Markets Abhor a Candid Central Banker

Is Mario Draghi’s dour assessment an admission of defeat? Plus, a slumping Swissie, Einhorn’s bet against easy money and more.

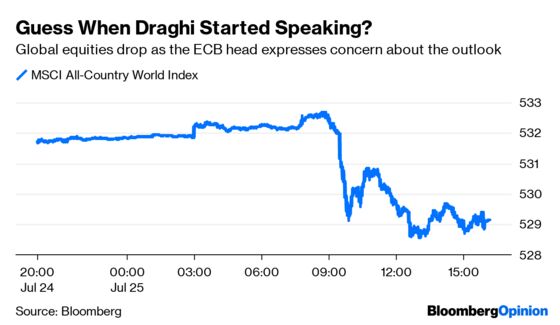

(Bloomberg Opinion) -- Everything was going according to plan, with the MSCI All-Country World Index of global equities rallying as the European Central Bank signaled that it was setting the stage for an interest-rate cut in September. But then Mario Draghi started speaking, saying at the outset of his press conference that the outlook was “getting worse and worse.” Equities quickly went from their highs of the day to having one of their worst days of the month.

The comments we’re so much a surprise as they were a shock. Everyone knows that the outlook for Europe’s economy is bleak, but nobody wants the person in charge of the world’s second-largest economy to seemingly admit defeat. The comments laid bare that not even years of zero interest rate policies by major central banks nor trillions of dollars spent on bonds and other financial assets can get the global economy to reach escape velocity. And the only answer central bankers have is to double down on failing policies. Sure, the global economy might be in much worse shape if central banks hadn’t taken the extraordinary measures that they had following the financial crisis. It’s clear, though, that they need to come up with other ideas to spur growth because more easing will be something like pushing on a string. “A perpetual state of easing is no longer easing because it doesn’t incentivize consumers and businesses to act today instead of tomorrow. They’ll just wait until tomorrow,” Bleakley Financial Group chief investment officer Peter Boockvar wrote in a note to clients. “Thus, it’s not stimulus anywhere because nothing gets stimulated outside of asset prices.”

A Bloomberg Economics index that aims to track the global economy shows gross domestic product likely expanded at just a 2.36% rate in the second quarter, more than a percentage point lower than the average of 3.55% since the recovery began in late 2009. Growth averaged 4.09% between early 2001 and mid-2008. “Draghi’s tone did more to raise recession fears than it did to ease them,” Jim Paulsen, Leuthold Group Inc.’s chief investment strategist, told Bloomberg News.

A BAD DAY MADE WORSE

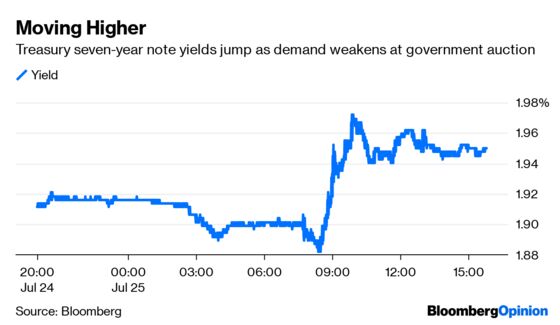

Draghi also had an impact on the bond market, as government debt in Europe and the U.S. reversed their gains and fell, pushing yields higher. It’s not that Draghi’s “worse and worse” comment spooked traders; they already knew that the outlook is pretty bad. Rather, they were disappointed that the ECB didn’t show a greater sense of urgency and cut rates now instead of waiting until September. But perhaps more alarming, there’s more evidence that investors are getting worried about mounting U.S. debt and deficits. Although lawmakers this week reached an agreement to suspend the debt ceiling to July 31, 2021, the deal came with new spending and limited savings that, taken together, will likely push the annual budget deficit to more than $1 trillion next year. That may be one reason why demand was soft at the Treasury Department’s auction on Thursday of $32 billion in seven-year notes. Investors submitted bids for just 2.27 times the amount offered, matching the lowest so-called bid-to-cover ratio for that maturity since 2009. The yield of 1.967% was higher than the 1.953% the securities were trading at just before the auction, which is another sign of weak demand. The Bloomberg Intelligence rates strategists pointed out that this was the fourth straight auction where yields “tailed.” Yes, wouldn’t be as relatively low as they are if there wasn’t a decent demand, but it appears investors will increasingly need a reason to buy.

