Lyft Joins the Litter of Unicorn Disappointments

Lyft shares were initially higher in after-hours trading following the release of the earnings report but then retreated.

(Bloomberg Opinion) -- Lyft Inc.’s rocky road as a public company should be a warning for other highfliers hoping to hit it off with stock investors. It is ugly out there for the elite startup superstars.

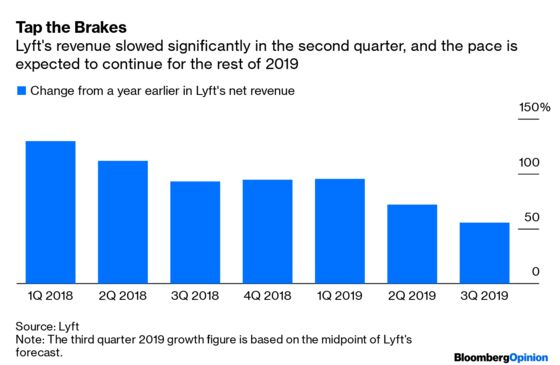

Lyft said in its second-quarter earnings report on Wednesday that the rate of revenue growth slowed less than it had forecast and that losses weren’t as bad as investors expected. Still, even the company’s slightly raised forecast for 2019 revenue growth of as much as 62% would represent a comedown from last year, when Lyft’s revenue was doubling or more year-over-year. Both Lyft and rival Uber Technologies Inc. are posting slowing growth at the same time they’re telling investors that they’re just barely scratching the surface of their potential.

Lyft shares were initially higher in after-hours trading following the release of the earnings report but then retreated. Questions about Lyft’s slowing growth, high losses and the general viability of on-demand transportation have pushed its share price far below the $72 at which the company sold stock in its initial public offering in March. Shares of Uber have also been underwater since its IPO. And those two are far from alone in their misery.

For all the hype about the post-2008 class of high-profile, highly valued and highly disruptive technology startups, many of the biggest “unicorns” that have gone public so far have been stinking up public stock markets like a skunk waddling into a picnic. In addition to the decline in shares of Uber and Lyft, the prices for Snapchat, Dropbox Inc., Spotify Technology SA and China’s Xiaomi Corp. and Meituan Dianping are also below their IPO levels.

For many of the top tier of richly valued young technology companies, the early message from public investors has been clear: If the company’s business model is a string of question marks and there are few public precedents and high losses, stock buyers are not greeting them with open arms. The lackluster performance of the unicorn elites isn’t a great setup for WeWork Cos., Postmates Inc., Didi Chuxing Inc. and others in the crop of still-private startup elite edging to go public soon, with even-bigger-than-Uber-sized doubts about their viability and wild valuations.

Many more richly valued startups remain private, so it’s too soon to call the elite unicorn crop a success or failure. But if the top-flight startups are being greeted with skepticism in the midst of an unprecedented decade-long bull market for U.S. stocks, what happens when and if market conditions deteriorate?

There are notable exceptions to the public investor shunning of unicorns. Investors are crazy in love with young tech companies that sell software or other products to businesses. The tier of tech startups below the richly valued elites such as Uber — think Zoom Video and Stitch Fix Inc. — have typically fared better than many of the superstars. Pinterest Inc., the online scrapbook, has a familiar advertising-based business model, seems to be managing itself well and has a share price that reflects hopes rather than fears. (A familiar business model hasn’t helped the less competently managed Snap Inc. Even after a wild run-up this year, Snap shares are trading below the price at which the company went public in early 2017.)

Even with the declines, there probably aren’t many regrets among the early backers of the elite unicorns. Investors who bought shares of companies such as Lyft and Snap early in their lives have made a fortune. Even stock buyers who bought at significantly higher prices soon before the IPO may feel fine about the investments because they were adding to stakes built earlier or they were making relatively small starter investments for giant investment funds.

This underscores why the last decade of startup investing has been so odd. It has been economically rational for investors to pour money into young companies and prod them to grow as big and fast as possible. Even when those startups aren’t home runs if they become public companies, those early backers have done fine, or far more than fine.

There are few losers, then. The early backers of elite startups are in the black. Buyers of public stocks can shun the young companies if they are too speculative once they go public. It’s all good — except for the startups themselves, perhaps. They are the ones under the most pressure to figure out how to thrive far into the future.

Investors seemed a bit spooked by the company's early end to restrictions on insiders to sell Lyft stock. The company's shares are heavily shorted, which tends to exacerbate stock movements.

Slack Technologies Inc. may be trading below its first stock sale in its non-IPO earlier this year, but it has generally been greeted warmly and its stock trades at a rich multiple.

Some of the unicorns are still underwater compared with share sales from years ago. Dropbox's per-share price now is lower than private purchase of company shares from 2014. Uber's stock is about even with the the level of 2015 share sales. Snap stock price isn't much higher than private share transactions two and a half years ago.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.