Markets Have More to Worry About Than Tariffs

A litany of market risks lead financial commentary. Plus, Bitcoin’s blast-off, a sagging Swiss franc and more.

(Bloomberg Opinion) -- Stocks around the world tumbled the most since December on Tuesday. The general sense was that investors remained on edge over President Donald Trump’s threat to increase tariffs on billions of dollars of imports from China, and China’s likely retaliation with more tariffs of its own. No doubt trade jitters were a factor, but focusing solely on that issue risks missing the bigger picture.

One underappreciated reason for the flight from equities was the European Commission’s decision to cut its 2019 growth forecasts for the euro area – collectively the world’s largest economy after the U.S. – to 1.2 percent from 1.3 percent. Although that’s not much, the biggest reductions were in two key economies: Germany and Italy. Plus, there had been a growing sense that the euro-zone economy was starting to look up after last week’s gross domestic product report came in better than forecast. In fact, the monthly Sentix Investor Confidence index released Monday showed the biggest gain since March 2015. That helps explain why most major European stocks indexes were down more than the S&P 500 by the time they closed around noon New York time. “The EC’s decision to lower its growth estimates for Germany and Italy look excessive in view of GDP data published last week,” Bloomberg Economics wrote in a research note. It’s also notable that U.S. stocks extended their declines and hit their lows of the day after House Speaker Nancy Pelosi warned that the Trump administration’s defiance of subpoenas could be an impeachable offense and the Pentagon said it’s sending B-52 bombers, in addition to the USS Abraham Lincoln aircraft carrier, to the Middle East as "prudent steps to protect U.S. forces and interests in the region and to deter any aggression" from Iran. Neither of those issues have anything to do with trade, but they will remind investors that the Goldilocks-like scenario that has played out this year in markets won’t last forever.

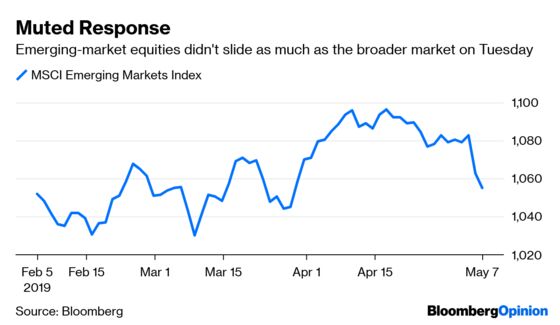

HIDING OUT IN EMERGING MARKETS

Emerging markets have a reputation for being volatile, tending to underperform in times of turmoil and outperform when times are good. On Tuesday, however, that notion took a hit. The MSCI Emerging Markets Index of equities fell just 0.61 percent, while the broader MSCI All-Country World Index tumbled 1.32 percent. It helped that China’s stocks actually rose, recovering a small part of Monday’s jaw-dropping 5.84 percent decline. It also helps that the outlook for emerging-market economies is brightening. The Institute of International Finance in Washington issued a report Tuesday saying that its measure of emerging-market growth was tracking at a 3.6 percent annualized rate in April, up from 3.2 percent in March. In addition to the sizable jump, the IIF notes the increase was the first in 14 months. The results seem to provide further proof that emerging markets have little to fear from a stronger dollar. The knee-jerk reaction from markets in recent years has been to dump emerging-market assets at the first sign of dollar strength, because of worries that borrowers in emerging markets will have a tougher time servicing the trillions in dollar-denominated debt they have taken out in recent years. But emerging-market growth has been firming even though the Bloomberg Dollar Spot Index is about its strongest since 2017.

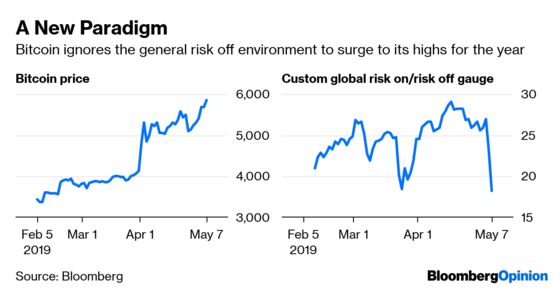

BITCOIN MAY BE FULFILLING ITS PROPHESY

One move that stood out was the rise in Bitcoin. The cryptocurrency jumped almost 5 percent to a new high for the year Tuesday amid the broadest “risk-off” atmosphere in markets since March. Could it be that Bitcoin is finally turning into a haven-like asset that so many of its backers have been predicting for a few years? It’s too early to tell, but it’s the evidence is mounting that Bitcoin’s correlation with the broader markets is diminishing. “Bitcoin is testing new near-term highs because the overall institutional involvement is becoming stronger and stronger,” Jehan Chu, managing partner at Kenetic Capital, told Bloomberg News. “We’re just seeing institution after institution lining up to the thesis of digital currency, and Bitcoin is the standard bearer.” Fidelity Investments, which began a custody service to store Bitcoin earlier this year, plans to buy and sell it for institutional customers within a few weeks, according to Bloomberg News, citing a person familiar with the matter. “Fidelity alone doesn’t move the entire needle, but Fidelity with E*Trade and Ameritrade” and others might. “You’re seeing a critical mass of these types of asset managers and brokers providing retail exposure and retail access to crypto,” said Chu, whose firm is a blockchain investment and advisory company.