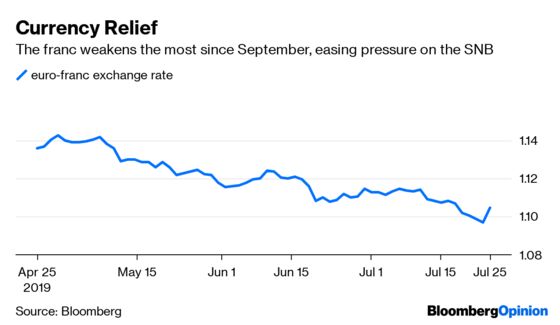

THE SWISS FRANC MAKES A MOVE

The euro strengthened following the ECB monetary policy meeting and Draghi’s press conference, and no one was more happy to see that happen than the Swiss. The Swiss franc tumbled as much as 0.78% against the euro in its biggest decline since September. Before Thursday, the franc had strengthened to its highest level since 2017 against the euro zone’s common currency, spurring speculation that the Swiss National Bank would consider exerting pressure on markets to help keep the so-called Swissie in check, according to Bloomberg News. Switzerland’s central bank is especially sensitive to changes in the value of its currency. Recall that back in early 2015 it roiled global markets by abandoning its currency cap. No one is saying that the Swiss National Bank is poised to take drastic measures to control the currency, but “one should certainly not exclude the possibility of the SNB matching prospective policy action on rates by the ECB if necessary,” said Credit Agricole analyst Manuel Oliveri. The SNB is “very much focused” on preventing a divergence, he said. For Marc Chandler, the chief market strategist at Bannockburn Global Forex, the move in the euro-franc exchange rate is just a reflection of a broader short-squeeze in the common currency. Many big banks had expected the Swiss franc to rally on the ECB and were leaning the wrong way, he said.

EINHORN PLAYS WITH FIRE

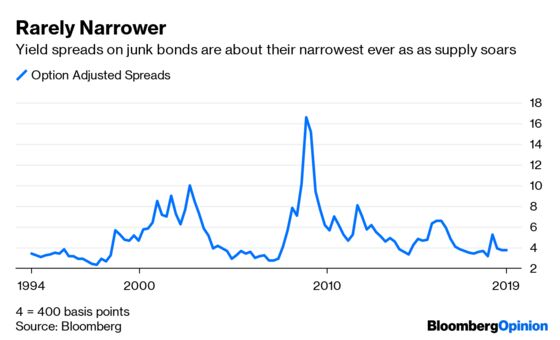

No discussion about financial market bubbles is complete without a reference to corporate credit. Yield spreads remain near record lows despite the slowing economy. Easy-money central bank policies have allowed borrowers to access credit seemingly with no questions asked. For proof, the amount of junk bonds tracked by the Bloomberg Barclays U.S. Corporate High Yield Bond Index has more than tripled to $1.26 trillion since the financial crisis. Hedge fund manager David Einhorn thinks the party is over, disclosing that he’s shorting U.S. corporate debt, according to Bloomberg News’s Katia Porzecanski and Claire Boston. Einhorn believes that the demand for anything with a yield has allowed borrowers to get away with terms they never would have obtained before, eroding protections for creditors. “Rating agencies have been complacent,” Einhorn wrote in a July 25 letter to investors seen by Bloomberg News. “Meanwhile, we are a decade into an economic recovery and there are signs the economy may be slowing.” Countless numbers of investors have bet against the credit market and lost in recent years, mainly because central banks have remained surprisingly accommodative. That has allowed the riskiest companies to stay alive by refinancing and rolling over debt. That may come to an end one day, but with central banks turning even more dovish, it’s hard to say when.

CLIMATE CHANGE HITS HOGS

Europe is not the only region that’s sweltering in a heat wave. In fact, scientists predict July will end up as the hottest month on record, bolstering evidence that the global climate is changing. This is, naturally, having an impact on the commodities market. And nowhere is that more evident than with America’s herd of hogs. It’s been so hot that pigs are sweating off the pounds, according to Bloomberg News’s Lydia Mulvany. But that’s not a bad thing for farmers or prices. The fact is, until lately, hog herds had not only grown, but the pigs had gotten too fat. So hog producers aggressively sold animals in June to try and work through burdensome supplies, which sent cash prices tumbling. Now, the average weight of pigs sent to slaughter is falling, signaling that the marketers successfully offloaded their too-numerous winter and spring hogs and now have a more slender summer lot to sell, Mulvany reports. As a result, prices are rebounding. National spot prices for hogs average 80.88 cents a pound, up from about 66 cents earlier this month. “With hog weights more under control and hot summer weather in the forecast, producers are no longer desperate to try to move hogs,” Steiner Consulting Group said in a report Wednesday.

TEA LEAVES

The U.S. government on Friday will provide its first read of second-quarter gross domestic product. The thinking among economists is that it won’t be pretty, with growth coming it an annualized rate of 1.8%, matching the slowest pace since the first quarter of 2016. But there is reason to believe that the data will exceed expectations. Some economists were busy Thursday reworking the numbers after the government said durable goods orders increased by a greater-than-forecast 2% for June. RBC Capital Markets Chief U.S. Economist Tom Porcelli and FTN Financial’s Chris Low both wrote in separate reports that it’s likely GDP will come in at about the same rate. “If growth continues from here, it could be a game changer for the second half,” Low wrote. “Weak business-fixed investment is the economy’s primary vulnerability, and this report suggests it is not nearly as vulnerable as it appeared a month ago, which in turn suggests GDP estimates could be revised up a couple of tenths.”

DON’T MISS

Draghi's ECB Message Brings Europe No Sunshine: Marcus Ashworth

Warren's Private Equity Proposal Encourages Abuses: Aaron Brown

Moody’s Catches on to Climate Risk Mispricing: Leonid Bershidsky

Game Theory Backs Boris Johnson's Hard Line: Mohamed A. El-Erian

U.S. Mistakes Hand Canada an Opening in High Tech: Noah Smith

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.