Blackstone Finds It Pays to Leave Something on the Table

(Bloomberg Opinion) -- The market’s positive reaction to London Stock Exchange Group Plc’s planned $27 billion takeover of Refinitiv is a sign investors think the U.K. bourse is getting a great deal. If that’s right, couldn’t buyout firm Blackstone Group LP, which is selling the data provider, drive a harder bargain?

London Stock Exchange shares jumped as much as 16% on Monday morning, adding 3.1 billion pounds ($3.8 billion) to the group’s market value. One interpretation is that investors think the company is paying a low price for the former Financial & Risk division of Canadian information group Thomson Reuters Corp. (Bloomberg LP, the parent of Bloomberg News, competes with Refinitiv in providing financial news, data and information.)

For LSE, a transaction of this scale isn’t without its risks – even if it intends to pay in shares rather than cash. Taking on Refinitiv’s net borrowings – $12 billion at Dec. 31 – could push leverage to comfortably over three times Ebitda at the point of completion, well above LSE’s target limit of two times. There’s also the risk of a distracting and lopsided integration: Refinitiv has 18,500 employees and LSE only 4,500.

But the market judges that the strategic and financial benefits clearly outweigh the risks. The takeover would accelerate LSE’s transformation into a data provider from a trading platform. Financial information and index revenue would account for more than half of the group’s total after the deal, according to Bloomberg Intelligence.

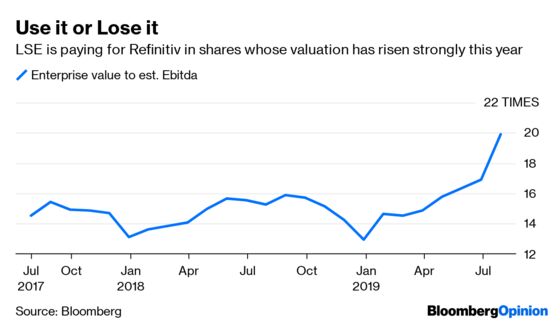

And the valuation put on Refinitiv is undemanding. The initial terms value it at 13 times adjusted 2018 Ebitda, according to JPMorgan Cazenove analysts. If you assume that the company’s future financial performance will benefit from Blackstone’s cost-cutting, the purchase price could be roughly 10 times underlying Ebitda for 2019 – about half the multiple at which LSE shares trade.

Couldn’t Blackstone have pushed for a higher valuation – something closer to, say, $30 billion? True, it’s already doing well on the terms as proposed. The private equity firm’s consortium deployed $4 billion in equity and preferred stock when it bought a 55% stake in Refinitiv last year. As things stand, it would receive LSE shares worth more than double that based on their current price.

But lock-ups will prevent Blackstone and its partners from cashing in their stakes in a hurry. LSE says this provision will involve a “long-term partnership”. If that is to be meaningful, the restriction would have to endure for the typical holding period for private equity investments, about five years. So the final internal rate of return on Refinitiv will be much lower than that implied by the preliminary terms of this deal.

It would nevertheless be difficult for Blackstone to demand a higher price. The warm reaction of LSE shares makes it more likely that the exchange’s shareholders will approve the transaction. That should matter a lot to Blackstone, which has endured some knock-backs from the public markets recently – Scout24 AG shareholders recently rejected the buyout firm's offer as too low. Here the New York-based firm happens to be the vendor, but a transaction would still need to get the nod from LSE shareholders.

Blackstone clients may wish the private equity firm was getting a bigger slice of the enlarged LSE. But the jump in the exchange’s shares – assuming it holds – should increase both the certainty of the deal completing and the value of it to them. Sometimes it pays to leave something on the table.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.