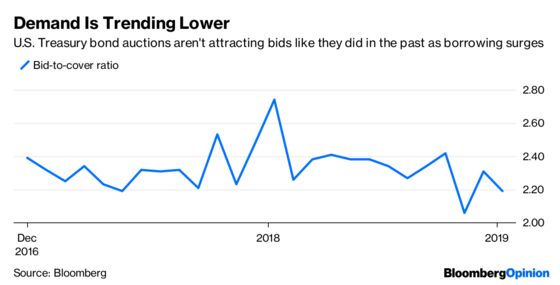

DUD AUCTIONS ARE ADDING UP

The U.S. sold $38 billion of three-, 10- and 30-year Treasuries this week in three separate auctions, and two of them can be considered disappointments. Tuesday’s sale of three-year notes drew bids for just 2.44 times the amount offered, the lowest so-called bid-to-cover ratio since 2009. Wednesday’s offering of 10-year notes was average, and demand at Thursday’s auction of 30-year bonds tied for the second-lowest for that maturity since 2016, helping to push yields to their highest in two weeks. It’s understandable that demand would be a bit soft given the big rally over the past few weeks as investors sought a haven from the turmoil in stocks and other riskier assets. But even so, demand has been trending lower for about a year, underscoring the challenge it will be for the U.S. to find willing buyers as it ramps up borrowing to finance what is expected to be a $1 trillion federal budget deficit. The International Monetary Fund’s latest quarterly report on global foreign-exchange reserves released Dec. 31 showed that the dollar accounted for 61.9 percent of global reserves at the end of the third quarter, t he lowest level since 2013. Last year, the amount of Treasuries outstanding jumped by $1.14 trillion in the biggest increase since the financial crisis. It’s not so much that the U.S. will suffer a failed auction, just that the rates it offers will most likely be higher than they otherwise would be if debt and deficits were lower.

THE STREAK CONTINUES – BARELY

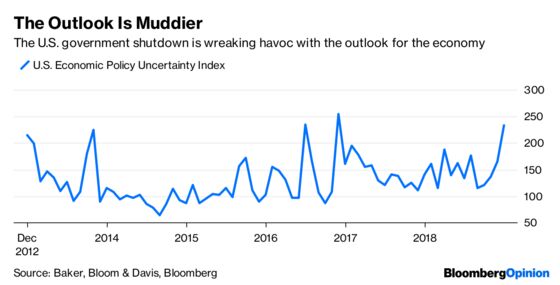

U.S. and global stocks strung together their fifth consecutive gain on Thursday, but it wasn’t an easy ride. The S&P 500 Index fell as much as 0.89 percent soon after the open before clawing back those losses to end 0.21 percent higher. That may not seem impressive, but consider that stocks took a big hit early in the U.S. afternoon around the time that President Donald Trump tweeted that he was scrapping his trip to the annual World Economic Forum gathering of global financial elites later this month in Davos because of the government shutdown. In other words, the gain in stocks may have been much more impressive if not for the tweet, which suggests that there’s no end in sight to a shutdown that may soon start having a noticeable drag on the economy. “I think we’re stuck,” said Republican Senator Lindsey Graham of South Carolina, who has been trying to forge a compromise to end the partial shutdown. “I just don’t see a pathway forward.” The thinking among economists is that every week that the government remains closed shaves about 0.1 percentage point from gross domestic product. It may be an old Wall Street cliché, but there’s some truth in the saying that markets hate uncertainty, which puts the recent rebound in equities over the past two weeks in doubt. The U.S. Economic Policy Uncertainty Index, which tracks news flow, ended 2018 at its highest level since 2016. “The impact of that uncertainty is already evident in plunging readings for business surveys and signs that this is passing through to weaker orders for non-defense capital goods,” Bloomberg Economics noted in a report on the shutdown.

