Markets Are Signaling Higher Odds of a 2019 Recession

The acceleration in the timing of a downturn is reinforced by the speed with which financial assets have slumped.

(Bloomberg Opinion) -- For investors attempting to adjust their portfolios in anticipation of a recession by the end of 2020, recent economic indicators carry a message: they may have to prepare for the downturn to start as early as 2019 despite stocks enjoying a recent “dead-cat bounce.” Bloomberg News reports that a Federal Reserve Bank of New York gauge puts the chances of a recession at almost 16 percent a year from now, the highest since November 2008.

The acceleration in timing of a downturn is signaled by the speed with which markets have moved, with the most important being the plunge in oil prices. Despite an agreement early last month between OPEC and Russia to reduce oil output by 1.2 million barrels per day starting this month, the price of West Texas Intermediate crude has fallen more than 40 percent from its high for the year in early October. This is because the demand for energy is expected to fall even more than the reduction in production that the OPEC+ countries will implement.

The International Monetary Fund has lowered its global growth forecast for 2019, with the U.S. and Chinese economies expanding more slowly. On Monday, it was revealed that China’s manufacturing purchasing managers index dropped to 49.4 in December, the weakest since early 2016 and below the 50 level that denotes contraction. Japan, one of the world’s largest oil importers, experienced a contraction in gross domestic product in the third quarter, and economic weakness is expected to persist into 2019.

Recent figures for U.S. housing, the backbone of the domestic economy, show weakness in housing starts, single-family home completions and mortgage applications. The rise in home prices since the last financial crisis, combined with relatively small increases in wages and salaries, have reduced affordability. The double-whammy was so severe that it caused home buyers to delay purchases, resulting in the 30-year fixed mortgage rate falling to 4.54 percent in late December from 4.82 percent in early November, according to Bankrate.com. Still, the rate is up from 3.85 percent at the beginning of 2018.

The recession die was cast when the Federal Reserve on Dec. 19 increased its target for the benchmark federal funds rate for the fourth time this year. While the rate hike was priced into market expectations, the announcement by Chairman Jerome Powell at his press conference that the central bank expects to raise rates two more times in 2019 came as a shock. Powell worsened the impact on markets by stating that the Fed’s balance sheet assets, now being reduced at a monthly pace of $50 billion, was on “auto pilot.”

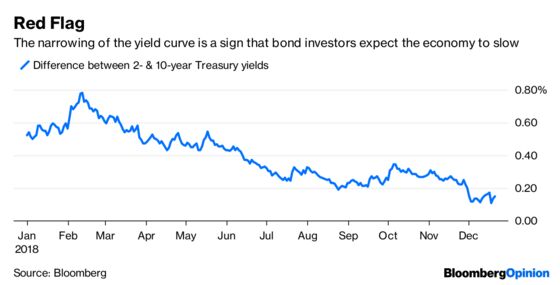

Bond markets signaled the increased likelihood of a speedy recession with two important U.S. Treasury yield curves inverting last month, with yields on five-year notes falling below those of two- and three-year notes. The more widely watched spread between two- and 10-year Treasury yields narrowed significantly following the Fed’s rate boost and Powell’s comments to less than 10 basis points.

Developments last month are key as investors form their 2019 outlook:

• U.S. economic growth is likely to slow in the first half of the year from the fast pace set during the second and third quarters of 2018 as the impact of the year-end 2017 corporate tax cut fades.

• The U.S. economy may not post two successive quarters of negative growth in terms of gross domestic product by mid-2019, although it will feel as if the economy entered a recession.

• Instead, the National Bureau of Economic Research, the unofficial arbiter of economic cycles, defines a recession as a “significant decline in economic activity, spread across the economy, lasting more than a few months.” Expect this to be reflected in falling equity prices in a wide range of sectors, but only after the two- to 10-year part of the Treasury yield curve has inverted.

• Powell did not please investors at his Dec. 19 press conference. Instead, he dispensed tough love. Once signs of economic weakness become apparent, not only will the Fed not be able to raise rates twice this year, but it could either cut rates or stop reducing its balance sheet assets. A “Powell Put” is likely to be delayed, but not denied.

• Based on the experience in the last recession, the spread between two- and 10-year Treasury yields may again become positive toward the end of 2019 as the Fed cuts rates. For example, the spread hit a high of 250 basis points in November 2008 when the economy was still in recession.

• Expect long-dated Treasury securities to fall in yield, providing a positive return during the recession.

• Even as the slope of the Treasury curve becomes positive, equities may start feeling the impact of the ongoing recession. This is likely to be the asset class that feels the brunt of the recession.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Komal Sri-Kumar is the president and founder of Sri-Kumar Global Strategies, and the former chief global strategist of Trust Company of the West.

©2019 Bloomberg L.P.