WHAT’S UP WITH THE SWISS FRANC?

Speaking of havens, the Swiss franc is acting like anything but lately. It’s little changed the past two days against a basket of developed-market peers, and it’s down against the dollar, yen and even the euro. This isn’t a short-term phenomenon: the franc is down over the past while month the dollar and yen are higher. “Despite its status as the world’s principal safe-haven currency, movements in the (franc) have shown little regard for convention thus far this year - a thought many investors may have had amid the price action these past twenty four hours,” BNY Mellon Senior Currency Strategist Neil Mellor wrote in a research note Tuesday. “Such information is potentially of some value as we head into a summer in which investors may be looking to the support of the generic central bank ‘put.’” At least some of the franc’s underperformance can be attributable to comments by Swiss National Bank Chairman Thomas Jordan that there’s “always the possibility” that the central bank lowers interest rates further. And it’s not as if the SNB welcomes any strength in the franc, which Mellor points out the central bank still regards as “highly overvalued.” And it’s also not like the Swiss economy is going gangbusters. Recent data suggest manufacturing is shrinking for the first time since 2015 and retail sales just posted their biggest decline in six months in March.

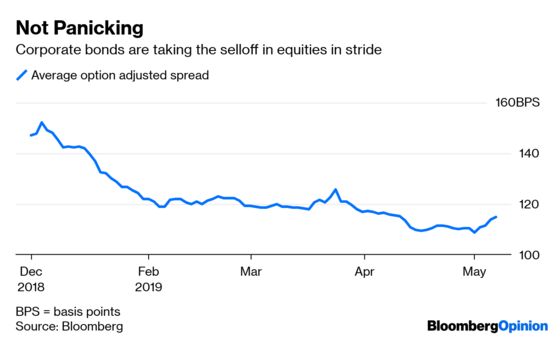

CORPORATE BONDS IN DEMAND

It was hard to escape that sinking feeling Tuesday watching stock markets steadily decline for most of the day. But there were was one big reason for optimism: The credit markets are working just fine. Bristol-Myers Squibb was on track to complete 2019’s largest bond offering and the 10th biggest ever, raising $19 billion across 9 tranches to help fund its $74 billion purchase of Celgene. Demand was heaviest for the longer-term maturities, which is an indication of animal spirits. The longest portion of the offering, a 30-year security, may yield about 1.45 percentage points more than similar-maturity Treasuries, after initial talk of around 1.6 percentage points, according to Bloomberg News’s Molly Smith and Rebecca Spalding. They report that Bristol-Myers is leading the charge for what’s expected to be a heavy month of new corporate bonds, potentially totally $120 billion, or 6 percent more than last May. T-Mobile and Fidelity National Information Services are conducting investor outreach ahead of potential jumbo M&A transactions, which may price in the coming weeks. More importantly, the increase in yield spreads has been relatively muted even with the flood of supply. While spreads have widened to about 1.15 percentage points from this year’s low of 1.09 percentage points last week, they remain well below this year’s high of 1.52 percentage points in early January.

TEA LEAVES

Fed Chair Jerome Powell suggested last week that the recent downturn in inflation rates is likely to prove transitory. Data in coming days will give a sense of whether that notion rings true. The government on Wednesday will release its producer price index report for April. The median estimate of economists surveyed by Bloomberg is that the index rose 0.3 percent last month, down from a 0.6 percent gain in March. Excluding food and energy, the measure likely increased 0.2 percent, versus 0.3 percent the prior month. Then on Friday, the government is expected to say that its consumer price index jumped 0.4 percent, the same as in March, but edged just 0.2 percent after stripping out food and energy. Bloomberg Economics said in its week-ahead preview that it “maintains the view that inflation will accelerate as the unemployment rate continues to dip further below its neutral level – but this may not be more evident until the economy moves beyond an inventory overhang in the latter half of this year.”

DON’T MISS

Trade Fears Threaten the Best U.S. Stocks: Stephen Gandel

Trump's Trade Tantrum Reopens Profit Wounds: Brooke Sutherland

New Trade Agreement With China Wouldn’t Change Much: Tyler Cowen

Trade Talks Founder on Mistrust and Arrogance: David Fickling

Leveraged-Loan Pushback Is Too Little, Too Late: Brian Chappatta

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.