Markets Sense the Narrative May Be Changing

Cracks in a bullish storyline lead financial commentary. Plus, cratering crude, central bank gold bugs and more.

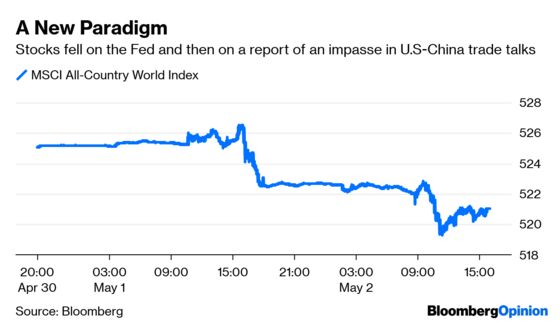

(Bloomberg Opinion) -- The story of global markets this year has been driven by two key themes: the Federal Reserve’s dovish pivot and purported progress in U.S.-China trade talks. In a matter of just 24 hours, however, both are at risk of going from a net positive to a net negative.

The Fed’s decision in January to suggest that it may not need to raise interest rates in 2019 has fueled this year’s gains in equities and sparked a rally in fixed-income assets, lowering yields and further loosening financial conditions. On the trade front, frequent pronouncements from the Trump administration that talks with China were, as economic adviser Larry Kudlow said Monday, making “very good progress” only bolstered investor sentiment. But now, it looks like investors can no longer count on either of things to underpin markets. On Wednesday, both stocks and short-term U.S. Treasuries fell after Fed Chair Jerome Powell seemed to doubt that the recent slowdown in inflation would last, saying the central bank didn’t see a strong case for moving rates down or up. That blindsided traders, many of whom had priced in a rate cut this year. Stocks extended their declines Thursday, with the MSCI USA Index falling as much as 0.81 percent and MSCI’s global index dropping 0.11 percent as China’s Global Times reported that trade watchers are wondering if China-U.S. talks have hit an impasse, as there were few details revealed after the latest meetings on Wednesday. Meanwhile, bonds declined across all maturities.

Maybe investors are overreacting. Powell certainly had a lot of incentive to knock some of the exuberance out of the markets, given how strongly equities and other risk assets have rebounded amid a growing climate of complacency seen in bonds and measures of volatility. Still, the way markets have responded to the Fed and the report on China’s trade talks suggests a new narrative may be developing centered on caution.

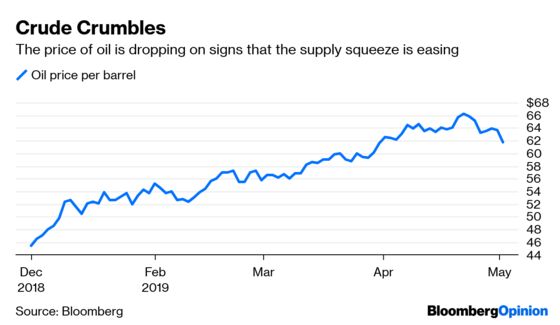

CRUDE CRATERS AS RUSSIA CHEATS

The Fed and trade talks weren’t the only catalysts for market moves on Thursday. Oil fell as much as 4.17 percent in its biggest decline of the year as two developments challenged the notion that the market is in for a supply squeeze. One was the release of data showing American crude inventories rose to the highest level in two years, according to Bloomberg News’s Alex Nussbaum and Grant Smith. The other was news that Russia missed a target for production cuts in April, dampening the impact of its agreement with OPEC to prop up prices. The decline in oil prices weighed on the shares of energy companies, making the sector the worst performer in the MSCI USA Index. At about $61.88 per barrel on Thursday, West Texas Intermediate crude prices are down almost 7 percent from this year’s high of $66.30 reached last week. The good news is that lower oil prices may bring relief at the pump. Prices for a gallon of regular-grade gasoline have risen to an average of $2.89 heading into the all-important summer driving season, according to the Automobile Association of America, up from January’s low of $2.23 a gallon. All else being equal, lower gasoline prices should provide a net benefit to consumer spending and help underpin the economy.

