Lufthansa’s Superstar Pilot Goes from Hero to Zero

(Bloomberg Opinion) -- If it’s true that all political lives end in failure, then the same could be said for business. Carsten Spohr became Deutsche Lufthansa AG’s chief executive in 2014, made an impressive start, and had his contract extended to the end of 2023. He may regret signing up for that long.

The German airline’s shares tumbled 12 percent on Monday after it issued a second profit warning in as many months. It expects to generate as little as 2 billion euros ($2.2 billion) of operating profit in 2019, up to 25% below what was expected by analysts.

The stock is now worth less than four times last year’s earnings, a pretty pitiful multiple, and investors who bought the stock when Spohr took over have lost money. Suddenly, a man feted as one of Germany’s most accomplished corporate leaders looks ordinary.

How times have changed. Spohr’s response to a 2015 aircraft crash at the Lufthansa offshoot Germanwings was both sensitive and assured. Later on he faced down industrial action to win concessions from staff on pensions. In 2017, Lufthansa’s profit hit a record high and the stock price soared 150%. Spohr was duly named Manager of the Year by Germany’s influential Manager Magazin.

Sustaining all of this was always going to be hard in the notoriously unstable airline business. Fuel costs have risen, rivals have added new capacity and air cargo demand has waned, thanks in part to U.S. President Donald Trump’s trade crusades. (It’s worth reading Bloomberg’s William Wilkes on Lufthansa’s litany of problems.)

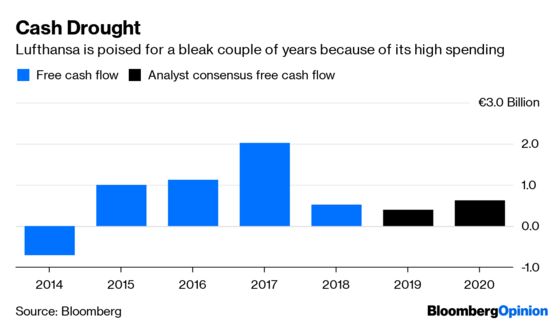

But Spohr can’t just blame external factors. His company has chased growth to the detriment of profitability and it has spent heavily on new jets and integrating older ones from the insolvent Air Berlin. Gross capital expenditure jumped 8% to 3.8 billion euros ($4.3 billion) last year, leaving precious little spare cash.

While Lufthansa is still doing fine on long-haul routes, Spohr’s big idea — a budget subsidiary called Eurowings — has been a disaster. The new unit was meant to challenge Ryanair Holdings Plc and EasyJet Plc in Europe, and to serve long-haul holiday destinations, but it lost more than 230 million euros last year. Instead of breaking even in 2019, as was anticipated, it will now remain in the red.

Spohr has hit the brakes on Eurowings’s expansion but the company plans to “vigorously defend” its dominant market position in Germany and Austria. Translated, that sounds worryingly like: “Fare war? Bring it on.”

Ryanair is pursuing a similar battle of attrition against weaker rivals such as Norwegian Air Shuttle ASA, with the aim of forcing them out of business. But Ryanair’s costs are much lower than those of Eurowings.

Of course, Lufthansa can afford a couple of bleak years. At the end of March it had 12 billion euros of net debt, aircraft lease and pension liabilities — or about 2.4 times Ebitda (a measure of earnings). Norwegian’s leverage is miles higher.

But when your corporate strategy is all about acquisition (Thomas Cook Group Plc’s German arm could be next on Spohr’s shopping list) and heavy investment, falling profits are doubly alarming. They suggest cash might be misallocated. “We think the sooner the company focuses on value for shareholders and less chasing or defending market share, the better for the shares. We see no hint of that yet,” RBC’s Damian Brewer complained.

At an investor event next week, Spohr has a chance to explain how he plans to fly Lufthansa out of this mess. Once seen as a safe steward of Lufthansa’s capital, he’s starting to look a little reckless.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2019 Bloomberg L.P.