BOLSONARO’S BULL MARKET

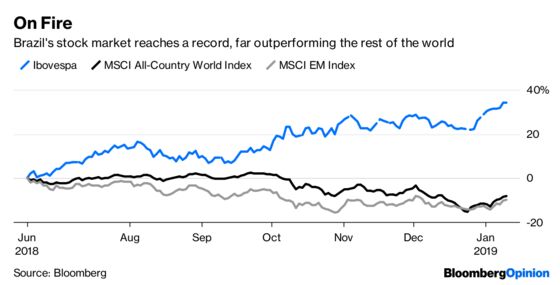

Talk about strong. Brazil’s stock market not only bucked last year’s big slump in emerging-market equities but also the scary collapse in global stocks in December. Since about mid-June, Brazil’s benchmark Ibovespa has soared about 34 percent to a record high, compared with a slide of 8.38 percent in the MSCI All-Country World Index and a drop of 9.79 percent in the MSCI Emerging Markets Index. The outperformance is partly a reflection of investor optimism that new President Jair Bolsonaro, a populist who brings with him big plans for reform and who was inaugurated on Jan. 1, will be able to push through his market-friendly economic proposals. To the strategists at Brown Brothers Harriman, the market’s euphoria is getting a bit overdone. After all, the economy is still weak. The World Bank this week predicted growth this year of 2.2 percent for Brazil, which is anemic for an emerging-market country. “We cannot help but think that investors have gotten overly bullish on Bolsonaro and his reform prospects,” the Brown Brothers strategists wrote in a research note Thursday citing everything from downside risks in its growth forecasts to the need for pension and tax reforms to a budget deficit that is a whopping 7.1 percent of GDP. “We expect Brazil equities to start underperforming, as suggested by its very underweight (weighting) in our EM Equity Allocation model,” the strategists added.

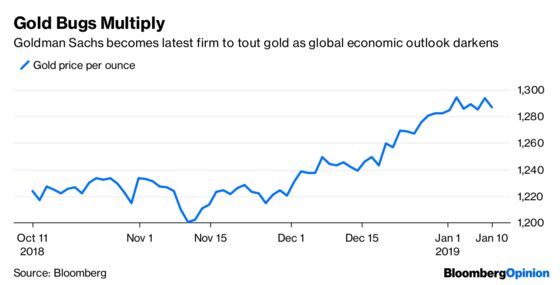

GOLD’S BANDWAGON GETS CROWDED

The price of gold has jumped almost 10 percent since mid-August, to about $1,287 an ounce on Thursday as investors seek out traditional havens amid signs the global economy is slowing and riskier assets get pummeled. Recent data from the U.S. Commodity Futures Trading Commission show money managers’ bullish bets on gold outnumbered their bearish wagers for the first time in five months. Exchange-traded funds have boosted their holdings to the highest since May. Now, one of the most influential voices in the global markets is saying that the gains are far from over, which is good if you’re a gold bug but maybe not so good if you’re positioned for a rebound in riskier assets such as stocks. Goldman Sachs Group Inc. raised its price forecast for bullion, predicting that over the next 12 months the precious metal will climb to $1,425 an ounce — a level not seen in more than five years, according to Bloomberg News’s Marvin G. Perez. Speculative interest in gold signals investors are not only closing bearish bets but are also adding to their bullish position, Suki Cooper, a New York-based analyst at Standard Chartered, wrote in a research note. “We expect the safe haven bid, and to a lesser extent gold’s inflation hedge properties, to remain key drivers of the metal’s price in 2019, complemented by a resurgence of physical demand,’’ Cantor Fitzgerald analysts led by Mike Kozak wrote in one of their reports.

TEA LEAVES

The U.S. government shutdown has caused many important economic releases to be postponed. The Labor Department’s monthly consumer price index report is one of the exceptions. The median estimate of economists surveyed by Bloomberg is that the government will say that the inflation rate fell 0.1 percent in December while rising 1.9 percent from a year earlier. Excluding food and energy, the measure is expected to rise 0.2 percent for the month and 2.2 percent from a year earlier — both the same as in November. In short, the report is likely to confirm that inflation is well under control, which is a reason Fed officials have been out in force recently saying they can be patient before raising interest rates again. “The inflation outlook will define the policy path this year,” the team at Bloomberg Economics wrote in a research note. “Fed officials project (core inflation) to remain roughly in line with the central bank’s target this year, which creates risk that further removal of policy accommodation will be slow. However, if wage-driven inflationary pressures materialize more meaningfully, the Fed will not hesitate to deliver more hikes.”

DON’T MISS

How the Fed Can Engineer a Soft Landing in the Economy: Tim Duy

Don’t Be So Sure Hyperinflation Can't Hit the U.S.: Noah Smith

AB InBev Is Looking for a Long-Term Commitment: Brian Chappatta

Matt Levine’s Money Stuff: Investors Have to Sell Stocks Too

Stock Market’s Correction Is Rudely Interrupted: John Authers

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.