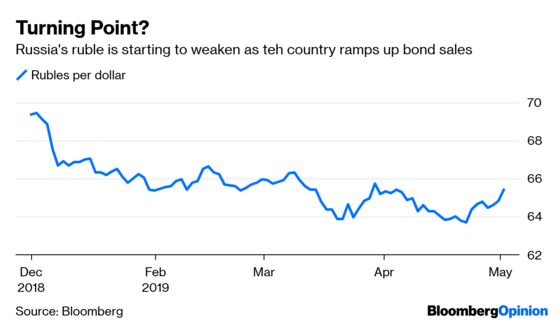

RUSSIA HAS A SUDDEN NEED FOR LOTS OF CASH

Speaking of Russia, the ruble was one of the world’s worst performing currencies Thursday, depreciating more than 1 percent. That’s to be expected on a day when oil is tanking, especially with low trading volumes in Russia due to a public holiday. But there may be something else going on. Russia’s economy is forecast to slow significantly this year, with the International Monetary Fund forecasting expansion of just 1.6 percent, versus 2.3 percent in 2018. Now comes word that Russia pumped more crude last month than agreed under the OPEC+ deal, thwarting Energy Minister Alexander Novak’s pledge to comply with the pact. Russia produced 45.97 million tons of crude in April, according to preliminary data from the Energy Ministry’s CDU-TEK unit. Does Russia need money? It’s hard to say, but it’s also curious that Russia borrowed more than four times its usual monthly average in April. Government ruble-bond sales totaled 400 billion rubles ($6.2 billion) for the month, the most on record, according to Bloomberg News’s Natasha Doff. Russia is running the widest budget surplus in a decade, so it doesn’t actually need to sell bonds, but bumper borrowing now could be a precautionary move to stockpile cash as the threat of new U.S. sanctions looms.

LOW INFLATION IS LOOKING STRUCTURAL

The drop in oil prices is having an impact on the bond market. Breakeven rates on five-year U.S. Treasuries — a measure of what bond traders expect the rate of inflation to be over the life of the securities — fell 3 basis points Thursday to 1.80 percent, the lowest level since the end of March. This is significant because the Fed closely monitors inflation expectations in the bond market as a gauge for helping to decide on monetary policy. The central bank, which has an inflation target of 2 percent, views expectations for rising prices as something of a self-fulfilling prophecy in that if markets and consumers expect faster inflation, it will likely happen. So, the drop in longer-term breakeven rates runs counter to Powell’s comments on Wednesday that today’s low inflation rates are likely to be transitory. On top of that, government data Thursday showed& productivity gains accelerated more than forecast last quarter to the fastest pace since 2014, further bolstering the notion that the expanding economy isn’t stoking inflation. The “productivity report is a good-as-it-gets confirmation the Fed’s inflation fears last year were misplaced,” FTN Financial chief economist Chris Low wrote in a note to clients. “Congress cut taxes effective early last year, unleashing a significant fiscal stimulus. At the time, the Fed noted it had no problem with faster growth as long as productivity accelerated.” Well, now we know it did, and it might have implications for monetary policy going forward.

WHAT DO CENTRAL BANKS KNOW?

Gold is considered one of those “haven” assets that investors flock to in times of turmoil, along with U.S. government debt and the yen. So it’s curious that central banks, which have more insight in the global economy and financial system than anyone else, are loading up on the shiny metal. First-quarter gold purchases by central banks, led by Russia and China, were the highest in six years, according to Bloomberg News’s Rupert Rowling. The increase of 145.5 tons represented a 68 percent jump from a year earlier, the World Gold Council said Thursday in a report. Russia remains the largest buyer as the nation reduces its U.S. Treasury holdings as part of a de-dollarization drive. To be sure, this isn’t exactly a new phenomenon. Central banks worldwide added more gold to their holdings in 2018 than all but one other time as heightened geopolitical and economic uncertainty drove them to diversify reserves, World Gold Council data show. The buyers are dominated by countries looking to reduce their dollar dependency, like Russia, and are typically nations with a lower share of reserves in gold than Western European countries, Rowling reports. Maybe the fact that central banks are loading up on gold is nothing to worry about now, but does anyone really want to take that chance, with all the talk of a global synchronized slowdown and the Institute for International Finance estimating global debt at $243 trillion, or more than three times worldwide gross domestic product?

TEA LEAVES

The monthly U.S. employment report will be released Friday, and the median estimate of economists surveyed by Bloomberg is for the economy to have created 190,000 jobs in April. That would be a solid number, little changed from the 196,000 jobs in March and the average of 214,000 over the past five years. Average hourly earnings are seen rising 3.3 percent from a year earlier, also a solid result. The risk is that the jobs numbers come in much higher than forecast, based on Wednesday’s ADP report showing U.S. firms added 275,000 jobs in April, the sixth-best figure going back to 2006. The two reports can often vary wildly, but based on historical correlations it wouldn’t be out of the realm to see the government report show 255,000 jobs were created in April, according to the rates strategists at BMO Capital Markets. If that were to happen, it’s likely to be interpreted as too much a good thing by markets, bolstering views that the Fed definitely won’t be cutting rates anytime soon and may even need to consider boosting them. Such a scenario would be bad for stocks and bonds, and good for the dollar. The largest upside surprise in ADP since February 2017, a strong rebound in the labor differential, and historically low jobless claims are all reasons for a positive bias, BMO noted. On the other hand, ISM Manufacturing employment dropped to the second-lowest read since November 2016, and the tick-up in Challenger job cuts could imply some weakness to the headline jobs figure.

DON’T MISS

Powell's Inflation Message Has Become Very Muddled: Tim Duy

Fed Needs to Develop a Better Feel for Markets: Mohamed El-Erian

Bank of England Tries Channeling St. Augustine: Marcus Ashworth

U.S. Expansion May Be Nowhere Near an End: Nir Kaissar

Politics Moves Faster Than Economists Gather Data: Noah Smith

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.